Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The recent rotation from growth to value is well documented. While the return divergences between technology stocks and materials or industrials stocks are significant, they do not tell the whole story. There are also extreme return differentials between broad industries and their sub-industries.

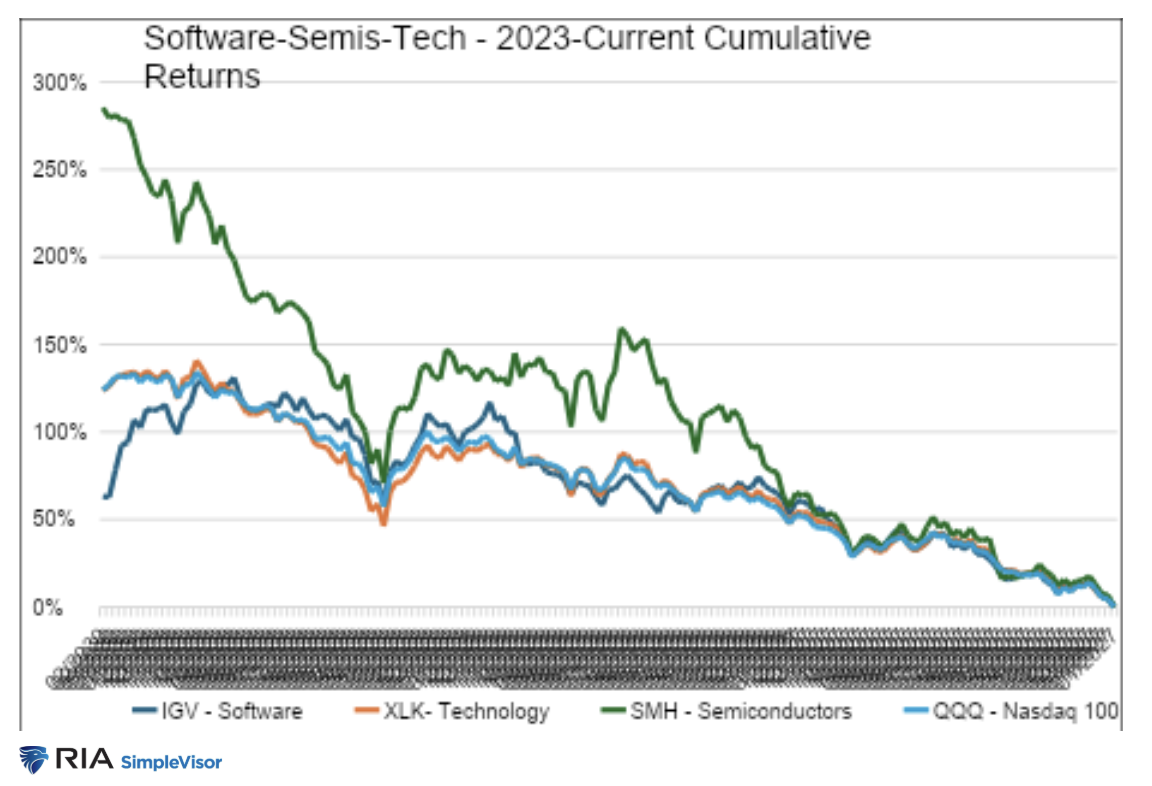

In this article, we address the divergence of the broad technology sector and the software-as-a-service (SaaS) sub-industry. The graph below shows the wide gap in returns between software, technology, the Nasdaq 100, and semiconductor stocks. Since the well-followed iShares Expanded Tech-Software Sector ETF (IGV) peaked on September 19, 2025, it has fallen 30%. For context, broad technology funds such as the State Street Technology Select Sector SPDR ETF (XLK) and the Invesco QQQ ETF (QQQ) are flat over the period, and the VanEck Semiconductor ETF (SMH) is up 30%.

Narratives Drive Passive Flows

Behind every good stock or index move is a narrative—the market’s collective explanation for why prices move. Most narratives have some truth, some degree of speculation, and include some falsehoods. The job of an individual or professional investor is to understand the narratives driving money flows, assess their accuracy, and trade accordingly.

As if evaluating the validity of narratives weren’t hard enough, we must also consider that many are based on expectations — and no one knows with certainty what the future holds.

