Day after day, Wall Street investors fret that artificial intelligence could disrupt white-collar industries by turning expert human judgment into code.

Stock picking appears to sit squarely in the path of that disruption.

A new academic study led by a Harvard Business School professor finds that much of what active fund managers do follows patterns machines can learn. Using a machine-learning algorithm called a neural network, the system could predict about 71% of mutual-fund trading decisions — whether a manager would buy, sell or hold a given stock over a quarter.

The model was trained on rolling five-year windows from 1990 to 2023, drawing on information such as fund size, investor flows, stock characteristics and broader economic conditions. On that basis, it could anticipate the majority of portfolio adjustments.

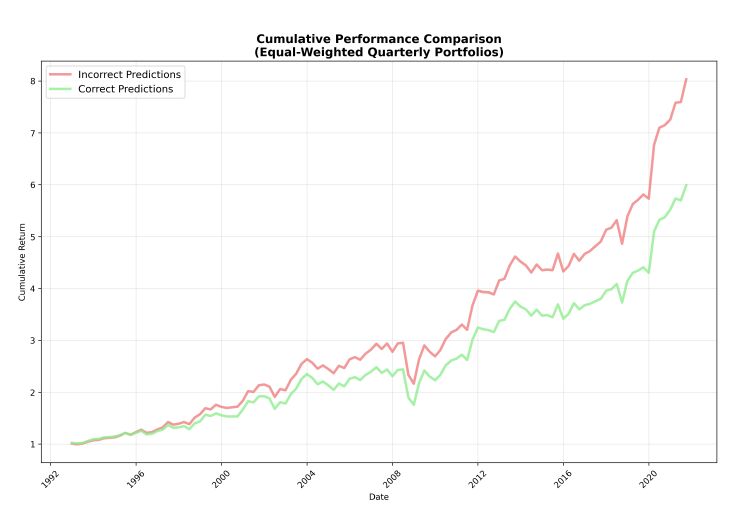

The twist: its limits may be more revealing than its success. The trades the system failed to anticipate — roughly 29% — were, on average, more closely associated with outperformance. In other words, the activity that falls outside routine, detectable investment patterns appears to be where most of the value lies.

The implication is not that machines have cracked markets. Rather, they appear to have learned much of the industry’s common playbook — how managers tend to react to flows, market trends and their peers. What they struggle to capture is the smaller share of decisions that depart from that playbook.

“If 71% of your decisions can be anticipated by an algorithm, it becomes very hard to justify active-management fees for that portion,” Lauren Cohen, a finance professor at Harvard who co-authored the paper, explained in an email. “Now, the non-routine trades, the ones our model can’t predict, are where genuine alpha lives. But those account for a relatively smaller share of overall activity.”

The working paper, posted last week to the National Bureau of Economic Research and titled Mimicking Finance, arrives at a moment when artificial intelligence is rocking increasingly specialized corners of professional services. In recent weeks, fears of AI disruption have sent shares of companies from wealth managers to logistics groups swinging sharply.

For active fund managers, the critique is not new. Investors have been shifting money out of stock-picking funds and into low-cost index products for years. The industry’s central promise has long been “alpha” — returns above a benchmark like the S&P 500 — even as quantitative models have steadily raised the bar by showing how much performance can be explained by broad market exposure and familiar investment styles.

This study, co-authored with Yiwen Lu at the University of Pennsylvania and Quoc H. Nguyen at DePaul University, pushes that erosion further. Earlier research largely dissected returns after the fact. By contrast, the new paper attempts to anticipate the trades themselves. Machine-learning models, the authors argue, are better suited than traditional linear factor models to capture the complex ways that managers respond to flows, market signals and one another.

Seen through that lens, the result is less a triumph of machines over markets than a reframing of what active management consists of. Much of the day-to-day activity of funds appears to follow patterns that can be mapped — and, in principle, reproduced at lower cost.

Some of those predictable buy-and-sell trades can serve essential purposes — managing liquidity, adjusting risk or rebalancing portfolios, Cohen says. But if the bulk of that activity is actually rules-based, it becomes harder to argue that it requires expensive discretion.

“The ‘human judgment’ component turns out to be more systematic than it appears, but you need flexible enough tools to see that,” Cohen said.

The paper also finds that predictability varies. Larger funds, those charging higher fees, those run by bigger teams and those facing more competition tend to be less predictable on average, while managers with longer tenures or multiple products tend to be more so. The model predicts the direction of trades rather than their size — a limitation the authors plan to address in future work.

For all the recent enthusiasm around AI, the findings underscore a distinction. Predicting how managers behave appears easier than predicting how markets move. Asset prices reflect the interactions of millions of participants and shifting expectations. Professional habits, by contrast, often follow recognizable patterns.

Ultimately, the narrower band of trades that the model failed to anticipate tended to perform better — a sign they may reflect human ingenuity, such as uncovering information on a stock others overlooked. Simply being random is unlikely to produce the same result.

Of course, machines could get even better as they collect more data. For now, however, the implications are economic rather than existential. If most portfolio adjustments can be anticipated by an algorithm, the justification for active fees increasingly rests on the smaller share of decisions that depart from the template.

“The genuinely skilled part, the unpredictable, non-routine component, is real but small,” Cohen said. “The policy implication is less about replacing managers wholesale and more about repricing what their predictable versus unpredictable activity is actually worth.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Justina Lee, Henry Ren