For months, Wall Street’s panoply of risk-hedging strategies did little but lose money. Now, as uncertainty sparked by the war with Iran hits the market’s most popular trades, investors that loaded up on portfolio protection are being rewarded.

The spiraling conflict in the Middle East has wiped out some $6 trillion in global equity-market value over the past week while catapulting oil above $100 per barrel for the first time since 2022. Prices for 10-year Treasuries fell for five-straight sessions last week and volatility has surged across asset classes, reversing months of calm in a matter of days.

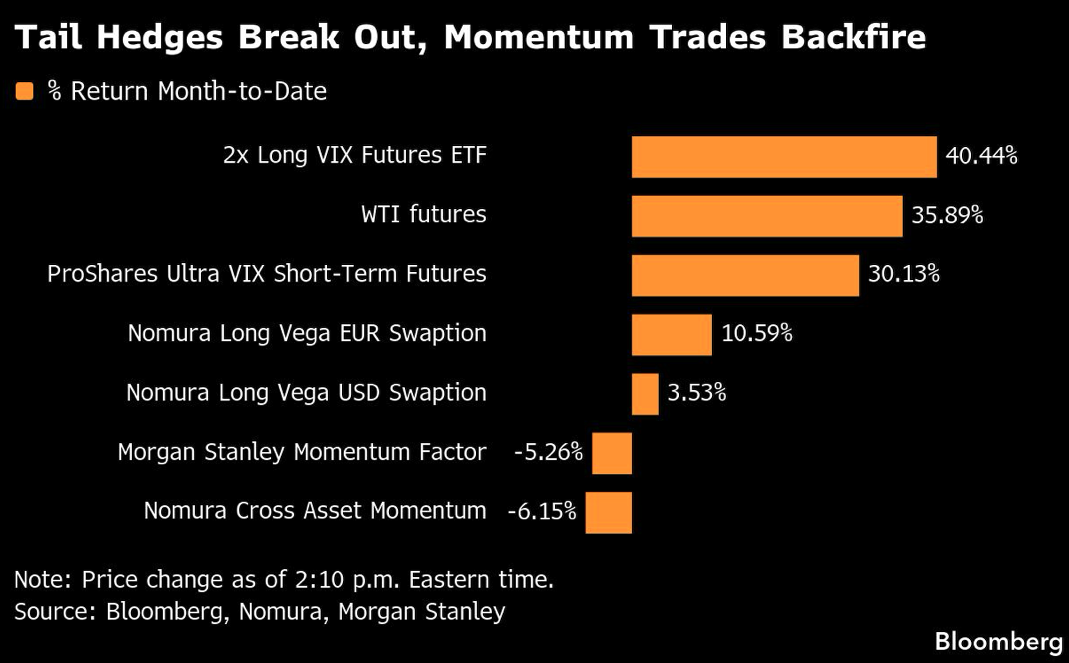

Strategies that benefit from market turbulence are surging as a result. Among them are leveraged funds tied to the Cboe Volatility Index, or VIX, which are up as much as 34% this month. A long-volatility strategy focused on European rate swaptions has risen more than 10%, and another tied to US interest rates is sporting a nearly 4% gain, according to indexes kept by Nomura International Plc.

“Tail risk hedging strategies have overall seen gains over the past week, in particular long volatility strategies across asset classes,” said Steven Loeys, head of macro quantitative investment strategies at Nomura. The strategies “are designed to perform in periods of increased risk.”

Tail-risk strategies are built to pay off in moments like this — but the cost of carrying them through calm markets has long divided portfolio strategists. The products lose money slowly and steadily when volatility is low, and the stretches of underperformance can last long enough to exhaust even committed holders, raising persistent questions about whether the occasional windfall justifies years of drag.

With the S&P 500 Index off more than 2% since the war kicked off and many individual stocks notching far greater losses, leveraged ETPs tied to the VIX have been among the top performers. The 2x Long VIX Futures ETF (UVIX), which looks to double the performance of a long-VIX index, has soared more than 30% so far in March. The ProShares Ultra VIX Short-Term Futures ETF (UVXY), designed to deliver 1.5 times the performance of a gauge linked to the VIX index, is up more than 20% this month.

The turnaround has been especially dramatic for strategies tied to long-expiry interest rate swaption straddles — derivatives that allow investors to enter interest rate swaps. They’re a protective tool against rate swings that also gauge expected volatility. Banks had spent years building and selling the products, only to watch the carry advantage that made them tolerable erode alongside the hedging value.

Meanwhile, the pain has been widespread on the other side of the ledger, as an unwind in popular momentum strategies across equities, credit, currencies and rates collides with an oil shock and a jobs report that wrong-footed consensus.

A cross-asset momentum index has fallen more than 6% last week while emerging-market currency momentum is down about 4%, according to Nomura. A long-short Morgan Stanley basket tracking momentum stocks has slid more than 6% so far this month.

To Amy Wu Silverman, head of derivatives strategy at RBC Capital Markets, the recent outbreak of volatility is exactly the kind of multi-front stress that many hedges were built for.

Though the S&P 500 is down only marginally year-to-date, “the volatility under the surface has been staggering,” she said. “I think true concerns on growth and inflation still have to make their way through the system.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.