The bearish software narrative — known as the SaaSpocalypse — serves as the market rationale for recent drawdowns in many software stocks. It contains some truths, plenty of speculation, and some outright falsehoods. Let's explore the narrative, examine the counterpoints, and assess whether software stocks are a steal or, as some claim, on their way to zero.

The SaaSpocalypse Narrative

The SaaSpocalypse story holds that the current AI wave poses a significant threat to traditional software companies because AI changes how software is built, delivered, and priced.

If generative AI can write code, automate workflows, and create customized applications rapidly and at a low cost, the value of today’s established off-the-shelf software products declines, and in some cases, may approach zero. Instead of paying for software and recurring subscription fees, enterprises and individuals may soon be able to build their own software easily and cheaply with generative AI.

As if that weren’t enough of a threat to traditional software companies, AI lowers the barriers to entry, enabling more competitors to quickly replicate existing software. More competition should compress profit margins and weaken the moats that once protected large software firms.

Rebutting the Narrative

The primary rebuttal to the SaaSpocalypse is that the value of software lies beyond the code. Enterprise SaaS companies derive their lasting power from durable moats such as network effects, high switching costs, proprietary data, compliance infrastructure, and trust.

AI-created software or a competing software product from an AI-driven startup might replicate the look and feel of a traditional software program, but it cannot recreate years of customer data, deep integration with other core systems, and, importantly, the confidence required for corporate deployments. Essentially, the rebuttal argues that the narrative fails to distinguish between the look and feel of software and the other attributes that can make it valuable.

Moreover, the narratives ignore that AI will help existing software companies improve their products, reduce costs, and, in some cases, make their moats even more durable. Current software producers have a huge leg up because they already have distribution networks, customer bases, and staff who understand the intricacies of their products and how customers use them.

However, the rebuttal may not apply to all software companies. Each software product and company should be judged according to its own merits. Basic, generic products that can be easily programmed with AI are more likely to be replaceable than widely distributed products with significant usage and data connections within companies.

Strong Moats

We asked ChatGPT for examples of SaaS companies with strong moats and received the following:

ServiceNow — Workflow + Enterprise System Depth

Why the moat holds up:

- Deeply embedded into IT service management, HR, security, and enterprise workflows — replacing it means re-architecting internal operations, not just swapping software.

- AI agents actually increase their value because orchestration becomes more important than stand-alone apps.

- Enterprise workflows contain thousands of hidden rules and dependencies that are hard for AI copilots to replicate. Research shows LLMs struggle with these types of opaque enterprise systems.

Salesforce — Data + Ecosystem Lock-In

Why it’s durable:

- Massive installed enterprise base + heavy customization.

- CRM data accumulation over many years = high switching friction.

- Ecosystem moat (partners, integrations, internal workflows, apps).

Even though AI can generate workflows or lightweight CRMs, enterprises still need:

- Enterprise data governance

Datadog — Observability Data Moat

Why this one stands out:

- Continuous telemetry ingestion creates a proprietary “data exhaust.”

- AI needs observability platforms — agents can’t fix or optimize what they can’t measure.

- Integrated logs + metrics + traces across thousands of systems = massive operational switching costs.

AI may help explain incidents, but it doesn’t replace the monitoring layer itself.

Opportunities In SaaS Stocks

We began this article with a graph showing software ETF IGV’s gross underperformance relative to the broader technology sector. We will now dig deeper to help form short-term return expectations for SaaS companies.

