How to Talk to Clients About Prediction Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

This article was written with the assistance of artificial intelligence. The underlying data, financial arguments, and strategic insights were authenticated by the author, who retains full accountability for the accuracy of the content.

Your client sends you a text: "Just made $2,000 on Polymarket betting Trump would win. Should I put more in for the Fed decision next week?"

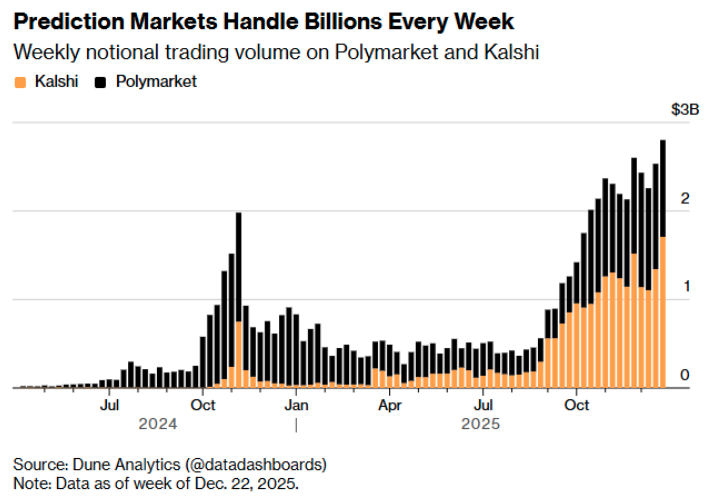

Welcome to 2026, where prediction markets have escaped the confines of academic economics papers and crypto-Twitter feeds to become dinner-table conversation.

Platforms like Polymarket and Kalshi have made it remarkably easy for anyone to wager on everything from election outcomes to Federal Reserve decisions to whether Taylor Swift will announce a new album by the end of the year.

For financial advisors, this creates an awkward conversation. Clients aren't asking whether prediction markets are interesting. They are asking whether they should participate, and with how much.

Investment vs. Speculation: Drawing the Line

The fundamental distinction advisors need to articulate is deceptively simple: investing funds in productive assets, while prediction market wagers stake money on short-term outcomes.

When you buy a share of stock, you are acquiring ownership in a business that employs people, produces goods or services, generates cash flows, and ideally creates value over time. When you buy a bond, you're lending capital that funds infrastructure, business expansion, or government operations. These are investments because capital flows into productive use. The investor should participate in that value creation through returns in their portfolio.

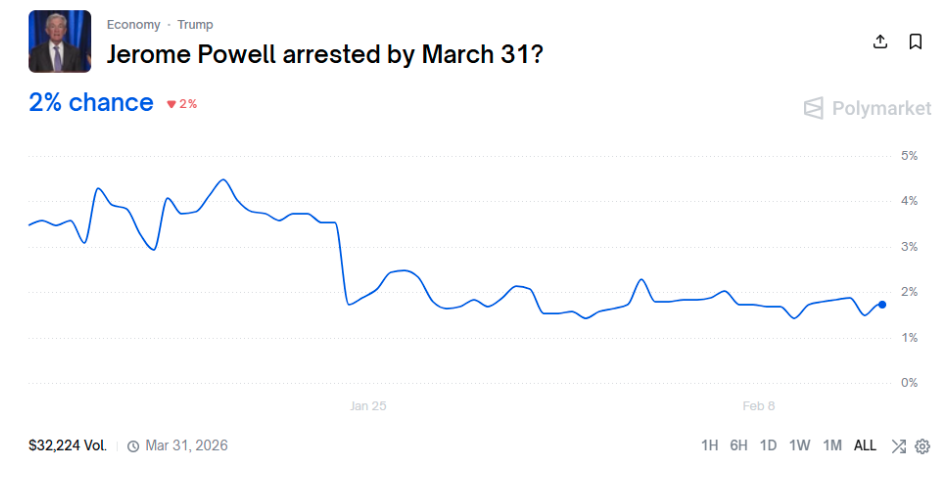

When you buy a contract on Polymarket asking if Jerome Powell will be arrested by March 31, no capital flows anywhere productive. You are simply taking the opposite side of someone else's bet. One of you will be right, one will be wrong, and money will change hands accordingly. The economy is not $1 richer for your participation. The value accrues to the platforms, data aggregators, and third-party users of that data, not to the participant, who therefore will have a negative overall return on average.

