Decades of “regulatory creep” and onerous disclosure requirements have discouraged companies from going public, say leaders of the Securities and Exchange Commission. To revitalize American markets, they plan to pare back those demands, especially for smaller firms. “We need a reset,” Chairman Paul Atkins recently declared.

Although this narrative has a certain appeal, the SEC risks misdiagnosing the problem it’s trying to solve — and hence overlooking more pressing concerns.

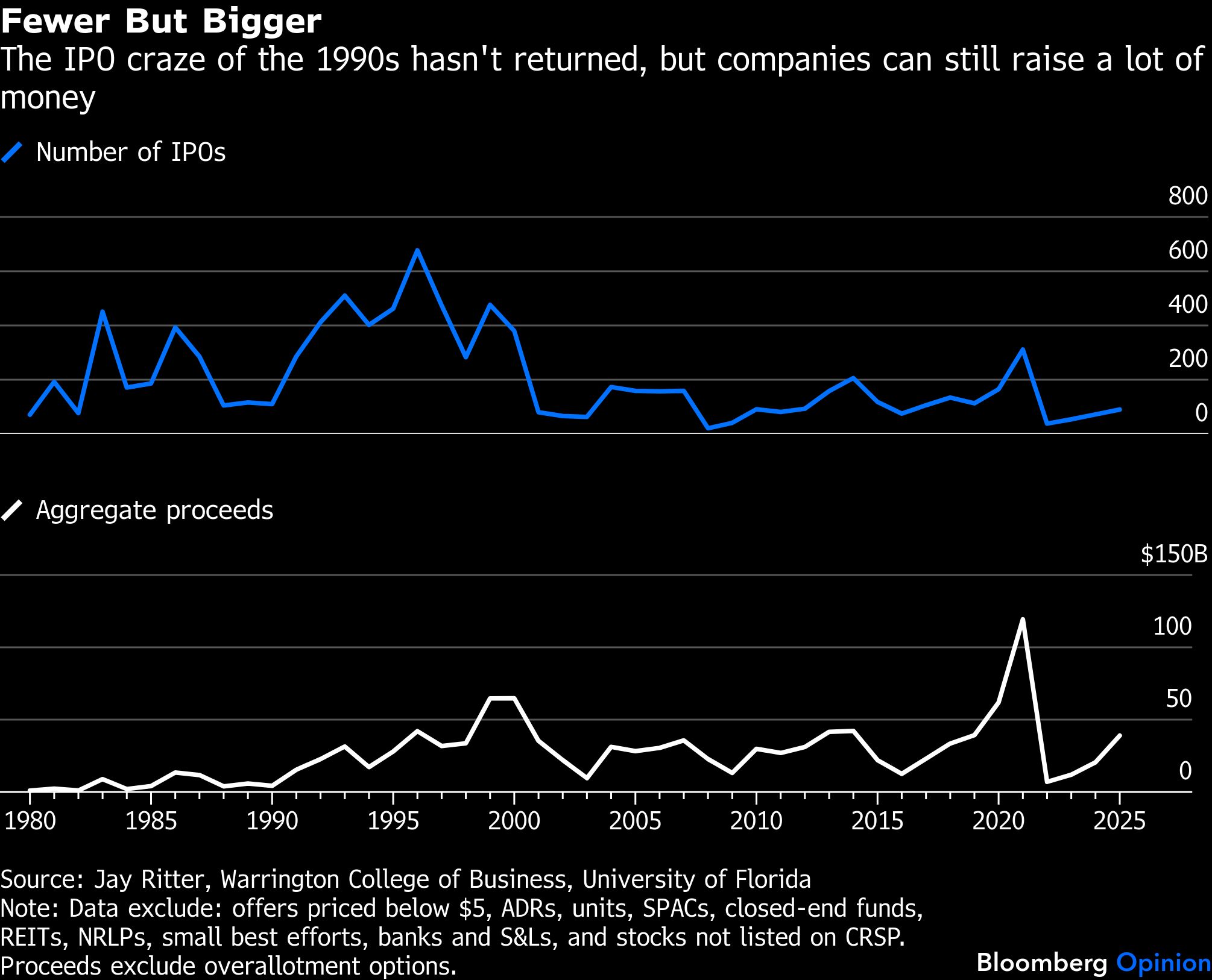

There’s no question that US markets have changed dramatically since Atkins first served on the commission’s staff in the 1990s. Total equity value has more than doubled as a percentage of gross domestic product, but there are some 40% fewer stocks. Today’s initial public offering candidates are often larger and more mature, with some already valued at tens of billions of dollars — or, in the case of Elon Musk’s conglomerate, more than $1 trillion. Increasingly, the market is made up of a smaller number of bigger companies.

It’s tempting to blame regulation for this dynamic. Expanding disclosures on topics as diverse as conflict minerals, cybersecurity and executive compensation have caused the average length of annual 10-K filings to nearly triple since 1996, making them harder to read and costlier to prepare. That in turn has conferred an advantage on bigger companies with more compliance staff. As Atkins said in a speech in December, “the path to public ownership has become narrower, costlier and overly burdened with rules.”

His proposed solution: Limit disclosures to those deemed financially material and let more firms qualify for the tailored rules reserved for the smallest ones.

These are reasonable goals, but they may not amount to much. A 2021 study estimated that all of the regulatory costs imposed since 2000 likely account for less than 8% of the decline in IPOs. Corporate filings have ballooned mostly because of rules related to fair-value accounting, internal controls and risk factors — topics already deemed financially material. Moreover, the SEC has already reduced the burdens for so-called smaller reporting companies and emerging growth companies.

