Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

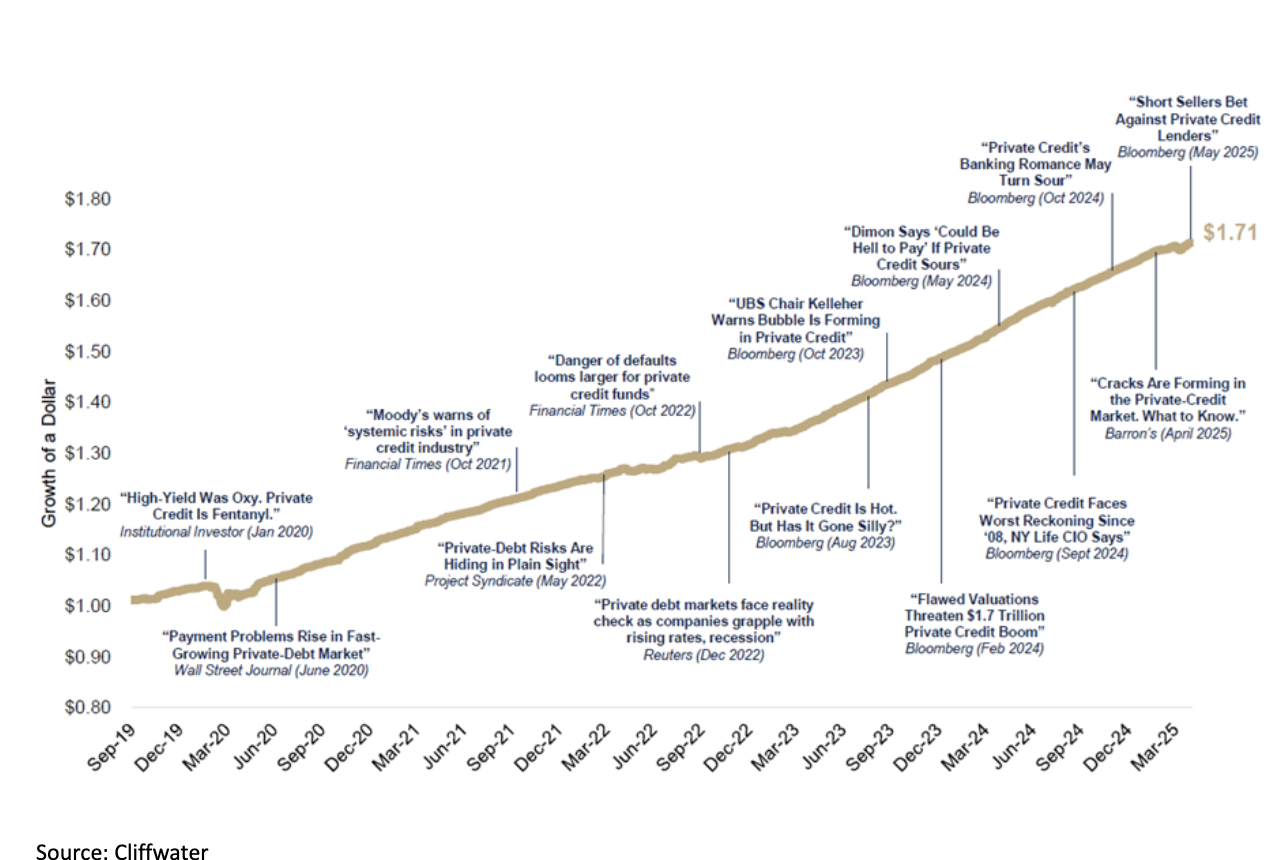

The bankruptcies of Tricolor Holdings and First Brands Group drew significant attention across private credit markets in the fall of 2025. Tricolor, a subprime auto lender, was accused of pledging the same loans multiple times, ultimately liquidating with over $1 billion in outstanding debt. First Brands, an auto parts manufacturer, collapsed following allegations of capital misappropriation and complex off-balance-sheet financing arrangements.

The resulting headlines prompted creditors and market participants to increase regulatory scrutiny and reinforce due diligence practices. A prevailing concern emerged that instances of fraud might not be isolated, but rather indicative of systemic issues within the broader private credit market. However, during these periods of market distress, private lenders who structured loans that sit high in the capital structure (i.e., they are first to be paid back in the event of a default) and are backed by the collateral of an underlying business were mostly protected from significant disruptions.

This dynamic demonstrated the value of owning senior-secured, collateral-backed loans due to their greater protection against defaults. Many private lenders issuing these types of loans maintained strong underwriting requirements and avoided First Brands and Tricolor due to their concerning financial situations. Though headlines raised alarm about the broader private credit space, it is important for investors to remember the benefits of holding these specific loans in the capital structure. Not only are they senior-secured and collateral-backed, but also provide attractive yields and inflation protection through their floating-rate nature. Ultimately, these unique components continue to make this area of the private debt asset class attractive, especially looking ahead.

The Advantages of Senior-Secured, First-Lien Loans

The landscape for private debt has evolved, but senior-secured loans continue to offer several benefits.

Risk Mitigation

Private debt offerings most commonly take the form of senior-secured, first-lien loans, which occupy the highest priority position in a company’s capital structure. This means the lender holds a primary claim on specific collateral, such as buildings, inventory, or accounts receivable, that backs the loan. In the event of a borrower default, the lender has the legal right to seize these assets before other creditors are paid, significantly reducing the risk of loss. This structure offers a more secure investment than subordinated or mezzanine debt, which is generally unsecured and ranks lower in the capital hierarchy, just above equity.

Sponsor Backed

Senior-secured private credit continues to appeal to investors because of its unique structure and the alignment of interests it fosters between lenders and borrowers. Lenders often work directly with borrowers — frequently private equity companies or “sponsors” — which encourages thorough due diligence and ongoing monitoring. This close relationship frequently results in stronger covenant protections and more customized loan agreements, allowing lenders to manage risk better and respond proactively to any signs of borrower distress.