Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The U.S. stock market is heavily concentrated in a handful of technology companies. The Magnificent Seven – Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla – account for just over 30% of the U.S. stock market’s total value, and they are all tech firms.1 Many investors and commentators find this alarming, arguing that such concentration makes the market riskier and that investors should take defensive action by rebalancing toward safer assets or equal-weighted strategies.

We think the concern about concentration is misplaced. Two recent papers, and our own 2021 research article – “Are Market Capitalization Weighted Indexes Too Concentrated in the Biggest Stocks?” – make a compelling case that concentration is not a useful signal of higher market risk or lower expected returns. Both theory and evidence suggest that investors who act on concentration fears are likely to hurt their own performance, particularly versus an investment strategy of dynamic asset allocation based on more direct estimates of the market’s expected excess return and risk.

We’ll explain the main findings of these articles and conclude with a discussion of what we think investors should be concerned about: the extremely low long-term expected return of the U.S. stock market.

The Market Is Concentrated – but That’s Not So Unusual

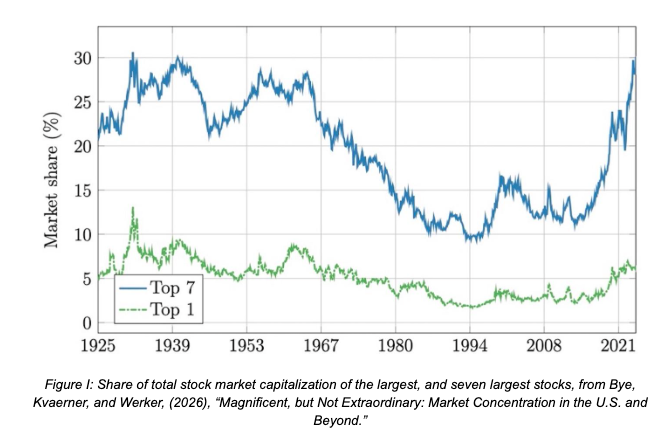

There is no denying the facts: the U.S. equity market is more concentrated today than at any point in the past quarter century. Kritzman and Turkington document this in their paper “The Fallacy of Concentration” (2025). They measure concentration using a measure of the effective number of stocks in the market2 and show that this measure has fallen to near its lowest level since 1998 for the S&P 500.

But when they extend the analysis further back, a different picture emerges. Current industry-level concentration “closely matches other prior low points in history. It is not unprecedented.” The market was at least as concentrated in the 1930s, 1950s, and 1960s as it is today.

Bye, Kvaerner, and Werker reach the same conclusion in their paper “Magnificent, but Not Extraordinary” (2026). They construct the history of U.S. market concentration back to 1926 and find that the current weight of the top seven firms is within historical norms:

From the 1930s to the 1960s, seven firms held comparable shares. The peak occurred in May 1932, when AT&T, Standard Oil Company, Consolidated Gas Company of New York, General Motors, DuPont, R.J. Reynolds Tobacco Company, and United Gas Improvement Company together accounted for roughly one-third of total value.

Far from being a uniquely American or uniquely modern phenomenon, concentration appears to be a pervasive feature of equity markets around the world. Bye et al. show that, when measured by the fraction of firms needed to account for one-third of total market capitalization, the U.S. is not an outlier:

The U.S. equity market is not more concentrated than other developed markets…This share is similar in countries with diverse industrial structures and stock market regulation…Market concentration is a global equity feature, not a uniquely U.S. issue.

Many active investment managers and some academics have argued that the growth of index fund investing has increased market concentration. But, as the data above make clear, the stock market experienced levels of concentration comparable to today’s long before the first index fund was launched in 1976 – and long before indexing captured a meaningful share of assets. The claim doesn’t survive contact with the historical record.