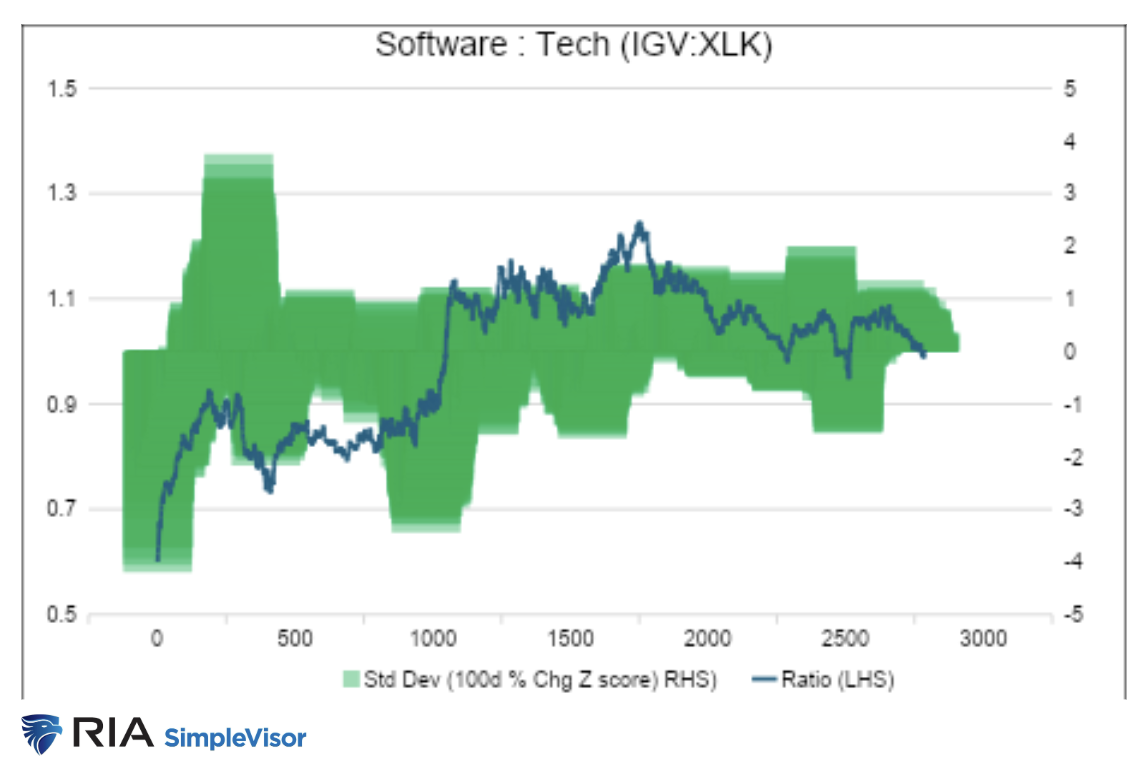

XLK vs. IGV

The first analysis compares software ETF IGV to broad technology sector ETF XLK. Within XLK's top 10 holdings, Microsoft (MSFT) and Palantir (PLTR) are the only two names that are also in IGV’s top 10 holdings.

The graph below shows the price ratio of IGV and XLK. As shown in red/green, the most recent 100-day price ratio change is almost 4 standard deviations from the norm.

