Credit investors are unwinding long positions worth tens of billions of dollars and jumping into hedging trades.

Bullish bets in high-grade credit-default swap indexes have plunged by about a fifth in recent weeks, based on data compiled by Bloomberg. Separate indicators by BNP Paribas SA, which also track metrics like the amount of cash investors hold or the volatility of their portfolio, show that investors are now short risk.

Conflict in the Middle East and worries about the disruptive impact of artificial intelligence are pushing money managers to reduce long positions that had insulated the safest part of the credit market from most risks over the past year. They’re doing so in an unsettled period, when markets can swiftly reverse direction depending on the headlines of the day.

“There is a lot of nervousness and a lot of uncertainty and people are afraid,” said Viktor Hjort, global head of credit strategy at BNP Paribas. “Many of them have already sold and dumped the risk.”

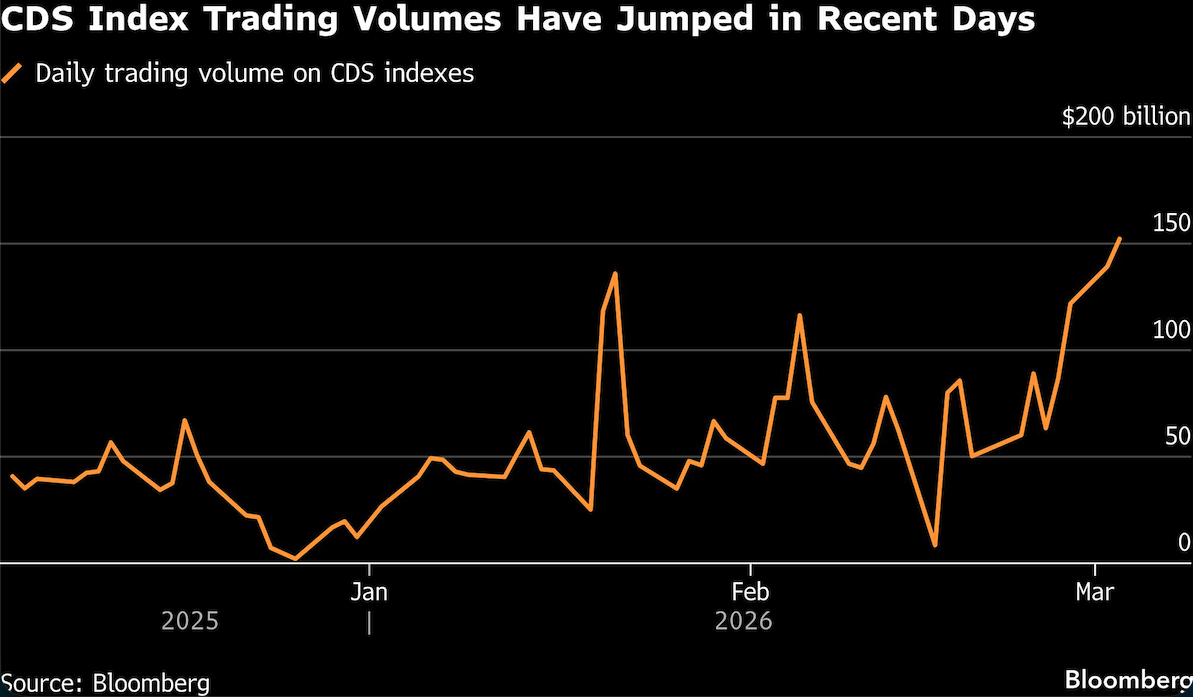

In credit, the mood shift is most clearly seen in CDS indexes. Formerly just a hedge against companies going bust, these gauges have become a popular way to take a broad view on market direction because of their high levels of liquidity. They are also able to react to news much faster than corporate bonds, which are still the main building block of a credit portfolio.