Our take on the Question From 2021

In July 2021, we addressed the concentration issue in an article titled: “Are Market Capitalization Weighted Indexes Too Concentrated in the Biggest Stocks?” We made three arguments for why we didn’t think concentration at that time was a concern. (Note that concentration continued to increase in the U.S. over the past five years since we wrote that article, with the top seven companies going from a bit over 20% to just over 30% today.)

- The S&P 500 overstates the problem. A global cap-weighted portfolio is roughly half as concentrated.

- Equal-weighting is an active bet, not a free lunch. Cap-weighting is the only portfolio all investors can hold simultaneously; deviating from it requires finding someone to take the other side.

- The level of concentration had extremely modest consequences for efficient returns. The largest stock needed only about 0.08% more expected return than the 100th largest for cap-weights to be optimal – a trivially small hurdle. While market capitalization weighted indexes were, and currently are, more concentrated than usual, we argued that they are still very well diversified based on the small amount of extra expected return the biggest stocks would need to offer to compensate for their weight in the index.

Why Concentration Is Normal

Both Kritzman and Turkington and Bye et al. offer compelling explanations for why concentration should not alarm investors.

Kritzman and Turkington emphasize that large companies are intrinsically more diversified and safer than small ones – they operate across more geographies, sell more products to more customers, have better access to capital, attract stronger management, and face more regulatory and investor scrutiny. They also argue that concentration is a natural consequence of the power law governing firm size distributions: “growth is self-reinforcing,” and “to take steps to counteract concentration, one should have reason to believe that the factors that drove growth in the past no longer apply.”

Bye et al. formalize this intuition with a simple but powerful model. They show that, if firm values follow a standard geometric Brownian motion with a common market factor and firm-specific shocks – the textbook model underlying option pricing and much of modern finance – the resulting concentration matches what we observe in the data. Starting from identical firms with 27.5% annual volatility, after 50 years, about 1% of firms account for one-third of total market value, which is right in line with historical experience.

Idiosyncratic volatility…induces valuation concentration…Expected returns do not matter for concentration, as they increase the expected value of all firms equally and have no impact on relative valuations.

The insight is that you don’t need to invoke bubbles, behavioral biases, market dysfunction or index investing to explain why a small number of companies dominate the index. Normal idiosyncratic risk, compounded over time, naturally produces a heavy-tailed distribution of firm sizes. Concentration is what a well-functioning market should look like.

Bye et al. also show that valuation concentration tracks earnings concentration. The share of firms needed to account for one-third of aggregate revenue, EBITDA, net income, and cash flow has fallen over time in step with market capitalization concentration. Today’s large firms are large in part because they genuinely earn an outsized share of corporate profits, not merely because investors have bid up their prices relative to fundamentals.

In support of Bye et al.’s observation, the Mag 7 technology stocks in aggregate are currently trading at 35x last year’s earnings. The S&P500 technology sector index is also trading at the same multiple, while a mid-cap tech index trades at 45x earnings.3 These relative price-earnings multiples fly in the face of arguments made by indexing skeptics that market-capitalization indexing has inordinately inflated the valuations of the largest companies.

Concentration Does Not Beget Risk

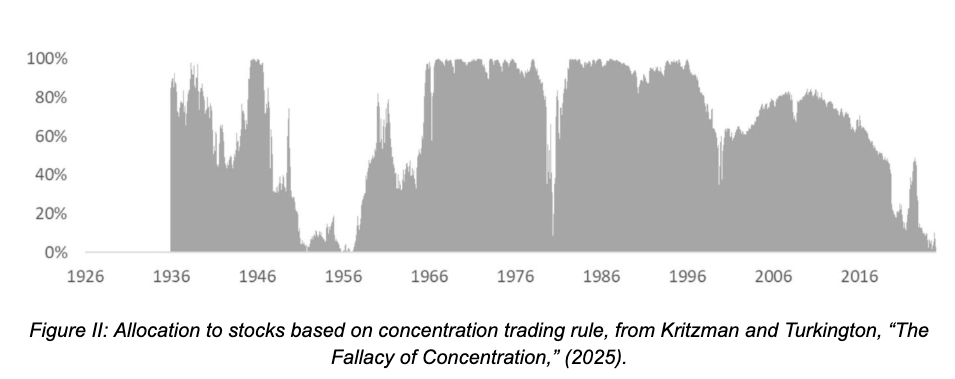

Establishing that concentration is not unprecedented is important, but the more consequential question is whether concentration makes the market riskier. Kritzman and Turkington attack this question from multiple angles, and their findings are strikingly consistent: concentration has essentially no relationship with subsequent risk or return.

