As investors digest the potential impact of artificial intelligence and debate whether this new technology will help or destroy existing businesses, a sharp divergence is occurring in global equities.

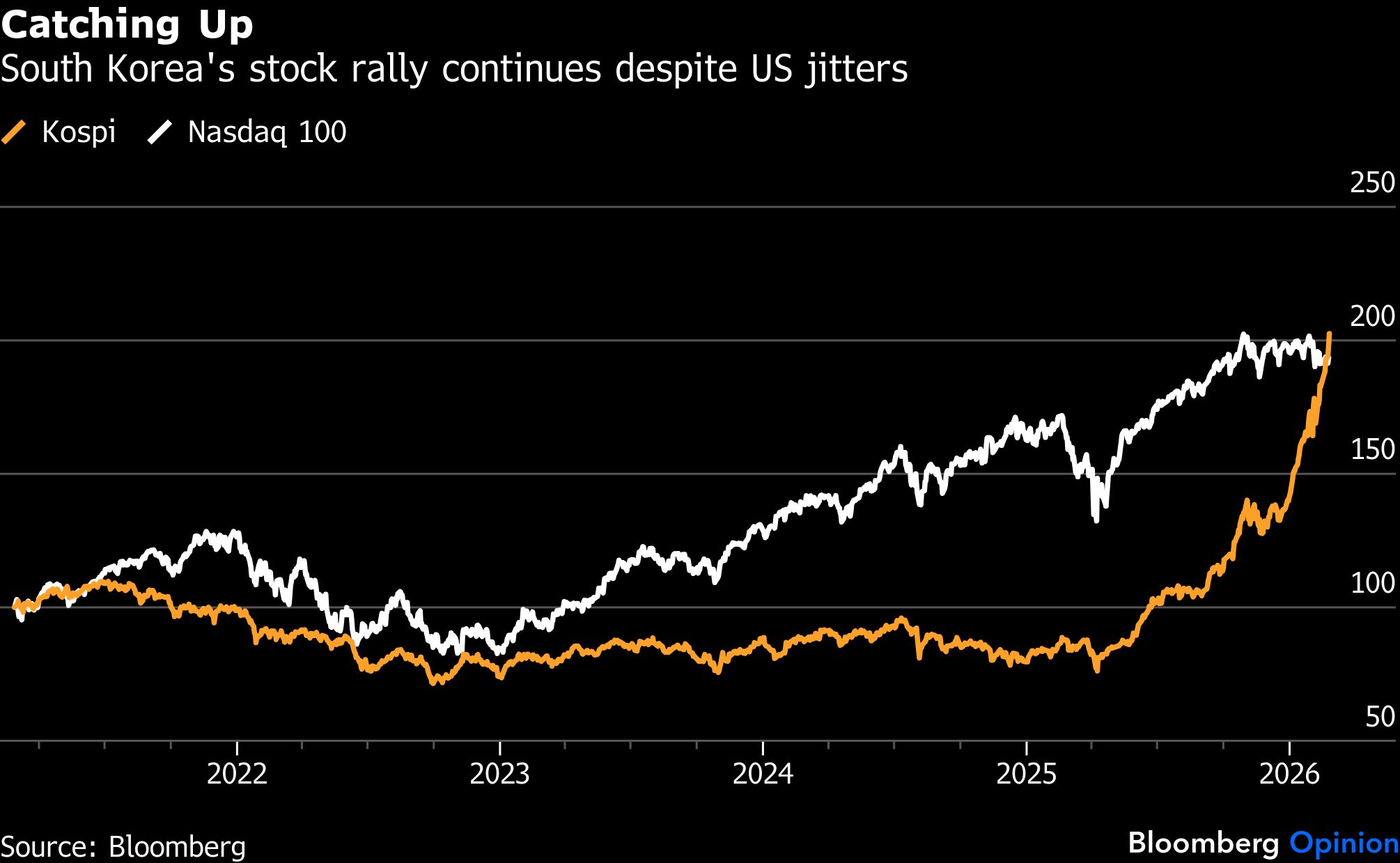

US stocks, which for years received strong, steady foreign money inflows, have experienced sharp selloffs lately as fear of AI’s disruptive power dragged down shares of software and services companies. By comparison, South Korea, one of the world’s most notorious value traps, has managed to ride through all those jitters and now repeatedly breaks records. The blue-chip Kospi Index is up 44% this year after 2025’s 76% spectacular run.

Given the anemic performance of US stocks, global asset managers are naturally discussing international diversification. As such, this is a good time to introspect and ask if long-held investing paradigms deserve a rewrite. I see two myths that need to be dispelled.

