The public loves to hate short sellers, the investors who profit from declining securities’ values. Their bad reputation is mostly undeserved. In reality, many provide a valuable service, taking the other side of frauds and bubbles, and generally helping drive prices toward a semblance of fair value. What’s more, they do this despite inherently poor odds: Statistically speaking, the market goes up more than it goes down. A healthy market needs short sellers, and in recent years they have gone missing.

Fortunately, there are early signs that’s changing. “The lost art of short selling has come back, and it’s absolutely critical this year,” Third Point LLC Chief Executive Officer Dan Loeb said last week at the iConnections Global Alts hedge fund conference in Miami Beach.

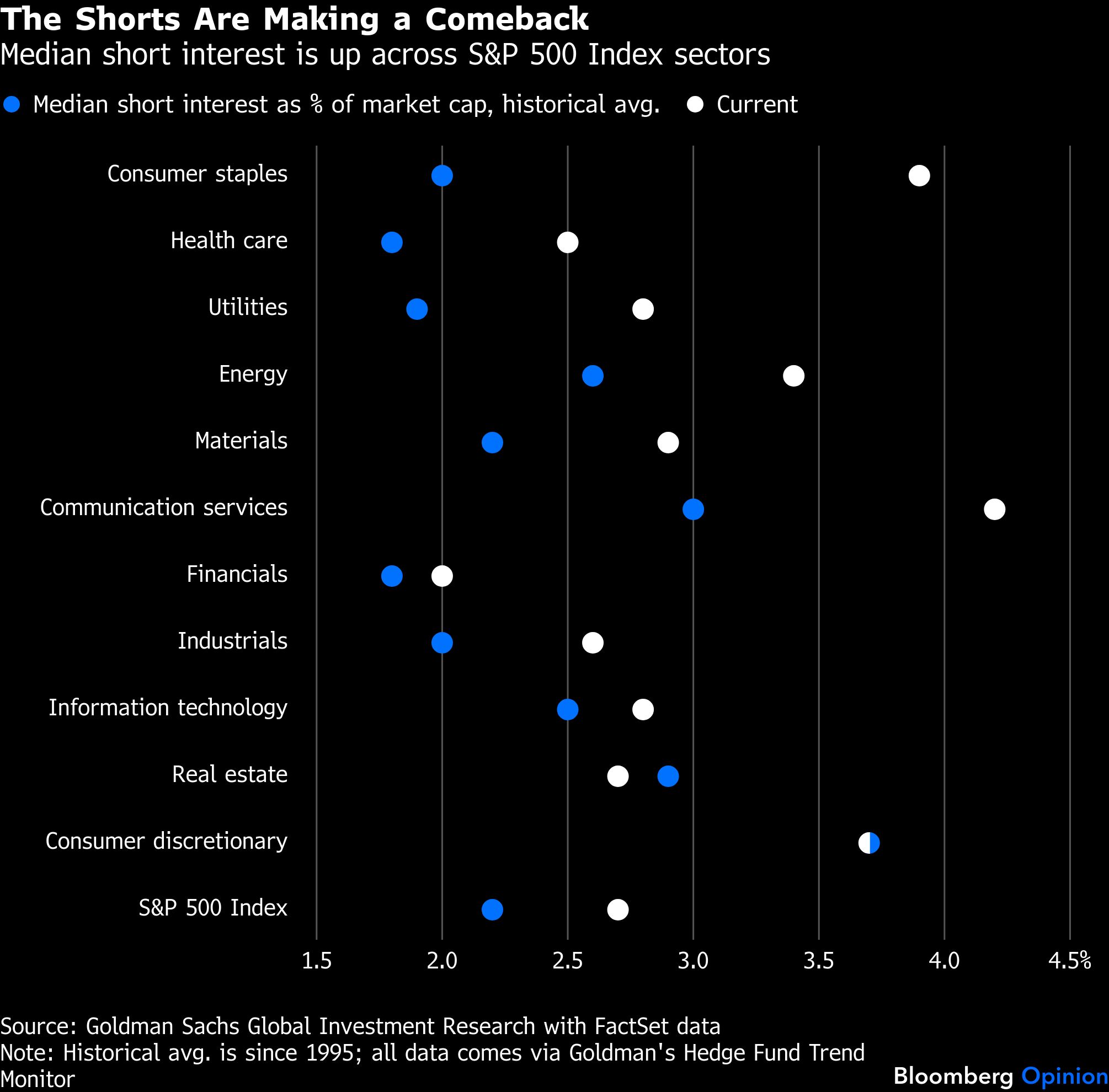

Loeb is right. The median S&P 500 Index stock has seen its short interest as a percentage of market capitalization roar back in the past few quarters to sit near the highest in around a decade, Goldman Sachs Group Inc. highlighted recently. Median short interest is well above normal in every sector of the index, and it’s particularly high for consumer staples and health care (by their own standards).

Combined with the recent caution across markets, this is another sign that investors are leaving behind the momentum-driven excesses that dominated the market from 2020 till late last year. Shorting was downright dangerous in that environment, now hedge funds smell opportunity again — and that’s just as well.