Prediction markets can be intellectually engaging, occasionally profitable, and even socially useful in aggregating information. But they aren't investments, will not accrue value to the participants long term and therefore, shouldn't be treated as such in a financial plan.

Why Clients Are Attracted

Understanding the appeal helps you address it productively rather than dismissively.

First, prediction markets offer immediate feedback and resolution. Unlike buying an index fund and waiting decades, you can bet on tomorrow's jobs report and know the outcome by 8:30 a.m. Friday. For clients exhausted by "stay the course" advice during volatile markets, this feels refreshingly actionable.

Second, these platforms are genuinely well-designed. The user experience is smooth, and the odds update in real-time. Seeing your position move as new information emerges creates a dopamine hit that periodically rebalancing a 60/40 portfolio simply cannot match.

Third, there's a seductive narrative of informational edge. Your client who works in pharmaceutical research might genuinely know more than the market about FDA approval timelines. The illusion of expertise makes prediction markets feel less like gambling and more like applied knowledge.

The Advisor's Framework

When a client raises prediction markets, resist the urge to lecture or dismiss. Instead, establish a framework.

Acknowledge Reality First

"Yes, some people make money on these platforms, just like some people make money playing poker. That doesn't make it investing." This validates their experience without endorsing the activity.

Quantify Acceptable Risk

If a client insists on participating, treat it like any other speculative activity. The traditional rule for speculation — whether day trading, crypto, or prediction markets — is that total speculative positions shouldn't exceed 5% of investable assets, and many advisors prefer 2% to 3%. Money allocated here should be genuinely expendable, not earmarked for retirement, education, or emergency reserves.

Tax Reality Check

Winnings on prediction markets are taxable income. Losses may or may not be deductible depending on whether the IRS treats the activity as gambling (where deductions are limited) or trading (where they're more flexible).

The regulatory landscape remains uncertain, and clients need to understand they may face tax bills without clear deduction offsets.

The Difficult Conversation

What if a client gets hooked? What if that $2,000 win becomes $10,000 in wagers on increasingly obscure outcomes?

This is where your relationship matters. You need to name the pattern you're observing without being judgmental: "I notice you've gone from one bet to five in the last month, and the amounts are increasing. That concerns me, not because I think you're doing anything wrong, but because this pattern often precedes problems."

Gambling addiction doesn't announce itself. It creeps in through a series of wins that feel like skill, followed by losses that feel like bad luck, followed by larger bets to recoup losses. If you see this progression, your job isn't to be a therapist; it is to acknowledge what you're seeing and suggest professional resources.

The Opportunity

Here's the counterintuitive part: client interest in prediction markets offers a teaching opportunity about actual investing.

When a client asks about betting on Fed decisions, you can ask: "What if instead of wagering on what the Fed will do, we positioned the portfolio to perform reasonably well regardless of what they do?" This reframes the conversation from prediction to resilience.

When they're excited about a political prediction market, you can discuss how diversified portfolios are designed to weather different political outcomes rather than requiring you to correctly forecast them.

Conclusion

Prediction markets aren't going away. They're designed to be fun and exciting for bettors, intellectually engaging, and culturally resonant. The question isn't whether your clients will participate, but whether you'll have a productive framework ready when they do.

That framework starts with clarity about what investing actually is and continues with reasonable guardrails for speculative activity. It ends with having the humility to recognize when a client's interest has crossed into something more concerning.

An advisor’s value isn't in predicting the future. It is building portfolios that don't require you to.

Joe Halpern is managing partner of Obsidian CIO. Request his new white paper, How to Scale Your RIA to $1 Billion and Beyond.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All