Most investors, from grandma to the mightiest sovereign wealth funds, own bonds to help steady their portfolio and provide a ready reserve for spending. So, it’s notable when prominent voices start questioning their safety.

Everyone from Ray Dalio and Janet Yellen to Jamie Dimon and China has worried recently that the US’s mounting debt and unruly deficits could sour investors on Treasuries. There are also concerns about companies loading up on debt that some will struggle to pay back.

These fears about Treasuries and corporate bonds strike at the heart of most fixed-income portfolios. Some market watchers have even suggested investors lighten up on bonds in favor of gold, stocks or private assets. But there’s a big world of bonds to choose from. The safest among them still offer the protection investors expect — certainly more protection than risk assets — even against falling Treasury prices or rising corporate debt defaults.

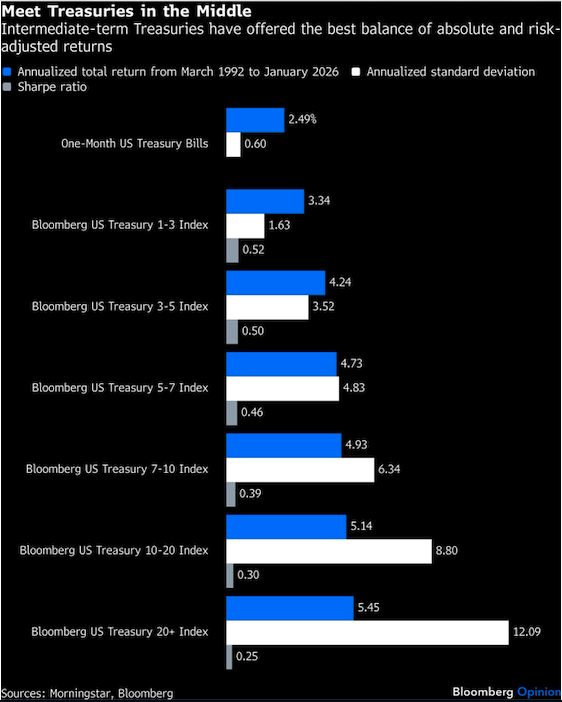

Bond investors have two big choices to make. The first is how long to lend. Interest rates and bond prices move in opposite directions, and the longer the term, the more sensitive bonds are to changes in rates. Investors in long-term Treasuries were reminded of the danger when rates ticked higher beginning in 2020 and then kept climbing as the Federal Reserve tightened monetary policy to fight inflation.

It got ugly. The Bloomberg US Treasury 20+ Index, which tracks the longest-dated Treasuries, declined by a staggering 48% from August 2020 to October 2023, including interest, a downdraft resembling the worst stock market collapses. That experience no doubt animates some of the current anxiety around Treasuries, but the pain was not universally shared. Shorter-term Treasuries held their value just fine, all things considered. The Bloomberg US Treasury 1-3 Index was down just 2%.

Risk and return are usually closely related in markets, but chasing term risk with longer-dated Treasuries has not necessarily paid off. Investors would have nearly doubled their return since 1992 by moving from one-month Treasury bills to five-year Treasuries. Extending further, however, would have paid only modestly more, resulting in significantly worse risk-adjusted returns. And that was mostly during a period of declining interest rates, which disproportionately benefits longer-term bonds. That history suggests the sweet spot for maximizing both absolute and risk-adjusted returns lies somewhere in the intermediate-term range.

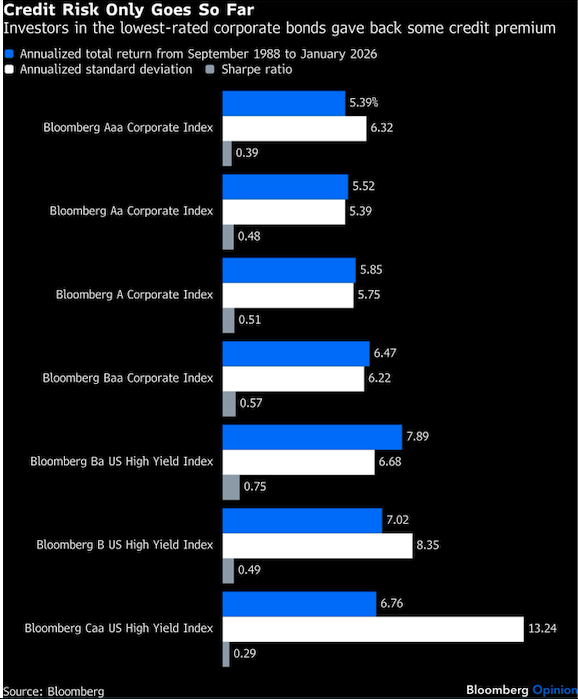

The second choice is about credit, or the quality of the borrower. The US government still tops them all. It’s backed by the biggest economy, deepest financial markets and a vast capacity to raise revenue. Companies don’t have the same privileges, which makes them riskier borrowers and requires them to pay a higher yield than Treasuries — in bond speak, a credit spread.

The risk is real, particularly when lending to the weakest borrowers, whose bonds can tumble as much as stocks during downturns. From the top of the 1990s internet bubble through the subsequent crash, bonds got a huge lift from declining interest rates, with Treasuries up 20% to 50% depending on maturity. Despite that considerable boost, the Bloomberg B US High Yield Index was down 11% from August 1999 to September 2002, and the Caa index (one rung lower) declined 43%.

As with term risk, taking more credit risk has not necessarily paid off. Since 1988, investors would have received an additional 1.1 percentage points a year by moving from Aaa, the highest-rated corporate bonds, to Baa, one notch above high yield. They would have captured an additional 1.4 percentage points by dropping down one rating to Ba, the highest rating among high yield. Any lower, though, and absolute returns start to fall off. Here again, the sweet spot seems to be closer to the middle of the rating ladder.

There are numerous low-cost funds that track indexes blending short- to intermediate-term Treasuries (or US government bonds more broadly) and high-quality corporate bonds. Those who want to reach for higher premiums can add a modest allocation to index funds that track high-yield corporate bonds, most of which cluster around Ba to B, the highest rating in the group.

The same approach to balancing risk and return can be applied to all bonds, whether US municipals or foreign government. There are exceptions: When 30-year Treasury yields topped 15% in the early 1980s, expected returns were hugely lopsided relative to risk because interest rates were far more likely to decline than rise from that level. The same was true when credit spreads blew out during the 2008 financial crisis — the massive yield over Treasuries was more likely to contract than widen further. There are also specialized bond strategies that can make sense in any environment, such as matching long-term liabilities with a reliable income stream from long-dated Treasuries.

So far, bond markets don’t seem worried about the US’s fiscal trajectory or corporate borrowing. The 10-year Treasury yield, at 4%, is only 0.4 percentage point higher than the federal funds rate, well below the historical average spread of closer to 1 percentage point. Credit spreads for both high-quality and high-yield corporate bonds are also historically low.

But if bond markets change their mind, and Treasury yields and credit spreads spike suddenly, as many fear, investors will be glad they didn’t stretch for more term and credit. And they’ll appreciate a thoughtfully constructed bond portfolio the next time risk assets live up to their name.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.