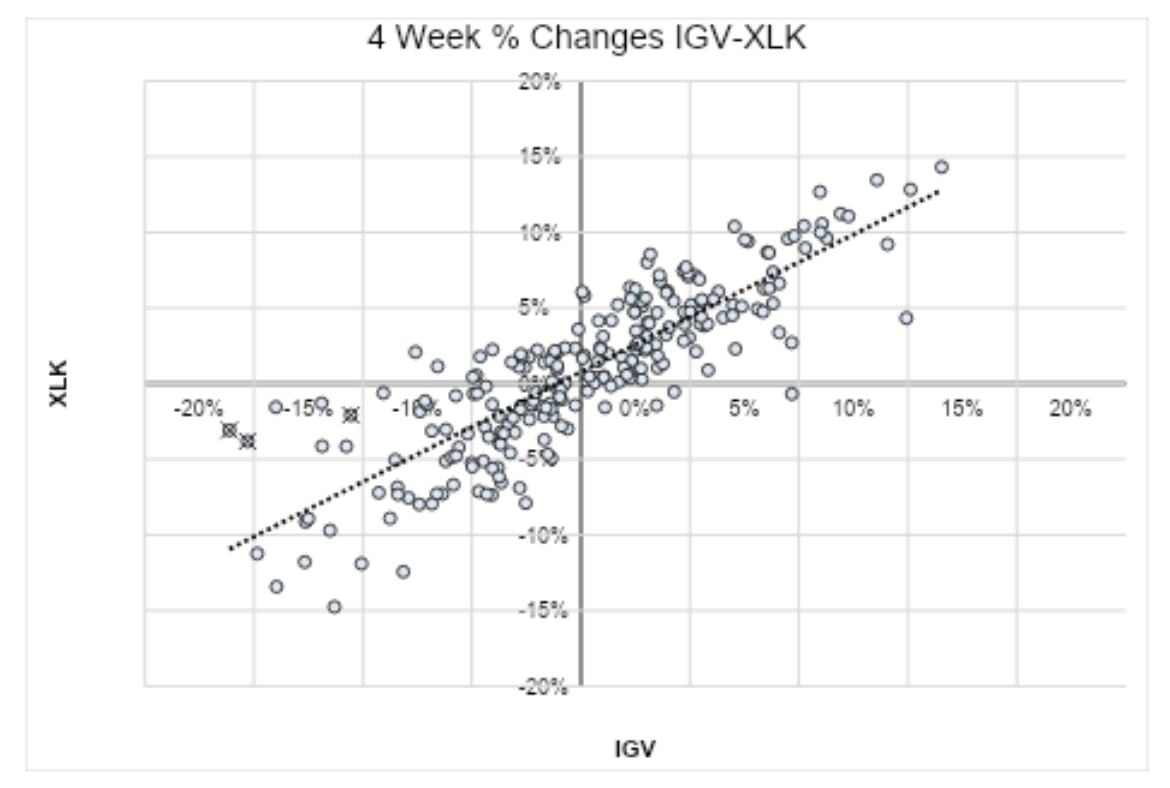

The next graphic uses the last five years to show how detached the sturdy relationship has become recently. Per the most recent weekly readings (green), either XLK is 10% overpriced or IGV is 10% underpriced.

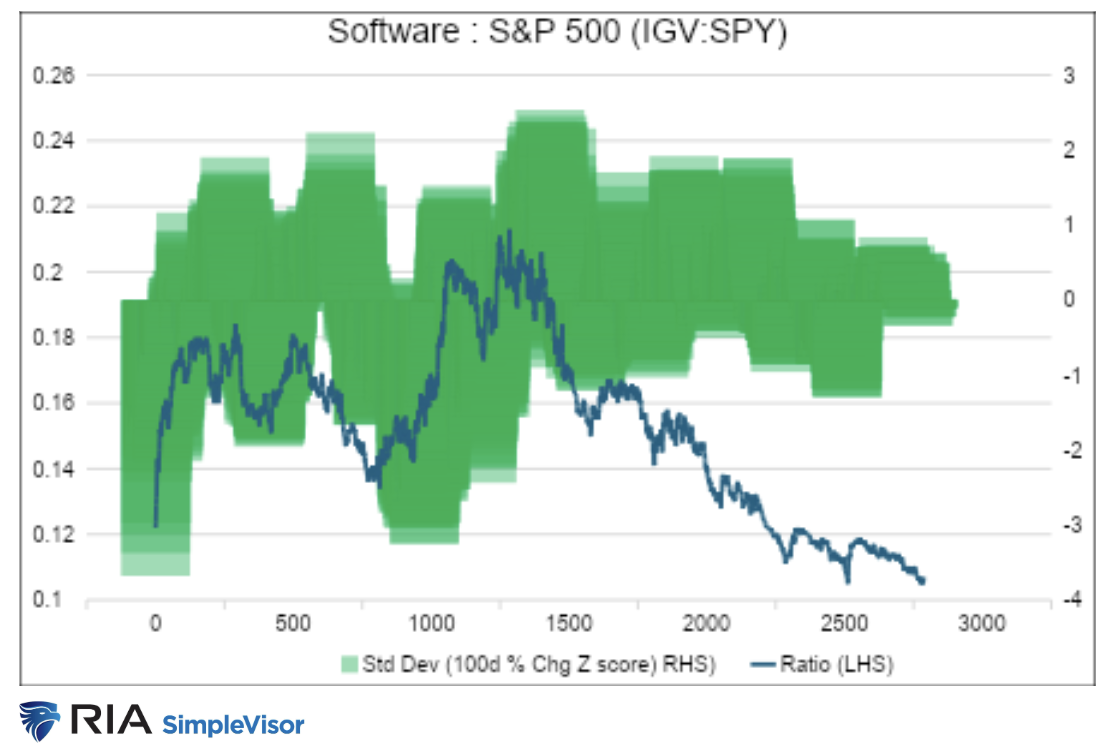

The statistical divergence is also significant when comparing IGV to SPY, which tracks the S&P 500.

