Industrial Metals in a Security-First World

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

For many decades, international trade flourished with the United States as the lead architect. Global supply chains stretched across continents, capital flowed freely, and commodities were treated as cyclical inputs rather than strategic assets. With nations now turning their focus inward, however, that framework is no longer applicable.

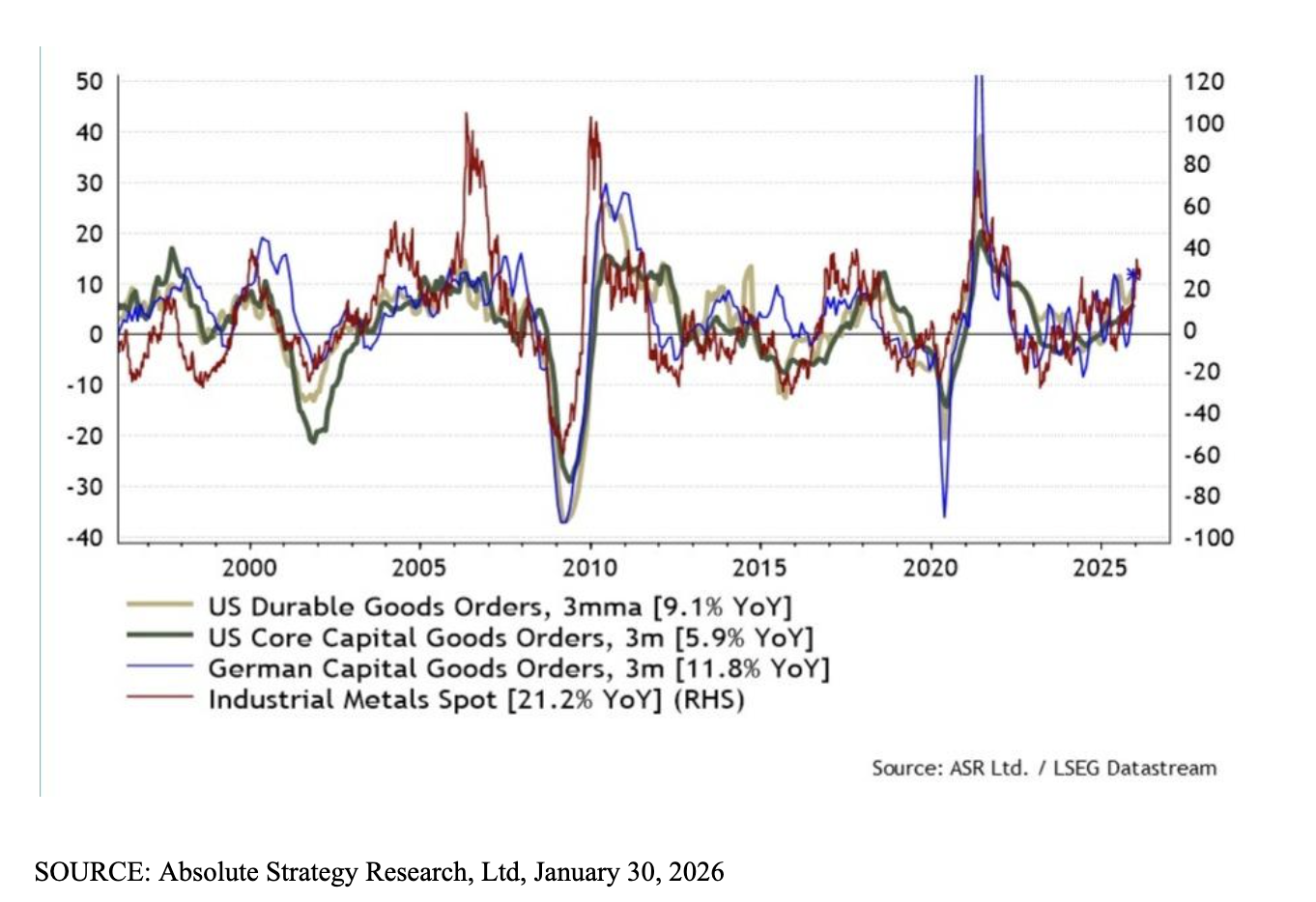

The global economy is now moving through what Absolute Strategy Research (ASR), an award-winning macro-strategy firm, has described as a rupture, meaning a break from the assumptions that governed the post–Cold War era. Governments are intervening more directly in markets and supply chains are being reshaped with geopolitical considerations at the forefront. Nowhere is this shift more visible than in industrial metals.

