His time horizon is infinite. His capital is permanent. And the rewards, he argues, should be enormous.

That’s the pitch Bill Ackman is making as he moves to take Pershing Square public alongside a new closed-end fund in a deal that could raise as much as $10 billion and bring millions of everyday investors further into his orbit.

For Ackman, it’s a comeback from a prior, aborted attempt to list a blockbuster closed-end fund in the US. But it’s also something bigger: a milestone in his years-long project to turn Pershing Square into a modern-day version of Warren Buffett’s Berkshire Hathaway Inc.

On offer are shares of Pershing Square USA Ltd., the closed-end fund. But for every 100 shares of PSUS they buy, investors will automatically receive 20 shares in the management company Pershing Square Inc. The structure means the closed-end fund will have a more permanent base of capital, which Ackman says will let him pick winners and allow them to bloom without worrying about investors yanking their money.

“Our long-term goal for Pershing Square Inc. is to build one of the most valuable companies in the world by generating one of the best long-term performance records of any investor ever,” Ackman, who has a net worth of more than $8 billion, wrote in a letter to investors this week.

The pitch is a timely one. The private-markets boom has given rise to a bevy of products that promise occasional liquidity while owning hard-to-sell assets like private loans and real estate. But now a wave of investor redemptions is forcing titans like Blackstone Inc. and BlackRock Inc. to balance those withdrawal requests with a need to keep the underlying portfolios healthy.

That’s precisely the kind of crunch Ackman says his business model avoids. Pershing investors would get liquidity by selling their shares, not by asking the manager for their money back.

“We think of our business model as akin to owning a royalty on the compounding of assets invested in high-return investment strategies,” said Ackman, who rose to prominence as an activist investor atop a traditional hedge fund. “If you understand the long-term math of compounding, you can appreciate the extraordinary potential of PSI’s business model.”

