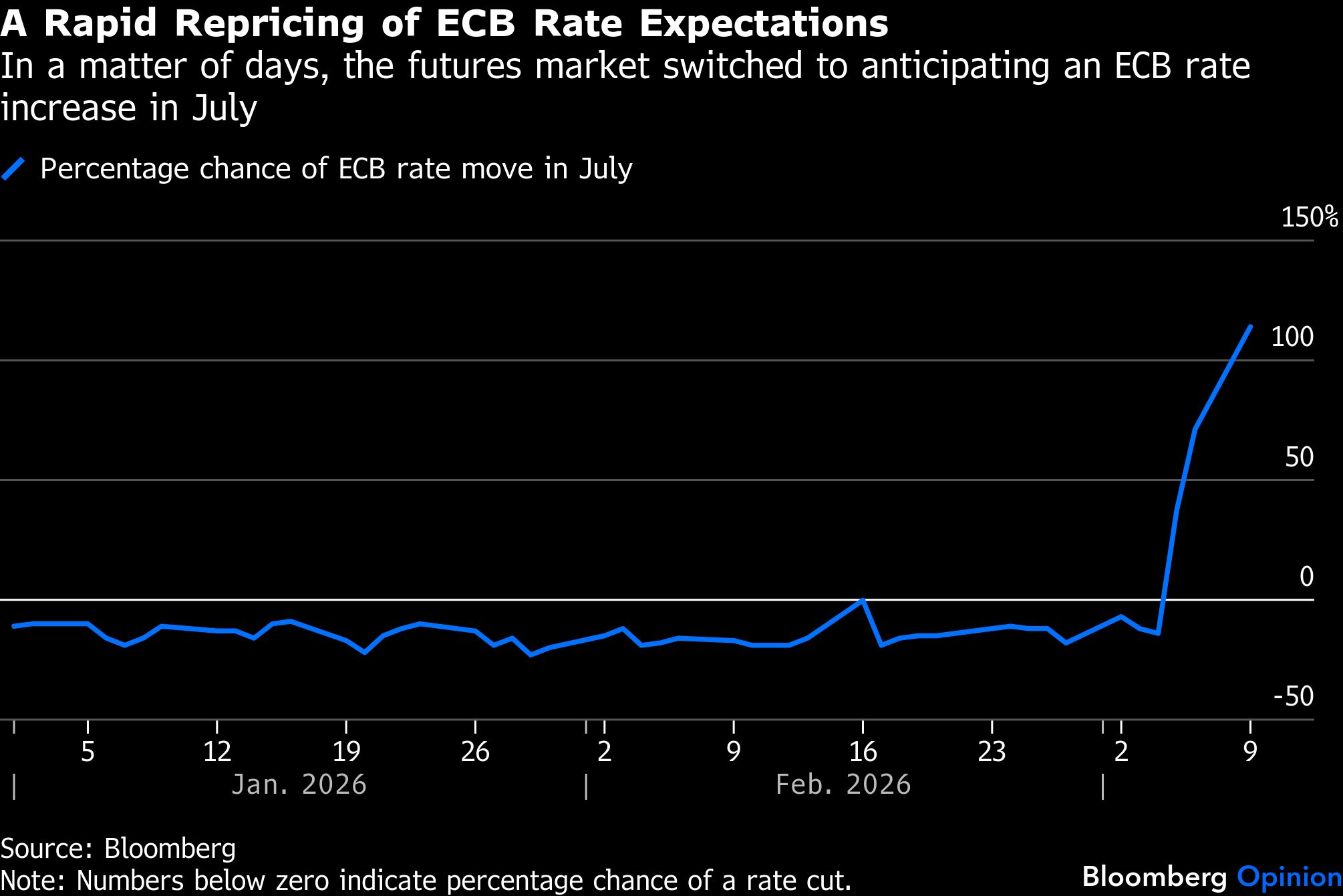

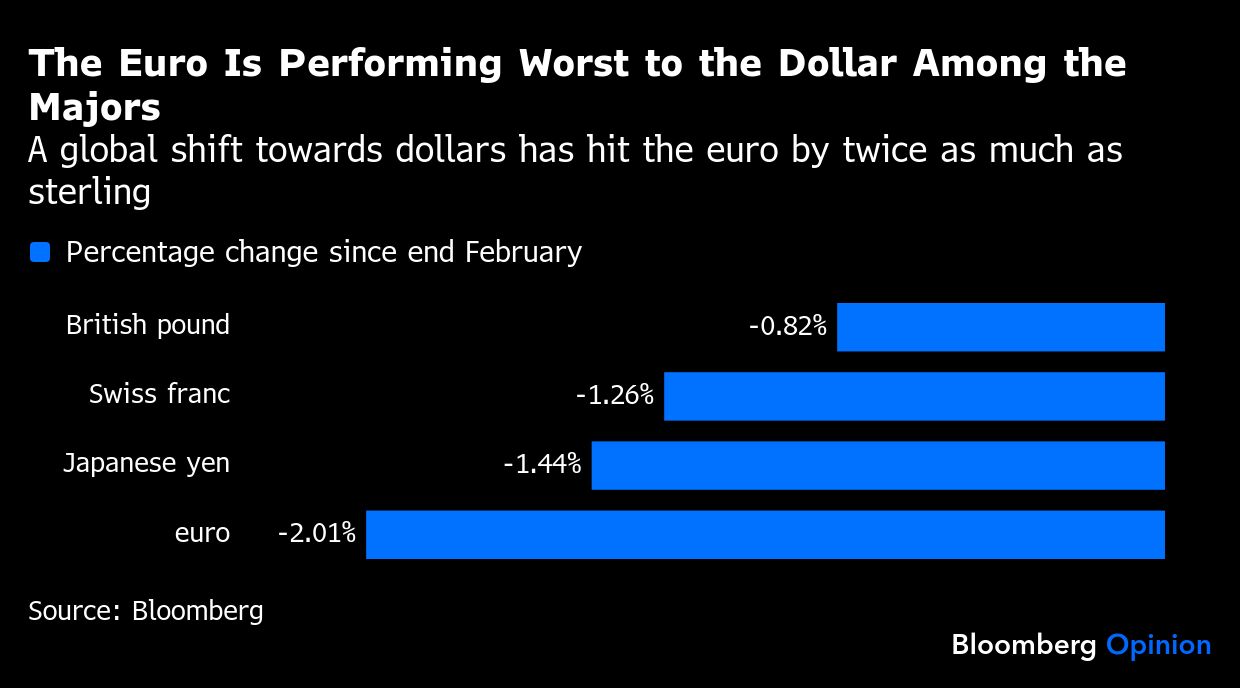

The European Central Bank can be forgiven for feeling nauseous as a massive global deleveraging of risk since the Iran war started has hit the euro area’s currency and interest-rate markets particularly hard. While haven flows into the dollar have boosted the greenback across the board, the euro has weakened by more than any other major currency, and by twice as much as sterling. The futures market has shifted from seeing no monetary policy actions this year to anticipating a tightening as early as July. Policymakers will need to tread particularly carefully.