The rupture framework articulated by Ian Harnett and David Bowers of ASR captures this shift well. The global economy is prioritizing resilience, redundancy, and security. Supply chains are being shortened and strategic industries are being reshored. Governments are no longer content to act solely as regulators; they are increasingly becoming financiers, dealers, and stockpilers.

Electrification, energy security, defense spending, and digital infrastructure all depend on large quantities of copper, aluminum, silver, and other industrial metals. As Zahra Ward-Murphy of ASR has consistently highlighted, the defining feature of the current environment is a growing mismatch between that demand and the physical systems needed to support it.

Industrial metals sit at the center of this rupture because they are foundational to nearly every strategic priority governments now care about: power generation, grid stability, defense readiness, and domestic manufacturing capacity.

Supply Is the Constraint

Most global markets often self-correct through the natural course of supply and demand. In the case of industrial metals, however, that mechanism is proving slow and unreliable. Mining projects typically take a decade or more to move from discovery to production. Ore grades are declining, capital costs are rising, and permitting hurdles are increasing. Even when capital is available, timelines remain extensive.

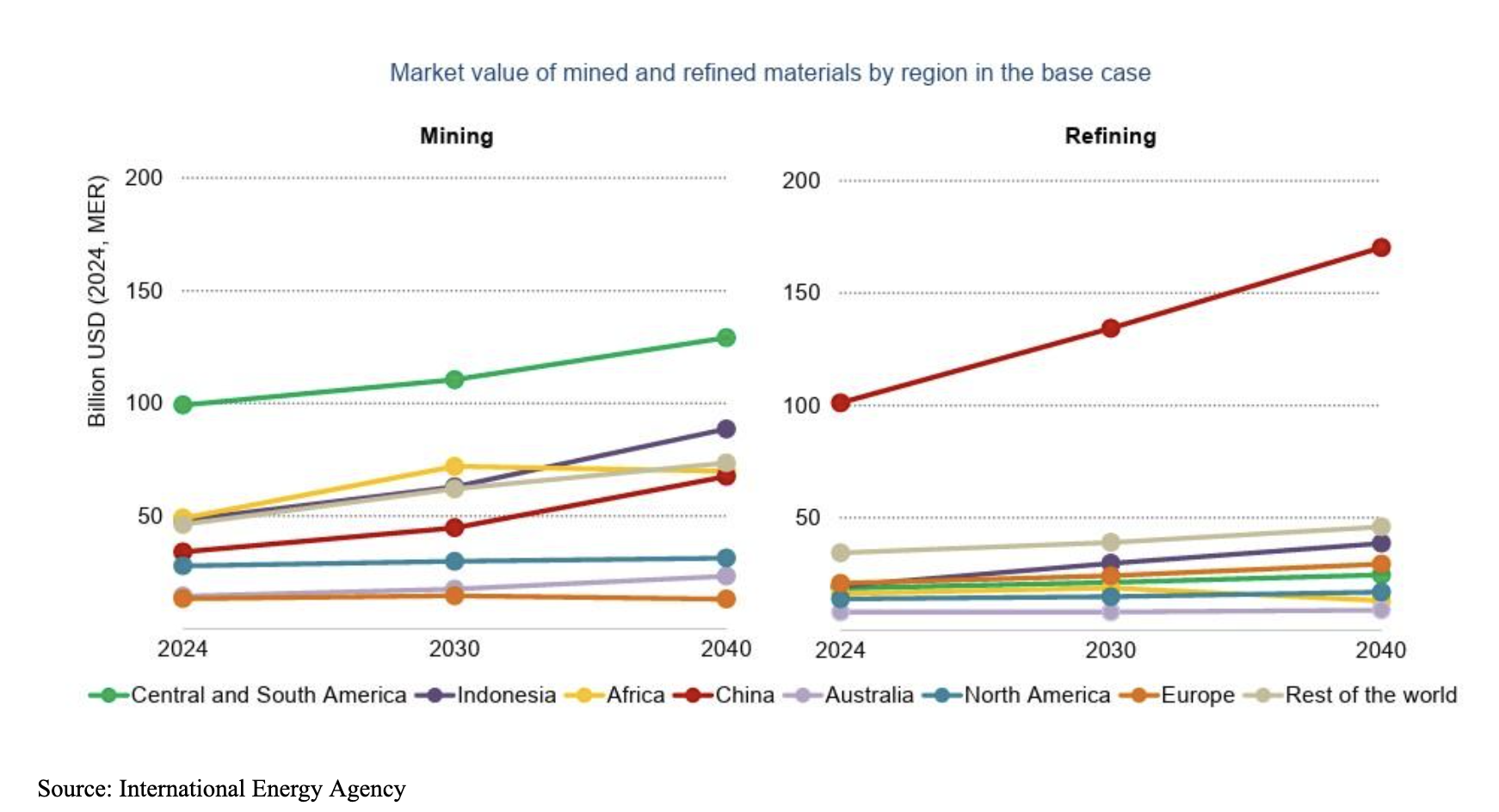

More important still is refining and processing capacity. While mining is geographically dispersed, refining is highly concentrated. China dominates the processing of many critical metals, including copper, aluminum, rare earths, and battery materials. This dominance reflects decades of investment, infrastructure build-out, and regulatory alignment.

Building refining capacity elsewhere is not simply a matter of price incentives. Refineries require environmental approvals, skilled labor, reliable energy inputs, and political support. Even with subsidies, for a variety of reasons, these facilities take years to come online.

Supply responses in mining and refining lag price signals by many years, as projects require sustained periods of higher prices before investment translates into production. Even then, execution risk remains significant. At the same time, capital discipline constrains expansion: after past boom-and-bust cycles, companies prioritize balance-sheet strength and shareholder returns over aggressive greenfield growth.

Environmental, social, and permitting hurdles have become structural features of the development process, further slowing new supply. Refining capacity is even less responsive to price, given its capital intensity, political sensitivity, and reliance on policy support rather than pure market incentives.