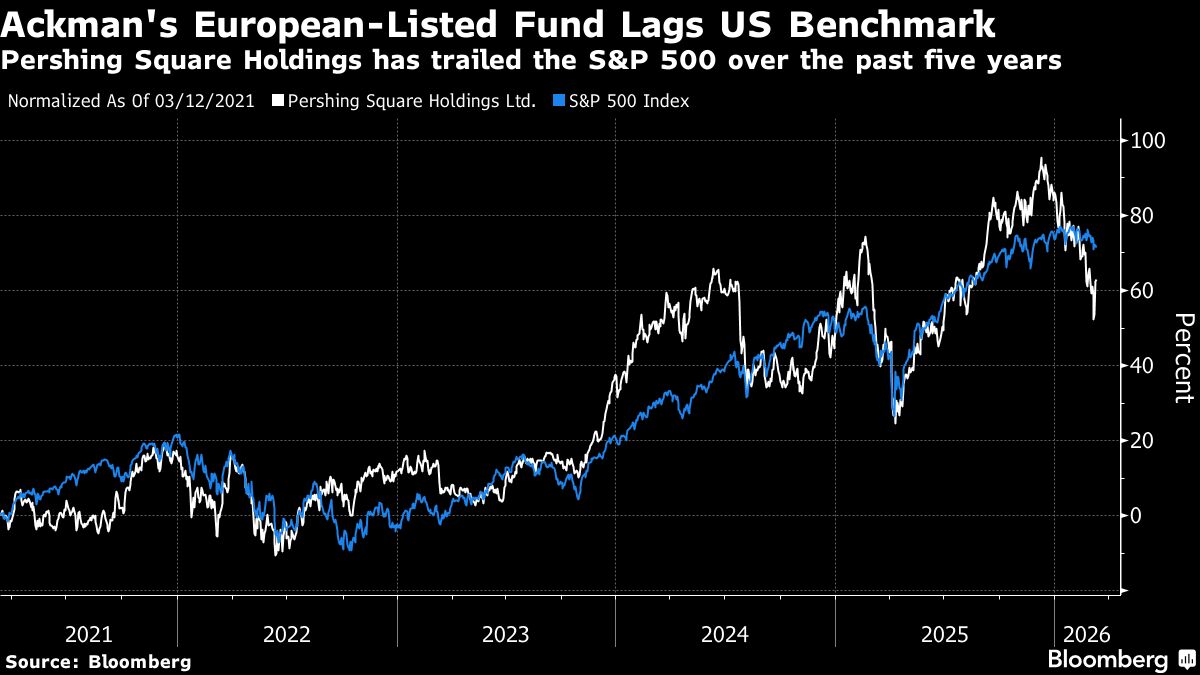

A wrinkle for Ackman is the reality that closed-end funds have fallen out of favor in recent years and most trade at a discount to the value of their underlying holdings. Pershing Square Holdings Ltd., the firm’s more-than $17 billion London-listed closed-end fund, trades roughly one-quarter below its net asset value, data compiled by Bloomberg show.

While investors will debate whether the newest closed-end fund trades below the $50 price for IPO buyers, its European counterpart hasn’t inspired enthusiasm when compared to the US bull market. Pershing Square Holdings has lagged the S&P 500 Index over both five-year and one-year time horizons, according to data compiled by Bloomberg.

Part of the funds from the IPO of the closed-end fund will be raised from a private placement, with $2.8 billion from investors including family offices, pension funds and insurances companies, according to regulatory filings. They include the Teacher Retirement System of Texas, Arch Capital Group Ltd., BTG Pactual and Marlton LLC, according to people familiar with the matter.

The asset manager won’t receive any proceeds from the IPO. Pershing Square expects the two companies to trade independently once the IPO is priced.

Representatives for all four firms as well as a spokesperson for Pershing Square declined to comment.

Ackman Comeback

The IPO would represent a major coup for Ackman. A plan two years ago for a New York Stock Exchange-listed vehicle was cut from $25 billion to $4 billion, then $2 billion, before being entirely scrapped.

The ordeal left many on Wall Street scratching their heads, and was a major stumble for an investor who has had his fair share of devastating losses. Soured bets on both Herbalife Ltd. and Valeant Pharmaceuticals cost the fund billions of dollars from 2015 to 2017 — a period so tumultuous for Pershing that it is called out in IPO filings.

Pershing has since entered what it calls its “permanent capital era,” focusing on growing its asset base and reorganizing its business. A key part of the transition came in May, when Pershing and its funds struck a deal to boost its stake in property company Howard Hughes Holdings Inc. to 47%.

The maneuver fits into a broader plan to fashion Howard Hughes into a conglomerate with controlling stakes in myriad businesses, including an insurer that could provide Pershing with even more capital. Ackman likened the model to Berkshire, the $1 trillion behemoth that Buffett spent decades building. Ackman and Pershing Square Chief Investment Officer Ryan Israel have even floated the idea of an in-person annual meeting that would have shades of Berkshire’s yearly confab in Nebraska.

He’s done little to discourage those comparisons with this week’s IPO filings. While not mentioned by name, the documents are replete with value-investing vocabulary from the school of Buffett and Berkshire. There’s talk of moats, an emphasis on cash flow and a preference for simple, predictable businesses.

But investing styles and corporate structures aren’t the entirety of what made Buffett into the Oracle of Omaha. He earned the long-term trust of investors and possesses a singular mix of candor, loyalty and patience, beyond just permanent capital, said Lawrence Cunningham, professor emeritus of law at George Washington University.

Cunningham hosted a symposium on Buffett’s shareholder letters in 1996 where Ackman, then a young striver, met Buffett. He recalled a turnout of a couple hundred guests for the event — modest compared to what such a gathering might command today.

“He needs them to be patient and willing to commit,” Cunningham said of Ackman‘s pitch to investors. “That’s not easy to do. There’s enormous short-term pressure.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Hema Parmar, Annie Massa, Bailey Lipschultz