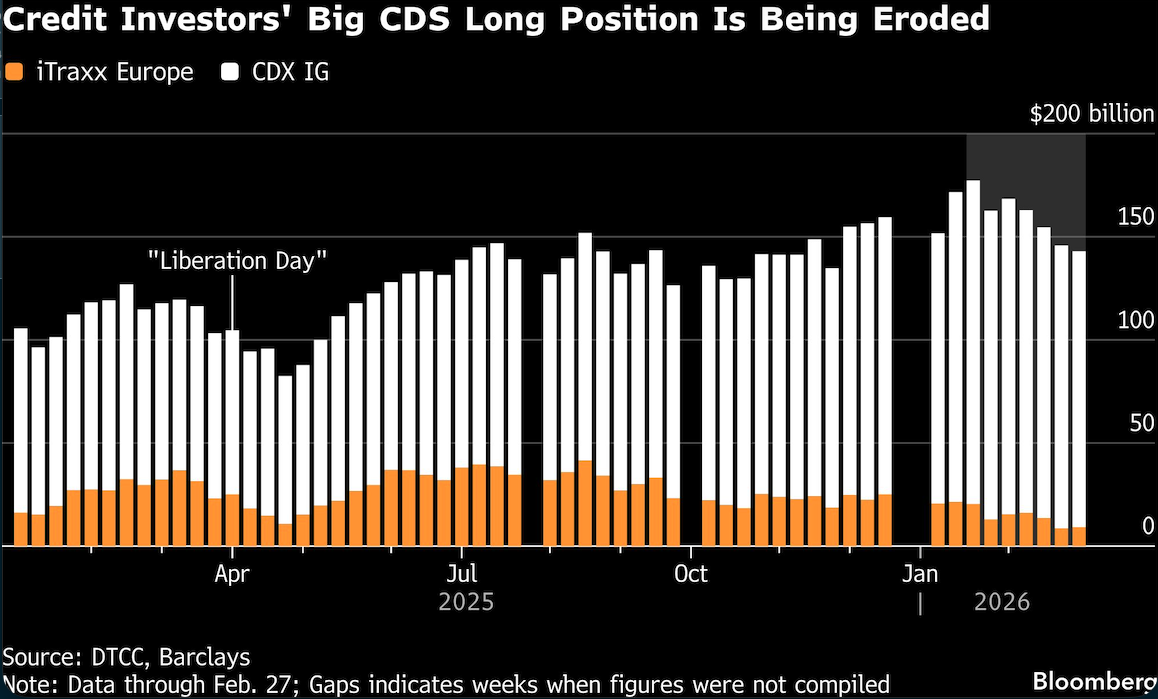

Bullish bets in CDS indexes have been eroding over the past few weeks amid anxiety over the software sector, according to DTCC data compiled by Barclays Plc. The weekly data doesn’t yet reflect the impact of war in Iran, though a jump in CDS index spreads amid high trading volumes suggests the positioning shift is ongoing.

Spreads on high-grade CDS indexes are widening further on Friday, with the iTraxx Europe index up more than 2 basis points to about 60.5 basis points, its highest level since last June, and the CDX IG index up 1.4 basis points to 57.3 basis points.

A separate US credit positioning indicator run by BNP Paribas fell below zero in the past few days, while a European measure sank deeper into negative territory, indicating that investors are now short risk. The gauges include metrics like cash balances on funds, CDS positioning and dealer inventories.

This rapid reversal is hitting valuations across different parts of the market. Worries about the impact of AI were already rattling private credit and leveraged loan markets, which have more exposure to software companies, but those anxieties have metastasized into a full-blown retreat that is now dragging down even the safest corners of credit.

Risk premiums on a Bloomberg index of global high-grade corporate bonds this week approached their highest level since last summer. Total return is set for its biggest weekly hit since late 2024 as investors absorbed the double whammy of wider credit spreads and jumping government bond yields on fears that the war will stoke inflation.

The turnaround in positioning has also made hedging — seen by many investors as a waste of money over the past year — a hot topic again.

“Given absolute spread levels and so much uncertainty, you’ve seen increased hedging for sure whether being short index outright or buying credit options to protect the downside,” said Nachu Chockalingam, head of the London credit desk at Federated Hermes.

The dynamics of systematic trading in the CDS market are also playing a part in the swift unwind.

As credit market volatility has been low and spreads have been tight, systematic models would have indicated that higher levels of exposure were necessary, according to April LaRusse, head of investment specialists, Insight Investment. “Now that volatility has increased and spreads have widened, the whole thing goes into reverse,” she said.

To be sure, shunning risk could end up being a contrarian indicator if the war in the Middle East ends up being relatively brief.

“If positioning is short, as it is right now, we would argue that it means that most people who need to sell have sold,” said BNP’s Hjort. “If news starts to turn good, there’s a lot of people who need to cover their shorts or who need to start buying again,” he said.

Still, with so much uncertainty over the duration, size and outcome of conflict in the Middle East, and questions about AI disruption unresolved, fund managers are likely to position conservatively, even if they return to buying.

“Spreads are priced too optimistically, even without accounting for the recent geopolitical volatility,” wrote Steve Caprio, head of European and US credit strategy at Deutsche Bank AG, noting that US and European high-yield bonds have enjoyed long stretches of positive monthly total returns.

“Exceptional winning streaks of this magnitude usually end with a thud.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.