AI is Not the Only Driver

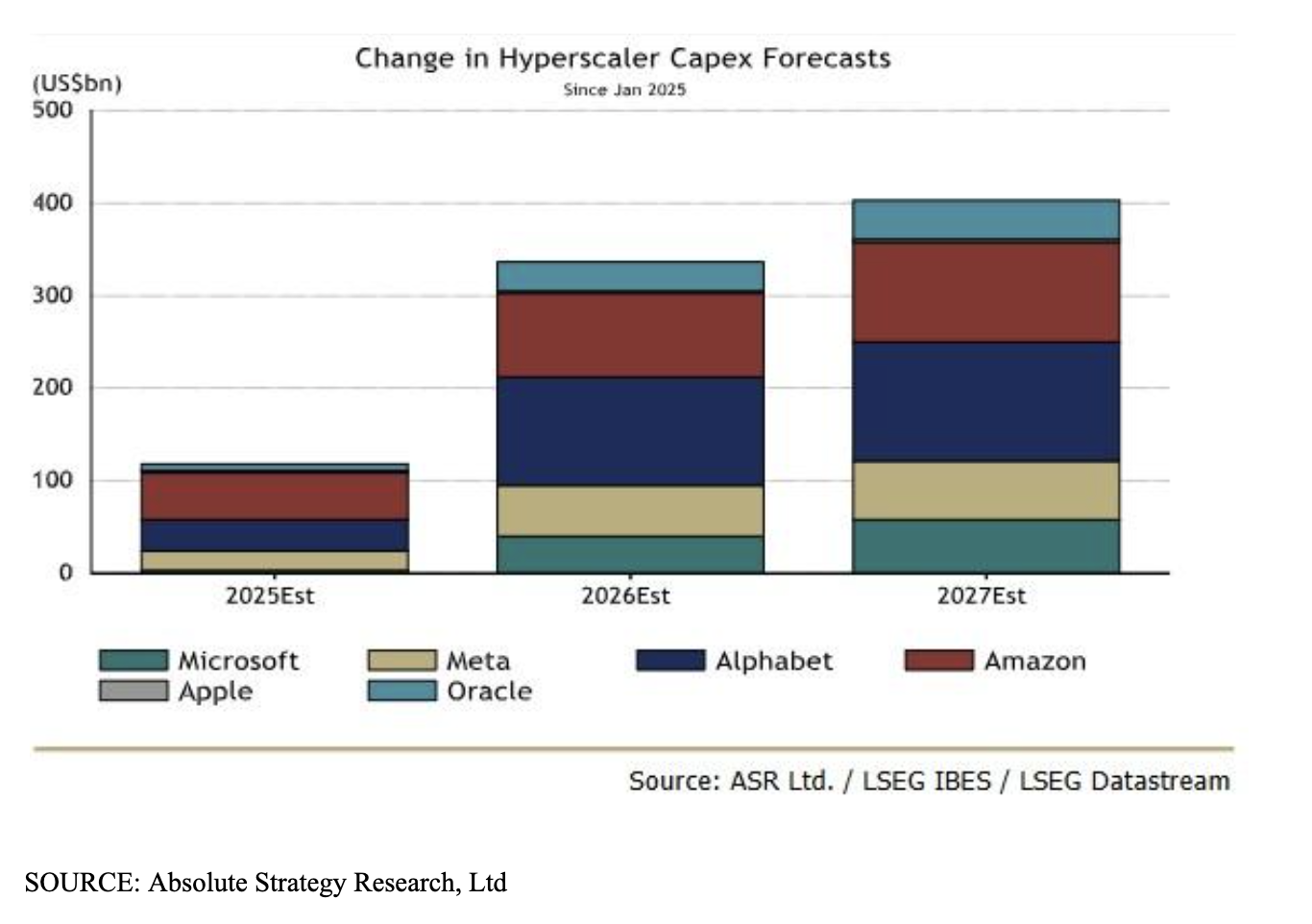

One of the most common questions surrounding industrial metals today is how much demand is tied to artificial intelligence and data center construction. AI has become the dominant narrative in markets, and the build-out of data centers is undeniably metal-intensive.

AI-related infrastructure has been contributing incremental demand for copper, aluminum, and certain specialty metals. However, when viewed in context, AI represents only a modest share of total demand for most core industrial metals.

Copper demand, for example, is dominated by electricity grids, electrification of transport, construction, and industrial applications. Even under aggressive assumptions, data centers account for only a low-single-digit percentage of global copper demand. Aluminum demand is similarly driven by power infrastructure, transport, and industrial use. Silver demand is overwhelmingly tied to solar photovoltaics and electronics, with AI playing a negligible direct role.

Even in a scenario where AI investment slows meaningfully, whether due to overcapacity, capital discipline, or weaker returns, the impact on industrial metals demand would likely be incremental rather than structural.