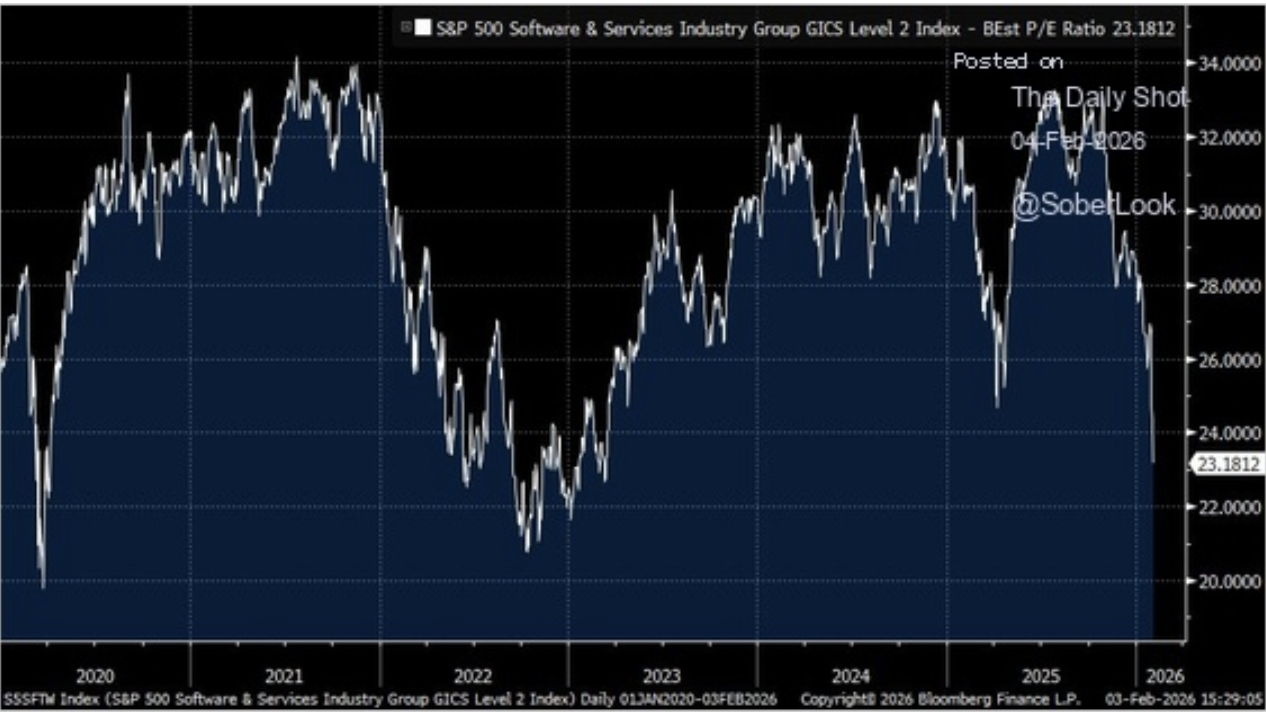

For fundamental context, we share the graph below from the Daily Shot. The P/E ratio of the software sector has fallen rapidly over the last few months, from 34 to 24. For context, the utility sector has a P/E ratio of 21.