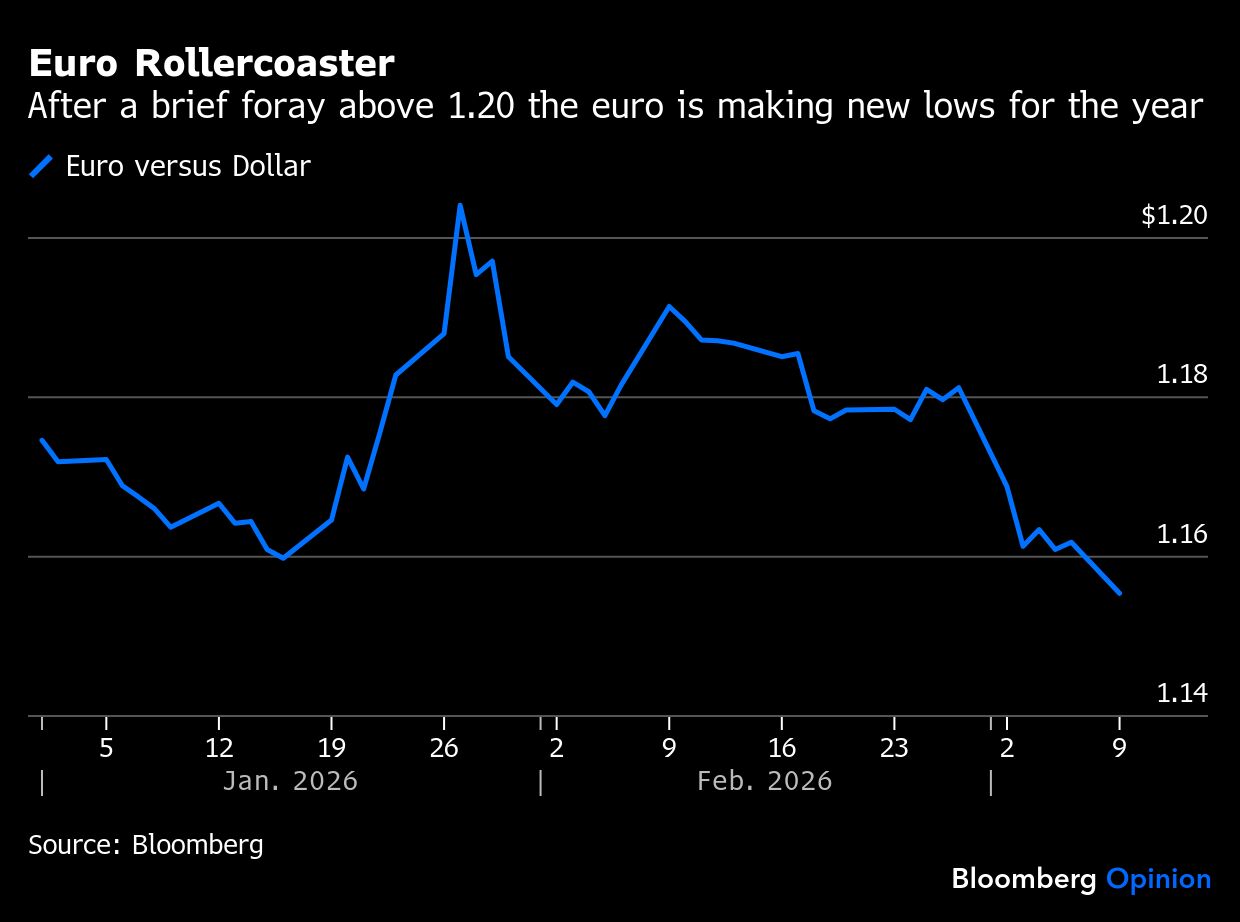

Just a few short weeks ago, the common currency breached the $1.20 level that sets alarm bells ringing in Frankfurt; this week, it’s fallen precipitously toward $1.15 in the kind of sudden lurch that makes central bankers nervous. Europe is dangerously exposed to rising energy prices as oil hovers around $100 a barrel; memories of soaring costs that propelled consumer prices upwards in 2022 after Russia’s invasion of Ukraine are still fresh enough to sting.

ECB policymakers need to balance their desire to control inflation expectations with the need to minister to an economy that remains lackluster at best. Allowing expectations to build that it will respond by hiking interest rates — the futures market has swung to currently anticipating tighter policy by mid-year from mildly betting on rate cuts just a few days ago — risks losing the plot. The ECB remains “very vigilant” on inflation risks, according to German central bank head Joachim Nagel; he emphasized that at the March 19 governing council meeting “we will then decide whether action needs to be taken.” That’s not helpful. ECB President Christine Lagarde ought to be calming the skittish market horses.

I’m highly skeptical that the euro economy could weather a rate increase, let alone a series of them, so tighter policy would probably end up hurting the common currency. The ECB expects growth of 1.2% this year — but this is contingent on improved domestic consumption, rising household incomes and improved financing conditions. I’m not quite sure an oil-price shock is compatible with that outlook. The inflation picture is somewhat mixed; February’s 1% increase in consumer prices put the measure at half the ECB’s target, but core inflation jumped more than expected to 2.4% from 2.2%, underlining the bloc’s sensitivity towards external price pressures.

Without this seismic repricing of interest-rate expectations, the euro would probably be even weaker. But there's a wider issue at play here — the euro is not yet the investment haven its policymakers would dearly love it to be. Societe Generale SA analysts reckon that "although Treasuries and equities are falling, investors seem comfortable holding dollars in this environment, especially relative to the euro.”