Since the release of ChatGPT in November 2022, the S&P 500’s price-earnings multiple has risen by around a whole number every six months or so. The ever-expanding multiple was on an unsustainable path, so it’s reassuring to see investors become more discerning and focused on company fundamentals. Rather than giving firms the benefit of the doubt for good stories, they’re scrutinizing cash flows again and starting to punish even the most dominant growth stocks for unwieldy capital expenditures with uncertain returns.

Short selling had been fading essentially since the financial crisis, though the retreat accelerated in recent years. For much of the 2010s, near-zero interest rates and a booming tech ecosystem undergirded the longest bull market in history.

The momentum paused only briefly for the Covid-19 pandemic before monetary and fiscal authorities uncorked coordinated stimulus, including the famous “stimmy check” cash transfers. Retail interest in buying stocks exploded, giving rise to the meme stock frenzy that many saw as the death knell for short selling: A group of individual investors coordinating on the r/WallStreetBets corner of Reddit squeezed the bears, leading to massive losses for Melvin Capital, which eventually closed down. In pop culture, the Reddit investors were celebrated as populist heroes who toppled big bad professional money managers. Then came ChatGPT and the frenzy around artificial intelligence.

Even leaving the Reddit short squeezes aside, many short sellers recognized it was suicide to bet against these forces. While short sellers try to unearth fundamental flaws in companies’ accounting or business models, they can sometimes be helpless against liquidity-driven markets based to a significant degree on narratives and expanding market multiples.