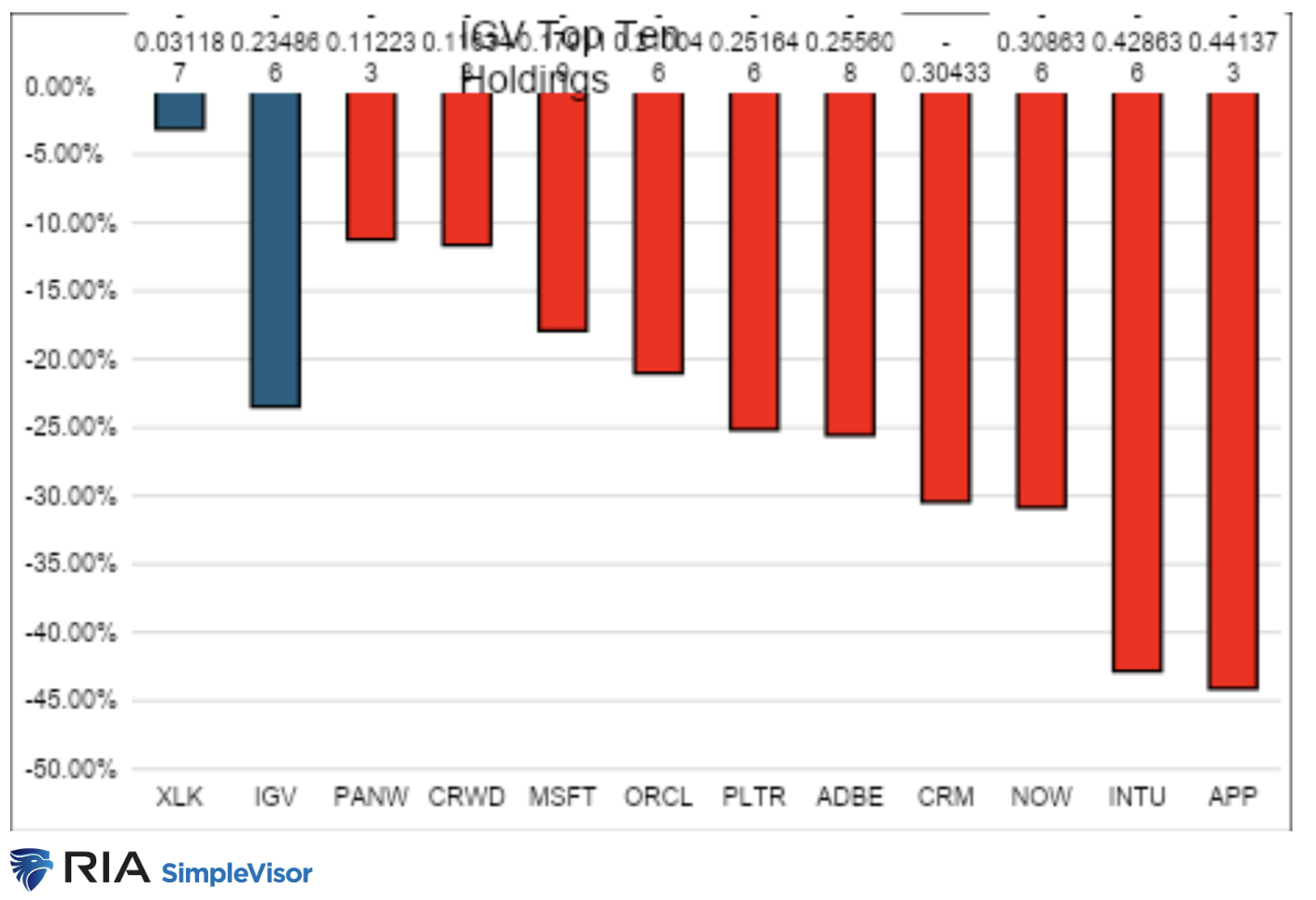

Lastly, we present the year-to-date returns of IGV's top 10 holdings. Based solely on the returns below, the market is betting that Intuit (INTU) and Applovin (APP) have the weakest moats and that Palo Alto Networks (PANW) and Crowdstrike (CRWD) will be the least negatively affected by potential AI competition.

Summary

Like most narratives, the SaaSpocalypse has some truth and some falsehoods. There is also a large degree of speculation buried within it. Furthermore, the truth shouldn’t be applied broadly to all software companies and their products. AI will make some software companies more profitable and strengthen their moats, while other companies may fail as competition becomes fierce. The goal for an investor is to accurately identify who the winners and losers will be. This is not a simple task, but doing so can provide significant rewards if your research proves correct.

We caution that market rotations have been volatile, with many relationships — such as those shown earlier — remaining statistically overstretched. While that may provide comfort to some, we recognize that in a market where narratives are this powerful, relationships can become even more divergent. If you are inclined to invest in the software sector, we recommend taking small starter positions with defined stop-loss levels. This way, if you are too early, losses are minimal. If rotations begin favoring software stocks and the bearish narrative fades, the evidence may warrant increasing those starter positions. Trade with caution.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.