By all means, the commission should look to further streamline things (as it has done repeatedly over the past 20 years). Companies can abide by federal securities laws without reporting their insider-trading guidelines annually, for instance, and mine-safety policies probably don’t need quarterly updates.

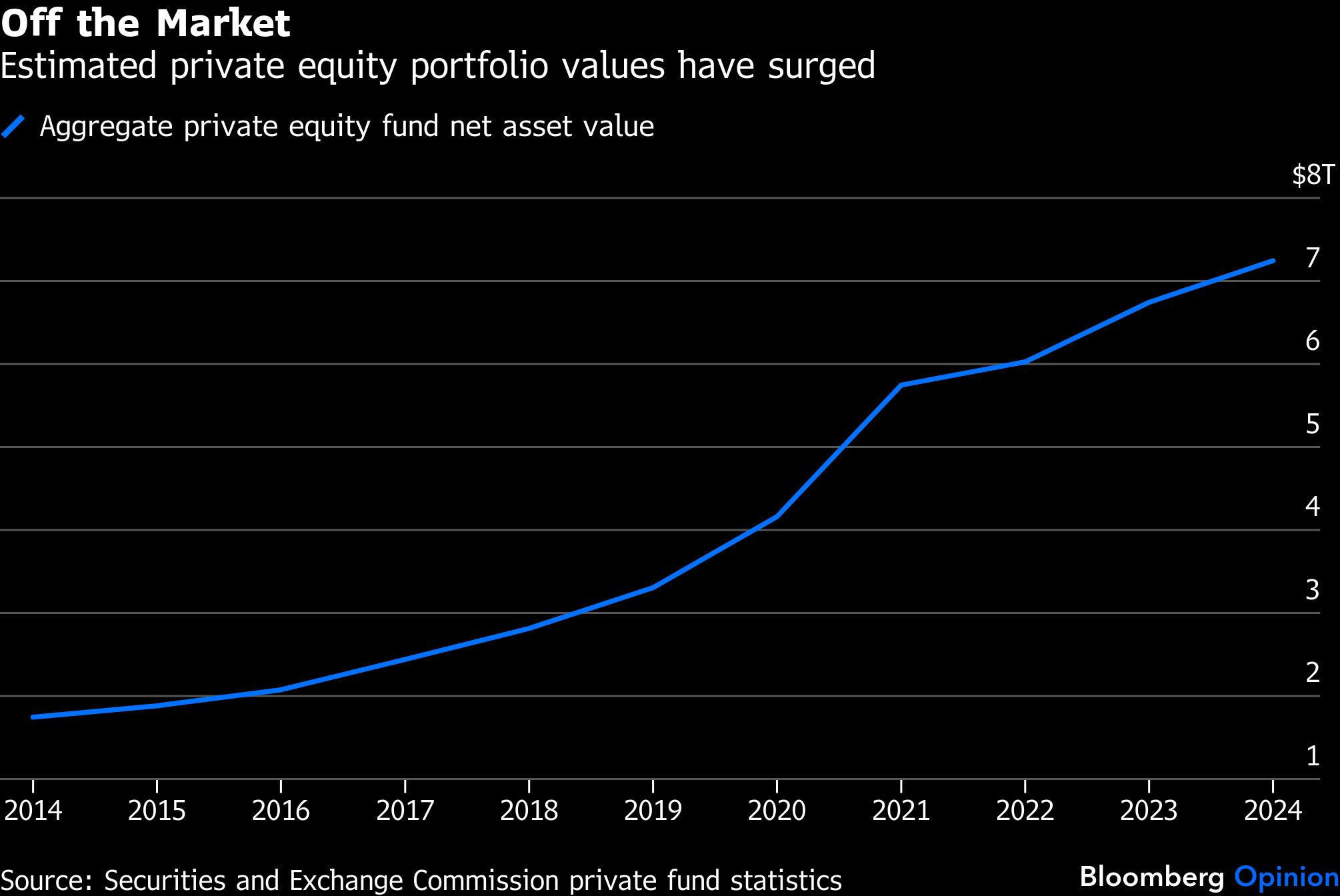

Yet markets have evolved for complex reasons. Most pertinently, the rise of private equity and credit funds — combined with a decade of zero-percent interest rates — gave US companies access to easy financing with little public scrutiny. More than $4 trillion has poured into such funds in recent years. As they increasingly seek capital from retail investors and retirement savers, instead of just institutions, the SEC needs to devote more of its attention and resources to overseeing them.

To begin, the commission should require better disclosures about liquidity and valuations at registered funds, such as ETFs, business-development companies and interval funds that already own private assets. Its examiners need to clamp down on bad actors, such as funds that artificially inflate the value of these rarely traded assets to increase fees.

Another priority should be reforming disclosure rules for unregistered private funds or securities that market themselves to individuals. Even institutional investors in such assets have long had to haggle for information, with the largest and most sophisticated often receiving favorable terms and additional data. If policymakers expand direct retail access, the SEC should mandate standardized disclosures to level the playing field. It should also revisit its previous — and failed — effort to require such funds to detail quarterly expenses and fees as well as conflicts of interest.

Atkins says that capital markets are “expressions of our national character” — in particular, the American tendency to “innovate endlessly and restlessly.” He’s right. The SEC needs to keep up.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by