Their most vivid test is a dynamic trading strategy that reduces equity exposure when the market becomes more concentrated and increases it when concentration falls. This is precisely the strategy that a concentration-worried investor would follow.

The results are not supportive for the concentration-risk thesis. Compared to a buy-and-hold strategy with the same average equity exposure of 68%, the concentration-sensitive strategy:

- Earned a lower average excess return: 4.7% vs. 5.6%

- Had higher volatility: 12.1% vs. 10.7%

- Delivered a substantially worse Sharpe ratio: 0.39 vs. 0.52

As Kritzman and Turkington put it: “This rule of investing less in the stock market when it is more concentrated reduces return and increases risk compared to the buy-and-hold strategy that allows concentration to evolve naturally.”4 The buy-and-hold approach “generated more than twice as much wealth as the dynamic strategy during this period, and it did so with less risk.”5

A more anecdotal take on the question is provided by author and WSJ columnist Jason Zweig in his excellent recent article on concentration, “The Big Scary Myth Stalking the Stock Market.” He notes that AT&T was 12.7% of the U.S. market in June 1932 – far more than Nvidia today – yet investors who bought in at that peak of concentration went on to earn extraordinary returns. His point: concentration isn’t inherently dangerous, and the “numbers help counteract Wall Street’s latest myth: that today’s market, dominated by giant tech companies, is a monster that will stomp your index funds to bits.”

Kritzman and Turkington also compare the risk properties of large and small stocks directly. When the S&P 500 is divided into deciles by size and each decile is equally weighted (so that concentration within each portfolio is identical), the largest stocks consistently display the lowest volatility and the most favorable tail properties. The largest decile has the lowest volatility, the least fat tails, and among the best upside outcomes.

Perhaps most strikingly, when they divide the S&P 500 into quintiles of equal aggregate capitalization – so that the top quintile holds about 8 stocks and the bottom quintile holds about 328 stocks representing the same total market value – the risk properties are essentially indistinguishable:

Even though one must invest in 328 of the smallest stocks in the S&P 500 Index to capture the same fraction of the index’s capitalization as the largest eight stocks, the riskiness of these equal-capitalization quintiles is essentially the same. These results strongly contradict the notion that concentration affects risk.

Less concentration on concentration, more on valuation and risk

While we don’t find much reason to underweight our allocation to U.S. stocks based on the current high degree of concentration, we do believe that the valuation of the overall U.S. stock market today is consistent with low expected returns relative to safer fixed income investments. We believe the long-term expected return of U.S. equities is only about 1% higher than the expected return on U.S. Inflation Protected bonds (TIPS), and our estimate is roughly in line with the consensus of a dozen major investment houses.6