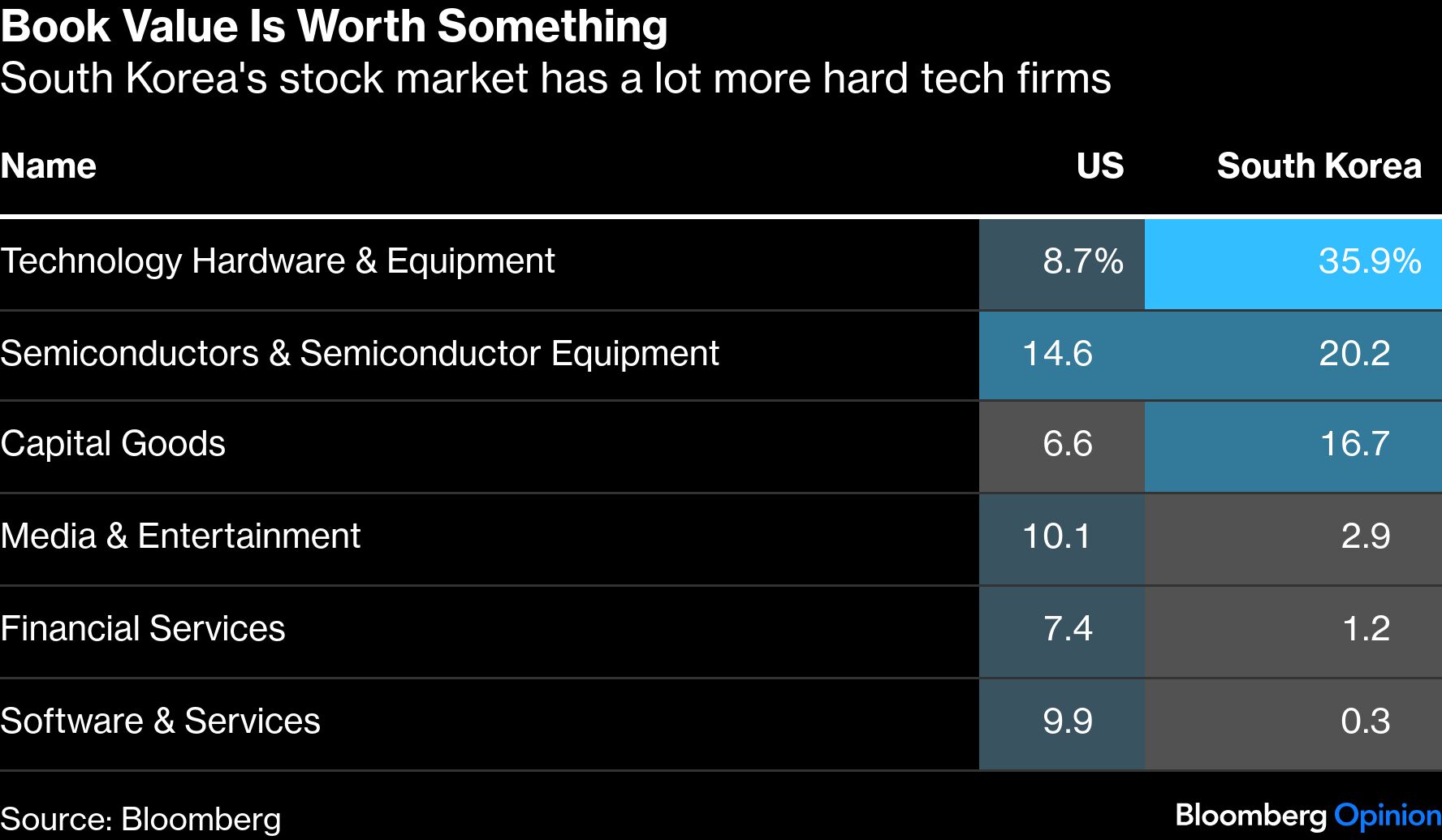

First, book value, or the net worth of a company according to accounting rules, is being re-priced. In the past, asset managers favored software companies, which tend to have fewer items on their balance sheets because their primary assets are intangibles such as intellectual property. The logic was that these firms had better customer stickiness and thus more recurring revenue. Their stocks, in turn, were rewarded with higher market valuation due to clear earnings visibility.

On the other hand, industrial companies, which often have much higher book value because of their factories and equipment, were unloved. Their revenues were seen as more sensitive to macroeconomic business cycles. Poor earnings visibility therefore gave them relatively lower market value.

The AI scare trade, which predicts that the arrival of new, AI-powered players will reshape competitive landscapes, is turning the narrative around. Investors are questioning the sustainability of recurring sales at legacy tech firms such as International Business Machines Corp. Meanwhile, they are clamoring for semiconductor manufacturers, such as Samsung Electronics Co. and SK Hynix Inc.