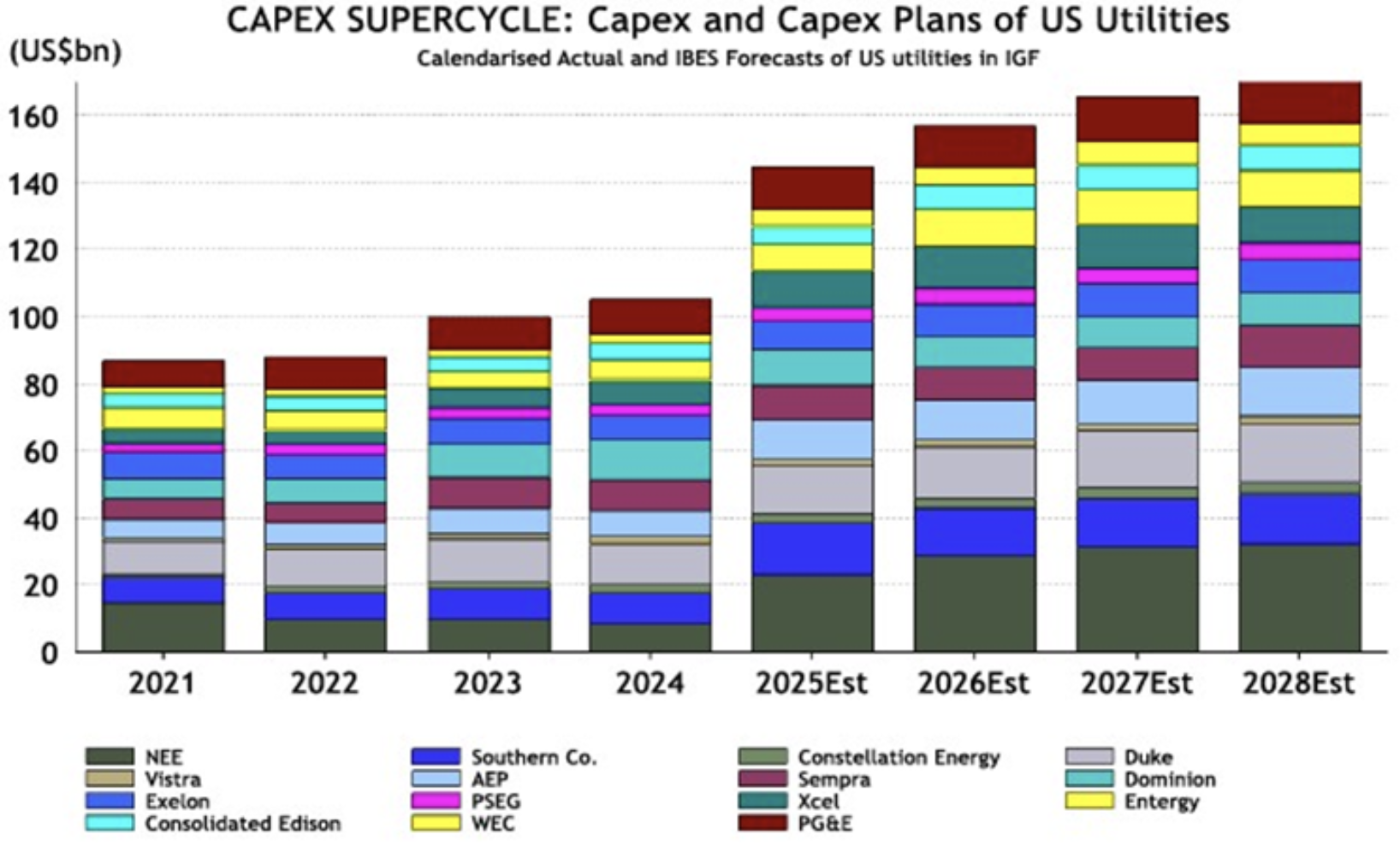

If AI has taught markets anything, it is that digital growth is constrained by physical reality. Data centers consume massive amounts of electricity from generation, transmission, and distribution systems that were built for a different era.

Further, global electricity demand is rising faster than grid infrastructure can adapt. Transmission bottlenecks, transformer shortages, and permitting delays are already creating friction across advanced economies. These issues are not theoretical; they are showing up in project delays and cost overruns.

SOURCE: Absolute Strategy Research, Ltd

SOURCE: Absolute Strategy Research, Ltd

Copper and aluminum are central to this challenge. Copper is essential for wiring, transformers, and transmission lines. Aluminum plays a critical role in overhead lines, substations, and structural components. These metals are difficult to substitute at scale, and their production cannot be ramped up quickly.

Crucially, AI, electrification, renewable integration, and industrial reshoring are all drawing on the same physical systems. Multiple demand streams are converging on infrastructure that was never designed for this level of load.