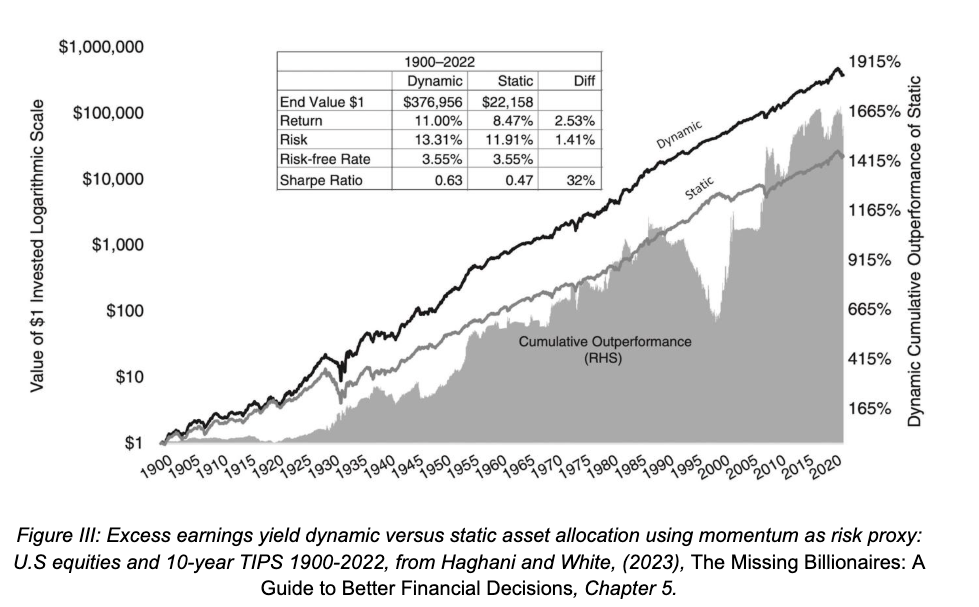

We think that dynamic asset allocation whereby you manage your exposure to equity markets guided by their relative expected returns and risk levels makes a lot more sense than managing your allocation according to the degree of concentration in the market. It is not only a much more comfortable approach to maintaining exposure to stocks over time, but it also has solid grounding in investing principles – and empirically, it has been an attractive approach to investing, though of course past returns are not necessarily indicative of future returns. The chart below, from Chapter 5 of our book, “The Missing Billionaires: A Guide to Better Financial Decisions,” suggests that dynamic asset allocation was an attractive approach to investing in the U.S. stock market over the past 100+ years.

Connecting the dots

We stick by our conclusion from five years ago that market capitalization weighting is the best index design available, offering the most efficient and diversified exposure to the broad stock market.

The evidence from both papers and our own research points clearly in the same direction: the current level of concentration is within historical and international norms; concentration has no meaningful relationship with subsequent risk or return; and the degree of concentration we observe is exactly what standard financial models predict from normal market dynamics. Investors who react to concentration by reducing equity exposure or deviating from market weights are, on the evidence, more likely to hurt themselves than help themselves. The best response to concentration is no response at all.

Victor Haghani is founder & CIO of Elm Wealth, a Philadelphia-based asset manager. James White is Elm Wealth’s CEO.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

1By contrast, thirty years ago, the industries of the biggest companies were, in descending order: industrials, energy, consumer staples, tech, pharma, consumer staples and tech.

2The reciprocal of the Herfindahl-Hirschman index, which is the sum of squared portfolio weights.

3We calculated this multiple from a sample of 20 randomly selected mid-cap technology stocks.

4Bye, Kvaener and Werker kindly shared four of their monthly concentration series (Bye et. al 2026) with us. We used three of the metrics – share of top seven stocks, fraction of market representing one-third of market capitalization and their FF48 industry concentration metric – to run a back-test from 1925 – 2025 for the US stock market. We found that the Sharpe ratios of dynamic strategies driven by their concentration series were indistinguishable from the Sharpe ratio of a portfolio that was always 60% in stocks and 40% in T-bills: 0.430 for the static asset allocation and 0.416 for the average Sharpe ratio of the three dynamic approaches based on each of their concentration metrics. While our results are less damning than those of Kritzman and Turkington, they certainly do not lend support to the strategy of reducing equity exposure when concentration is high.

5They further examine the question using panel regressions of sector-level performance metrics – return, volatility, downside volatility, and maximum drawdown – on the effective number of stocks, controlling for both year and sector fixed effects. The results are unambiguous: “concentration is not significantly related to variation in these performance metrics.”

6For more detail, see our capital market assumptions here.

Read more articles by Victor Haghani, James White

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.