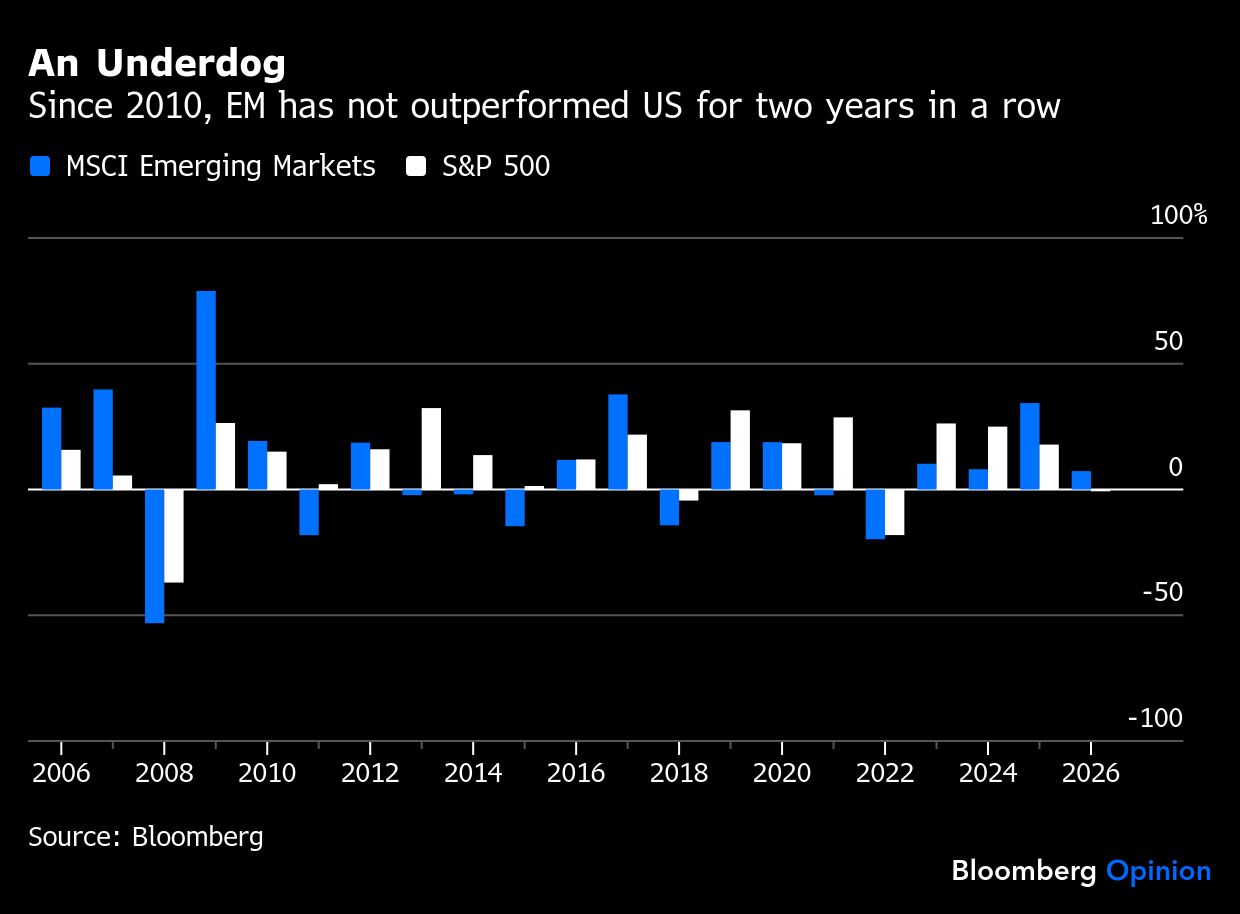

For more than a decade, emerging markets have been a heartbreak for those who place their faith in developing countries. Since 2010, the benchmark MSCI Emerging Markets Index has not outperformed its US counterpart for two consecutive years.

Coming into 2026, global investors were getting their hopes up. The mechanisms that underpinned last year’s outsized returns, such as a weak dollar, benign global economic growth, and investors’ desire to diversify internationally, continued to be present.

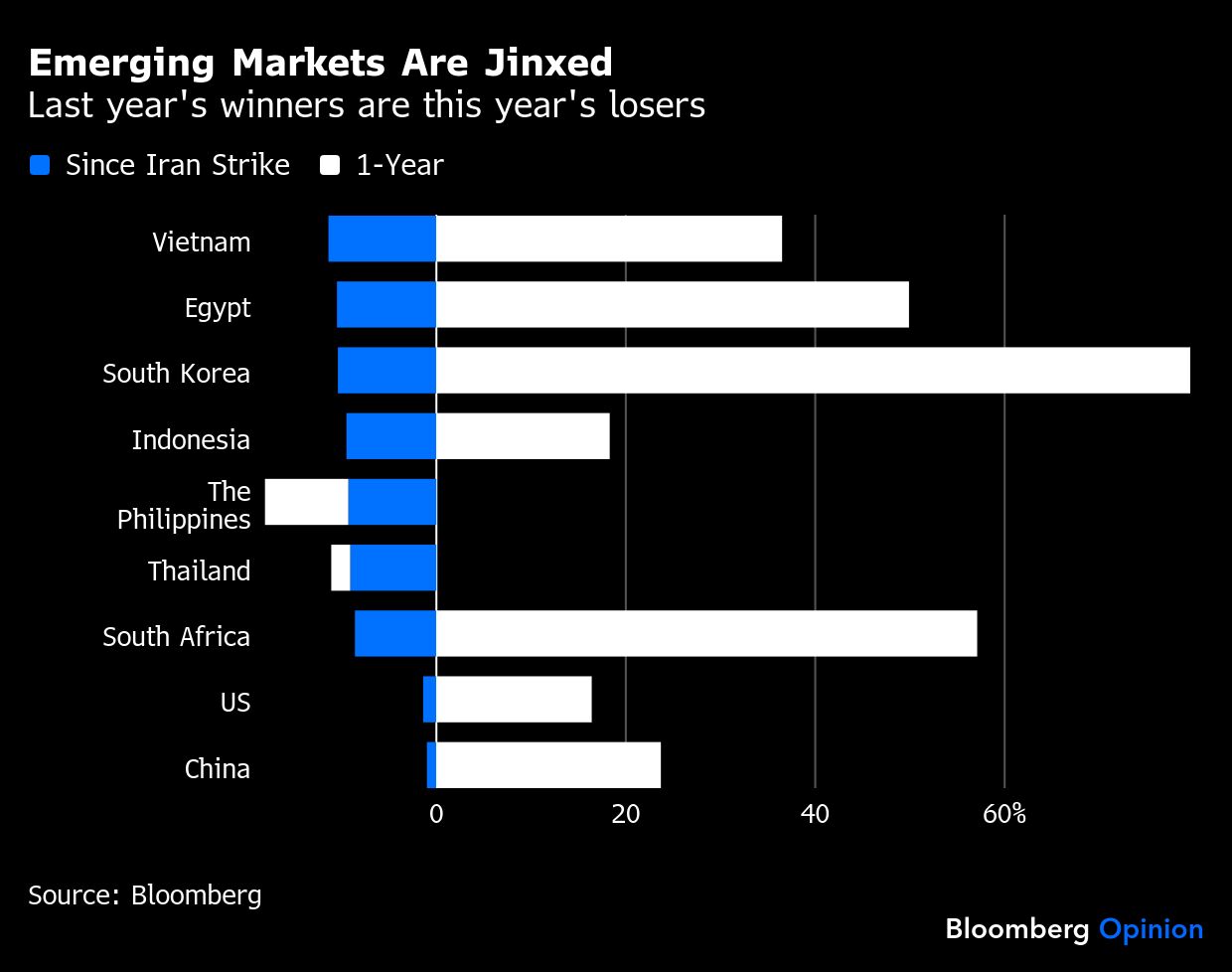

The Iran war has broken that optimism. Since the US and Israeli strikes began on Feb. 28, emerging-markets equities have fallen by as much as 10%, while the S&P 500 has held firm.

De-grossing, where investors clear their positions to reduce leverage and overall exposure to markets, was at work. Last year’s frothy bourses, from South Korea to Egypt to Vietnam, have been sold off the most. As long as volatility remains — oil markets have been on a wild ride in recent days — emerging markets will likely be collateral damage.

South Africa, for instance, had a fantastic run last year as its economy picked up pace and its debt ratio stabilized. The rand gained 14% against the dollar, government bond yields fell to a decade-low, and the stock market rallied in part due to heavy exposure to gold miners.

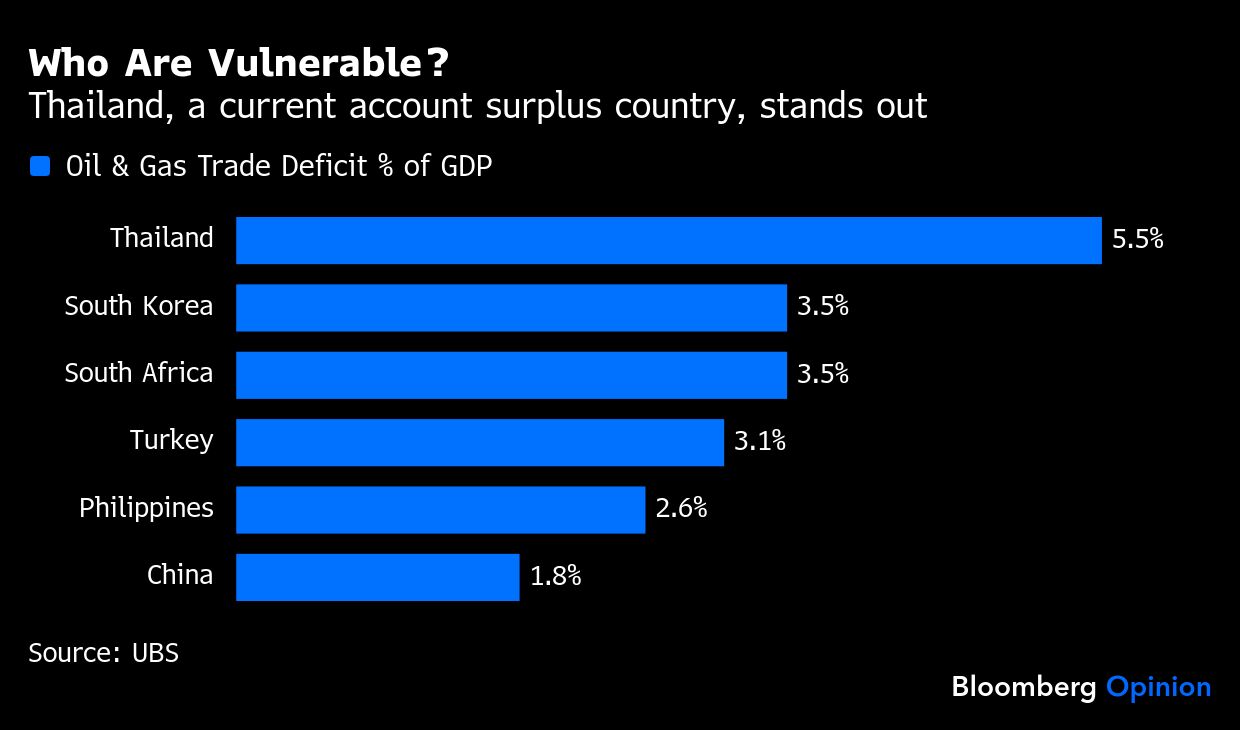

That’s being reversed. Now that portfolio managers have switched to their risk-averse lens, they are once again examining emerging markets’ fragile side. An importer when it comes to fuel, South Africa’s oil and gas trade deficit still accounts for 3.5% of its gross domestic product even though cheap solar from China is transforming the economy and reducing power cuts.

Other energy customers are suffering, too. Stock markets in Thailand and the Philippines have tumbled, despite the fact that they underperformed last year. Thailand’s current account is a particular worry, because unlike South Korea and Taiwan, it can’t rely on booming AI-related semiconductor exports to offset ballooning energy imports. A sustained rise in the oil price can flip Thailand into a deficit nation.

And what’s the lure of emerging markets if there’s no growth? More than inflation, investors are worried that conflict in the Middle East will set back an AI-fueled global economic expansion. In Taiwan and South Korea, where the likes of Taiwan Semiconductor Manufacturing Co., Samsung Electronics Co. and SK Hynix Inc. make chips for Nvidia Corp., about 60% of energy consumption comes from oil and gas, according to UBS Group AG. A prolonged oil shock could raise input costs for global tech companies and slow down their capital spending. This, in turn, hurts domestic growth in developing countries.

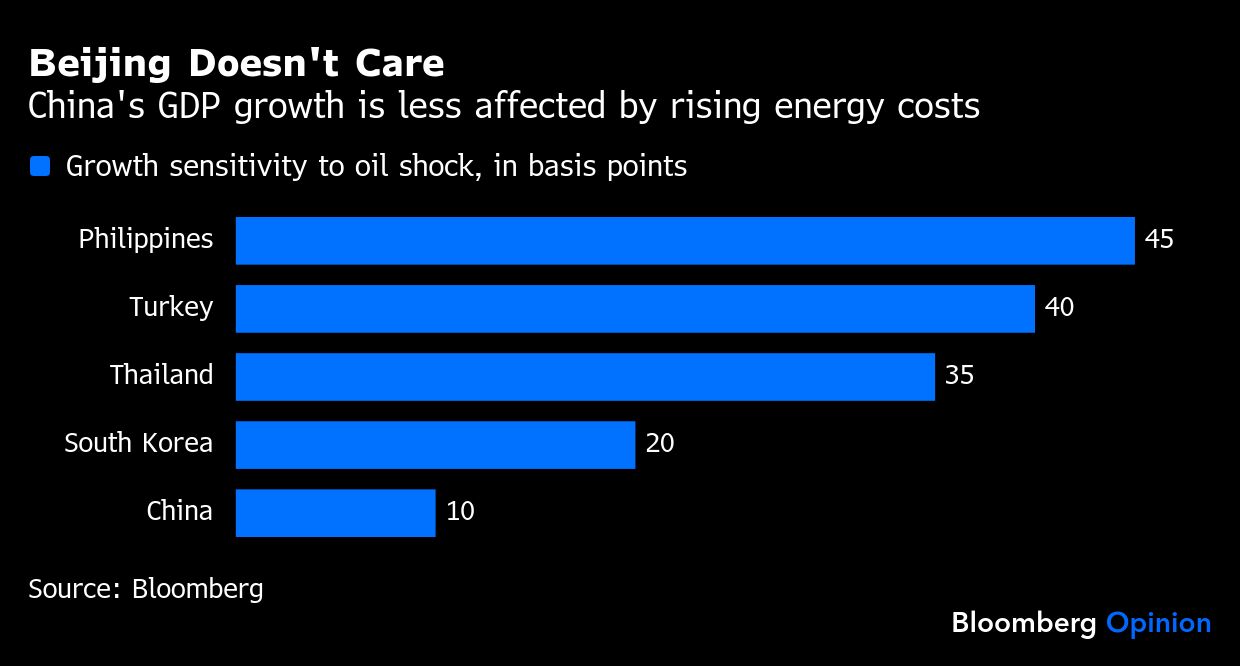

But more importantly, let’s not forget the elephant in the room — China. Last week, as the Iran conflict escalated, policymakers led by President Xi Jinping congregated in Beijing to discuss and set long-term economic goals. They certainly didn’t pencil the war in, dialing down fiscal support from last year. The reflation trade did not pan out.

And why should China come to the world’s rescue? As far as Beijng is concerned, its economy is well-buffered. For every 10% sustained rise in oil and gas prices, GDP growth would fall by only 0.1%, among the lowest in the world, according to UBS estimates. While an energy importer, the country’s current account remains solid. In fact, China doesn’t quite know what to do with all the money it’s earned from a record trade surplus.

For emerging markets to outperform, many things have to be right. They are more sensitive to the global growth outlook. They’re also more vulnerable to hot money flows. At the onset of 2026, few would have thought that President Donald Trump would wage a war against Iran. Unfortunately, that black swan has arrived.

Look at what the world’s two most powerful leaders are up to. Trump is continuing his military operations against Iran because he believes the US “hasn’t won enough.” On the other side of the Pacific, it surely seems like Xi hasn’t earned enough from exports, either. Rather than using fiscal spending to stimulate the domestic economy, he’s banking on trade to meet the GDP growth target again. Emerging markets, unfortunately, are jinxed by these two men.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.