Why Substitution and Recycling Are Not Near-Term Solutions

Often, at times of peak demand, recycling and/or metal substitutes help to alleviate the supply bottleneck. While both help at the margin, neither provides an ample near-term solution.

Substitution has already occurred where economically and technically feasible. Silver use in solar panels has been reduced dramatically over the past two decades. Battery chemistries have evolved to reduce reliance on certain metals. These changes improve efficiency but do not eliminate overall demand growth.

Recycling faces its own constraints. Scrap availability is limited and increasingly regulated. Several governments have restricted scrap exports to retain domestic supply, reducing global flexibility. Recycling is also energy-intensive and depends on the same infrastructure constraints affecting primary production.

Technological innovation tends to shift bottlenecks rather than remove them. New systems still require physical inputs — often in different combinations.

Strategic Behavior: Hoarding, Stockpiling, and Policy Intervention

Strategic stockpiling, once associated primarily with oil, is expanding to include a wide range of metals. Export controls are proliferating. Subsidies and financing programs are being deployed to encourage domestic mining and refining, even if it costs more than importing the metals.

This behavior reflects a simple reality: When supply is tight, availability matters more than price. Governments are willing to accept higher costs in exchange for security.

Ward-Murphy has emphasized that this policy-driven demand is inherently price-insensitive. Once a metal is deemed critical, procurement decisions are driven by reliability, not short-term market conditions.

In recent news, the U.S. plans to launch a $12 billion public-private critical-minerals stockpile (“Project Vault”) to reduce reliance on China, stabilize input costs for manufacturers, and protect supply chains for sectors like autos, semiconductors, and aerospace. The structure combines $1.67 billion in private capital with a $10 billion EXIM loan, with companies committing to buy and later repurchase stored materials at preset prices, effectively creating a buffer against price spikes and disruptions. The initiative reflects rising geopolitical urgency after export controls and recent commodity shocks, while also signaling deeper government involvement in domestic production and allied supply partnerships.

Risks and What Could Go Wrong

Any number of events may directly and adversely impact the industrial metals market. A sharp global recession would likely soften demand. China’s growth trajectory remains uncertain. Political missteps could distort markets. And institutional and consumer investment manipulation can generate potential price instability.

However, in our opinion, these risks tend to affect timing and volatility rather than direction. The underlying physical constraints remain. Even a meaningful slowdown in AI investment would not reverse the broader demand drivers. Power grids still need upgrading. Defense systems still require materials. Electrification goals remain policy-anchored.

Investment Horizon

This is a theme with a two-to-four-year horizon, perhaps even longer. Unless credible substitutes emerge at scale, a development that appears unlikely in the near term, industrial metals will be required in increasing quantities. That reality will likely continue to compel nations to secure supply, hoard strategic materials, and accelerate domestic mining and refining, even at higher cost.

For investors, this requires a complete reconsideration of their investment allocation. “Rising debt burdens, persistent inflation, and growing resource scarcity challenge the assumptions underpinning the 60/40 portfolio,” says Ward-Murphy. “This strengthens the case for real assets to play a greater role in portfolio construction, both for inflation protection and as a source of diversification.”

As the world confronts energy security, geopolitical fragmentation, and infrastructure strain, we are reminded that materials are critical economic inputs. The rupture described by Harnett and Bowers is no longer theoretical. It is visible in supply chains, policy decisions, and investment priorities. Zahra Ward-Murphy’s work makes clear that this shift is not fleeting. Particularly in a world of rapidly fluctuating equity values and interest rate curves, investors would be prudent to consistently evaluate their portfolios and consider adding suitable exposure to the metals markets.

David Tepp is the founder and chief wealth strategist of Tepp Wealth Management, an SEC-registered investment advisor based in Westfield, New Jersey. With over 20 years of experience in wealth management, David provides strategic financial planning and investment advisory services to high-net-worth individuals and families. He frequently writes on macroeconomic policy, fiscal risk, and market strategy to help investors navigate an increasingly complex global economy.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All