Rising commodity prices, which are typically denominated in dollars, are exacerbating demand for greenbacks. George Saravelos, global head of FX research at Deutsche Bank AG, said in a note on Tuesday that "there is a negative supply shock under way which represents a direct tax on Europeans that has to be paid to foreign producers in dollars." He estimates that for a 10% rise in Brent crude, the euro to dollar rate is currently weakening by about 0.8%.

Demand for dollars in the cross-currency swaps market has surged relative to its global peers, reflecting increased requirements to fund liquidity in greenbacks outside of the US. The euro basis-swap spread to dollars is the widest since the April 2 “Liberation Day” tariffs hit; sterling and Swiss franc cross basis differentials show a similar picture. There is very little dollar funding stress, but there are vibes of the 1970's energy crisis as bond yields are rising reflecting a lack of demand for duration risk. So while there’s no panic, risk premiums are rising.

As Europe is much closer to the conflict, it’s logical that investors there will be more sensitive to de-risking. The subsequent inflationary, and negative growth, implications if the conflict extends are greater. The opposite is largely the case for US investments, which also stand to gain more on a swift resolution. It’s notable that intraday recoveries this month have been stronger in US market opening hours.

Central banks can handle steady currency fluctuations, but sharp adjustments push them out of their comfort zones. Actual intervention is fraught with unintended consequences, while threatening rhetoric about potential action is usually meaningless — something the Swiss National Bank has likely discovered amid speculation it’s been intervening to cap the franc’s strongest level to the euro since 2015 after attempts last week to talk its currency lower failed.

The lack of a domestically-generated energy base is a constant thorn in Europe’s side — it’s hamstrung by being a price-taker. This puts its manufacturing industries in a even tighter bind as they struggle with stringent net-zero requirements. Increased currency volatility doesn’t make corporate planning any easier but higher interest-rate expectations are far more corrosive. Europe desperately needs a swift end to this Iran conflict, knowing that the Ukraine war shows no sign of resolution. Euro weakness maybe the most visible sign of stress, but it’s also a sign of longer-term structural issues. Letting rate-hike pressures build won’t solve anything.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Marcus Ashworth