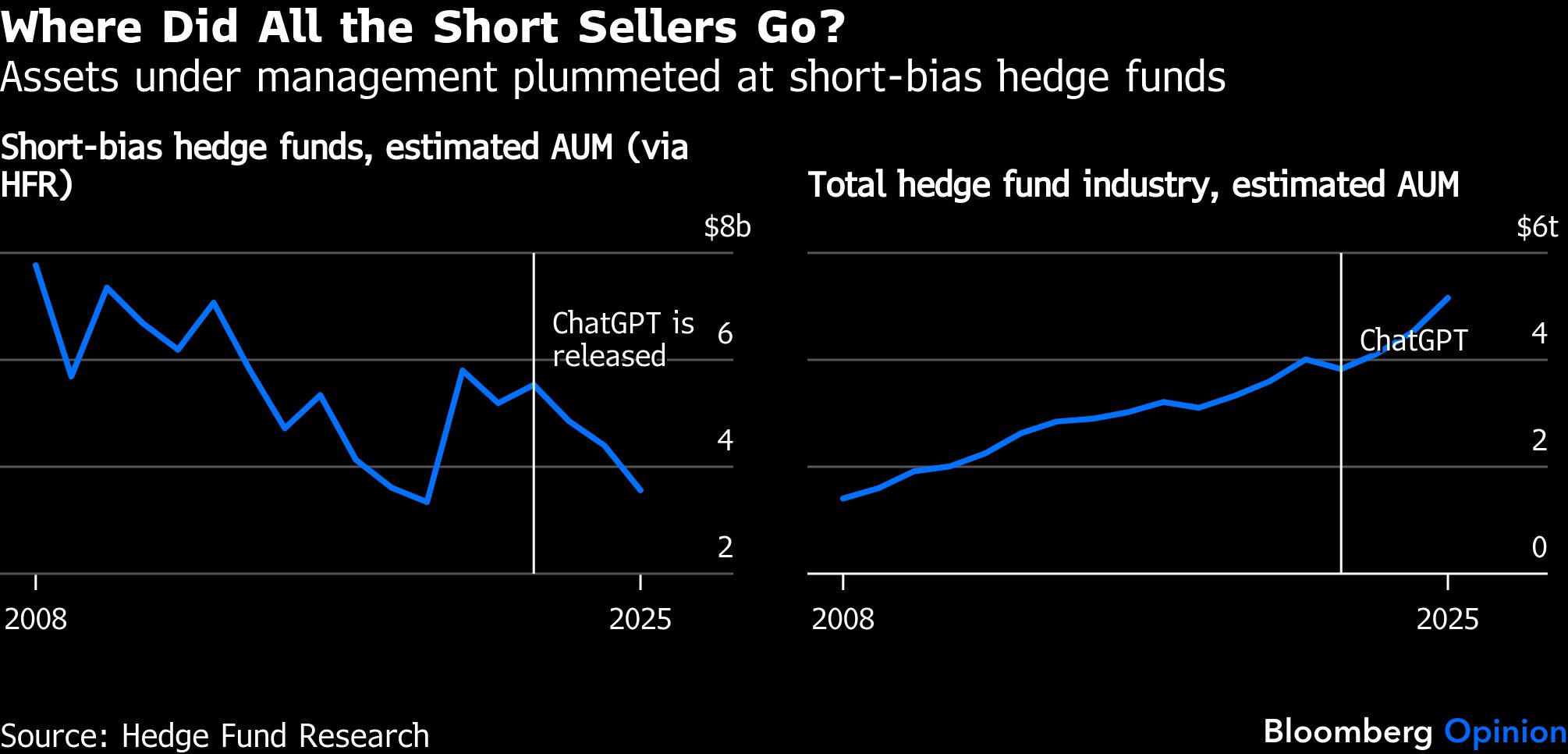

As data from Hedge Fund Research shows, the assets under management of short-bias hedge funds plummeted 31% to $3.6 billion in the five years through 2025, even as the broader hedge fund industry continued to grow. The number of short-bias funds tracked by HFR fell to 10, down from 14 in 2020 and 48 in 2010. Legendary short-seller Jim Chanos shuttered his hedge fund, and Carson Block’s Muddy Waters Capital LLC even launched its first long-only fund during this time.

We shouldn’t get ahead of ourselves and predict a massive short-seller renaissance. What the statistics about median short interest don’t show is that hedge funds are still pretty queasy about taking very concentrated bearish bets on single names. Goldman analysts including Ben Snider see that as perhaps “a lesson from recent short squeezes” (the Reddit fiasco).

But even a modest rebound in short-selling activity is a welcome development. As I’ve written before, the retail-driven, long-only, high-momentum stock market of 2023-2025 was headed toward the bubble valuations of 1999 — a recipe for a boom and bust scenario that would have ended badly for the market and economy. Instead, the market seems to be taking a breather as market P/E multiples drift toward slightly more palatable levels and individual stocks search for fair value. If we get there without a dot-com style trainwreck, short sellers may be part of the reason why.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin