It’s the leveraged loan market’s liquidity paradox.

Selling pressure for leveraged buyout loans has been high all year, amid fears that artificial intelligence will damage or even bankrupt the software companies that account for a fair chunk of the market. But investors often aren’t offloading the riskiest debt — they’re shedding the loans that are easiest to sell, which are often bigger and comparatively safer.

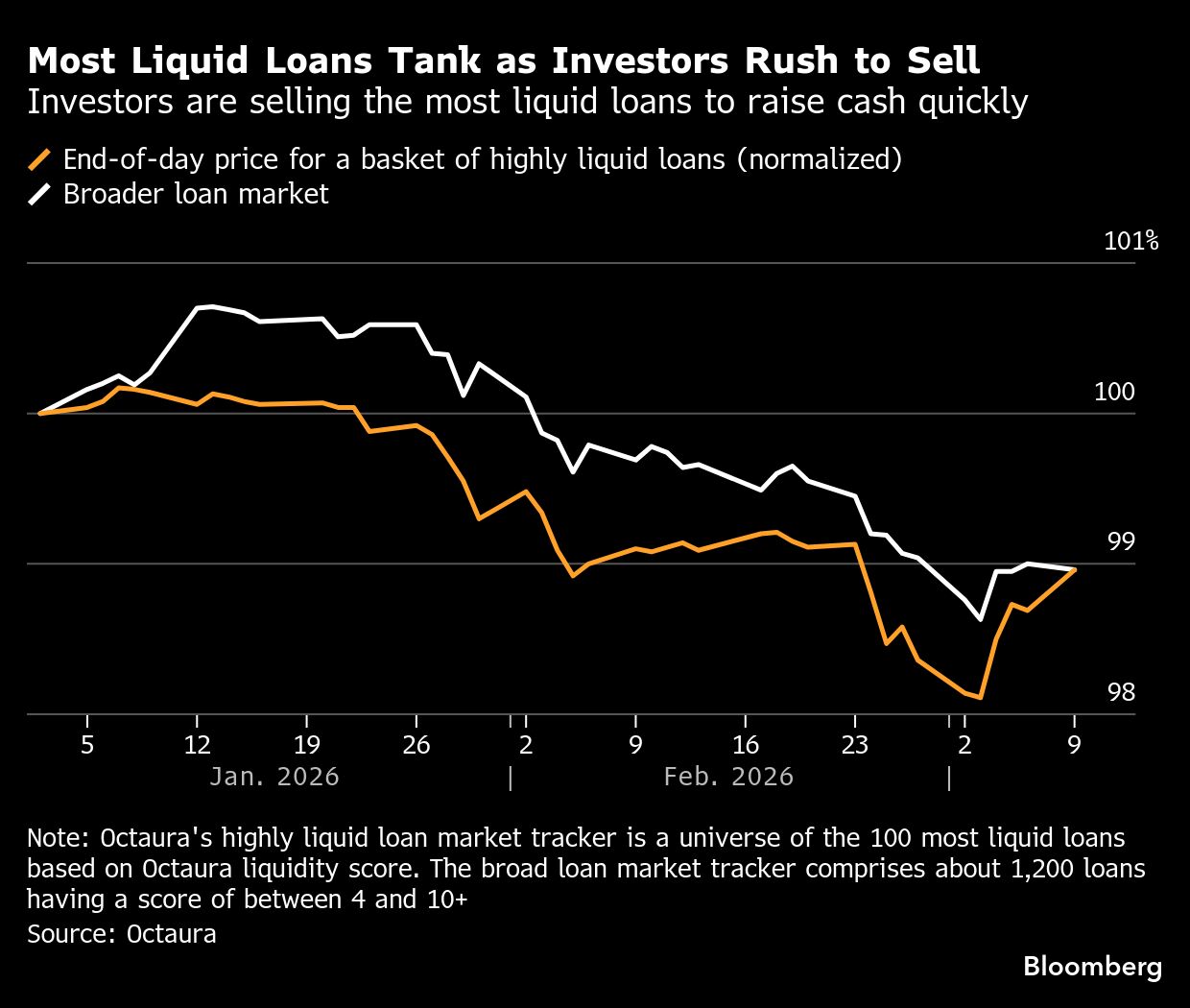

According to electronic trading platform Octaura, the average price on the 100 most liquid loans have fallen 1.04 cent on the dollar this year through Monday, compared with a 1.01 cent decline in the broader index. Some weeks, the difference is even starker: in the last week of February, the 100 most liquid loans fell 0.77 cent, while the broader index fell 0.4 cent.

The selling pressure on liquid debt in the $1.4 trillion US leveraged loan market highlights how price drops for individual loans may not reflect investor fears about credit risk for the borrower, but rather how easy it is to sell the loan. When funds need to raise capital and target selling the biggest, highest-quality loans, dealers often slash prices “hard and fast,” according to Grant Nachman, founder and chief investment officer at Shorecliff Asset Management.

“Even though small illiquid tranches are probably riskier, they can ironically appear less risky on the screens during periods of volatility,” Nachman said.

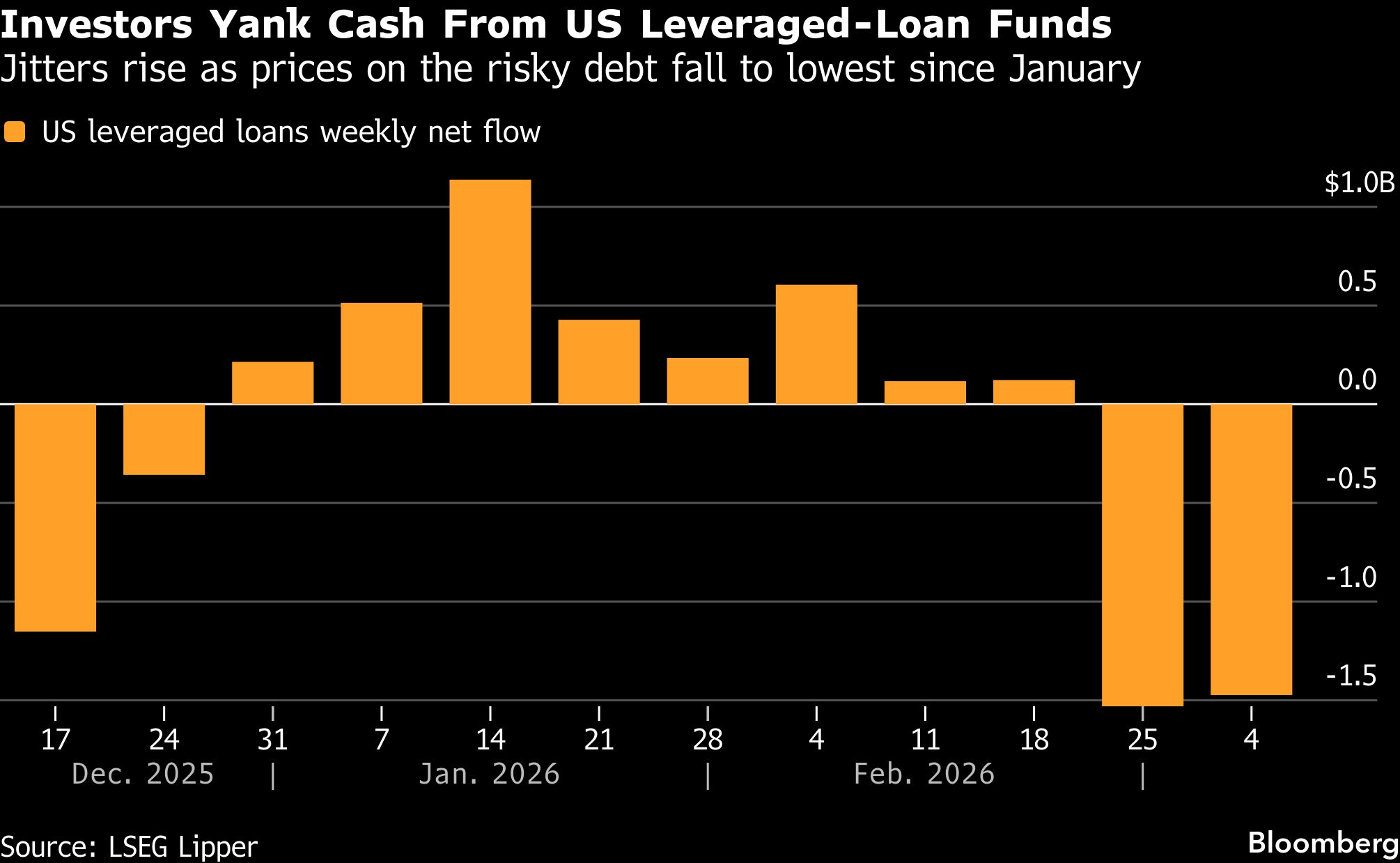

Investors in exchange-traded funds and other leveraged loan-focused vehicles are racing for the exits, with loan funds having seen two consecutive weeks of outflows exceeding $1 billion, according to LSEG Lipper data. Such selling can force managers to offload debt to meet redemptions, pressuring prices. Business development companies may also look to sell leveraged loans to meet redemption requests, according to Deutsche Bank analysts.

The impact is visible in the market’s largest benchmarks. The $6 billion Invesco Senior Loan ETF, which tracks around 100 of the largest and most liquid senior-secured loans, saw roughly $460 million of outflows last week, marking its sixth straight week of withdrawals and the longest streak since 2024.

Similarly, the roughly $5 billion State Street Blackstone Senior Loan ETF saw $276 million pulled, extending its run of redemptions to seven weeks — its longest weekly exodus ever.

Both ETFs slid last week to their lowest levels since the 2020 pandemic turmoil, pushing down prices that have drifted lower since mid-January over AI fears. Prices have improved this week after President Donald Trump’s remarks that the Iran war could be ending soon helped boost broader market sentiment.

“When people need to sell these liquid names, maybe they’ve become a little bit more bearish on the particular credit,” said Howard Cohen, head of markets at Octaura. “But an ETF manager per se, they have to raise funds in the names that they’re investing in.”

Weakness in the secondary market is also making it harder for companies to borrow. A $1.1 billion leveraged loan tied to chemical maker Arclin Inc.’s acquisition of DuPont de Nemours Inc.’s Aramids business priced last week at one of the steepest discounts for an acquisition financing in months.

The exodus highlights deepening concern over software sector concentration in the loan market. With 16% of the market exposed to those borrowers, US loans trail only private credit collateralized loan obligations, at 19%, and the 26% exposure held by business development companies, Morgan Stanley’s research shows.

Much of this exposure in loans is skewed toward the lowest-rated tiers, including B- and CCC, and largely private names, Morgan Stanley analysts including Vishwas Patkar wrote in a note dated Feb. 9. They expect defaults to probably stay low for now but anticipate price declines to potentially broaden and worsen, saying they prefer junk bonds over loans.

Sentiment has rapidly soured on leveraged loans, once a favored hedge against higher interest rates. The asset class is down about 0.8% this year on a total-return basis, ranking among the worst-performing corners of credit so far, although loans have broadly edged higher this week. While these floating-rate instruments thrive when yields climb, that advantage gets diminished by building growth concerns and credit stress.

Escalating tensions in the Middle East could lead to higher borrowing costs in the leveraged loan market as traders demand higher premiums to compensate for more risk. This could tighten liquidity and place additional pressure on loan borrowers looking to refinance debt and increase downgrades and defaults, prompting even more investors to dump their holdings.

“Pick the catalyst - AI, geopolitics, credit worries - as the backdrop flips to ‘risk off,’ credit vehicles like bank loans are not going to provide a safety cushion,” Todd Sohn, chief ETF strategist for Strategas. “I would expect more discounts and outflows assuming the risk backdrop remains bumpy.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.