One of my most longstanding and controversial opinions is that the move from defined-benefit pensions to defined-contribution pensions was a success. It’s an especially unpopular view amid stories of retirees who fall through the cracks and a grim market that is pruning many retirement accounts, if not retirement dreams.

Nevertheless, my position is unchanged. Baby boomers, in particular, are going into retirement better prepared than previous generations. The US retirement system certainly has room for improvement. But Americans don’t need more generous pensions, subsidies, or access to private equities and active management. Let’s stick with what’s working.

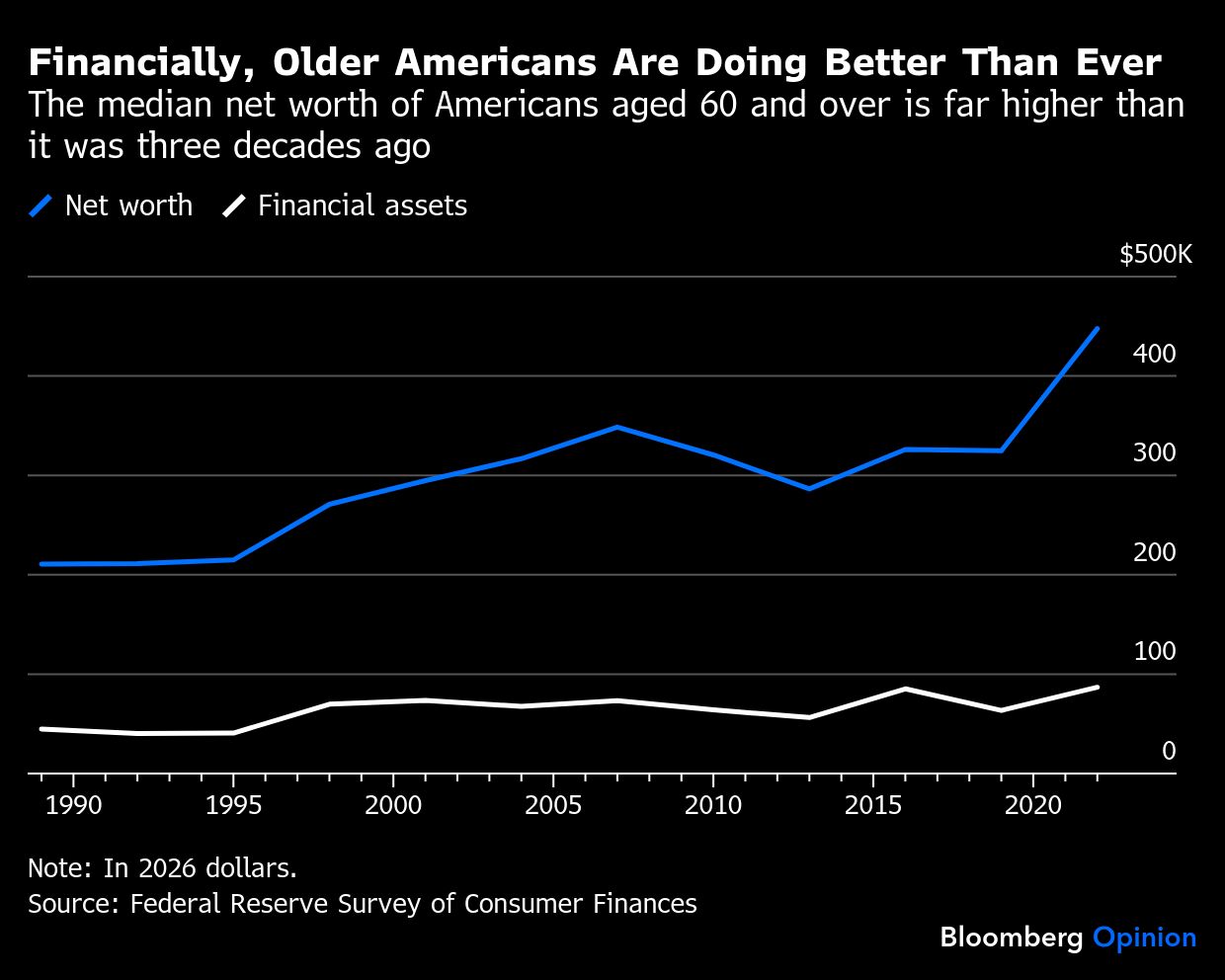

Consider those boomers and near-boomers. In 2022, Americans aged 60 and over had a median net worth of $448,000 and $87,000 in financial assets (in 2026 dollars). That may not sound like a lot to retire with. But in 1989, the same age group only had $210,000 in net worth and $45,000 in financial assets. It is also true that people are living longer — but they also tend to have less physically demanding jobs, which opens the potential for longer careers and more years of saving.

To be sure, these are averages, and some people are struggling. About 5% of Americans have only Social Security — but they tend to be people who had lower incomes while working and could not afford to save much. Social Security replaces a large share of their income, leaving many low-earning retirees better off than when they were working. Encouraging lower earners to devote more of their limited resources to retirement saving could make them worse off.

And Social Security and Medicare have become more generous over time. Older Americans are the least likely to live in poverty compared to other age groups. The government spends five times more on people over 65 compared to people under 18, and the older group just got a $6,000 tax credit.

The news gets better: Younger generations have even more financial assets than boomers did at their age. It is probably true most people would be even better off if they saved more. But if other generations got by, odds are that this one will, too. The bottom line is that a lack of retirement savings is not this country’s most pressing problem, and more tax benefits and subsidies for the elderly should not be its main priority.

One big reason retirees have more money is the move to defined-contribution pensions such as 401(k)s, which became popular in the 1980s. They are cheaper for employers and more portable across jobs, resulting in more consistent coverage. The period since the ’80s has also coincided with tremendous stock market gains, which made retirement accounts look even better. But market exposure means bearing more risk, and with a volatile stock market, the costs of a taking on that risk may soon be felt. There is no guarantee that the future will be as good as the past.

The asset management industry says it has a solution: Retirees should pay more fees by investing in active managed funds or private equity. This is exactly what they don’t need. BlackRock argues this will reduce risk, but it will do the opposite. Returns might look higher on paper, yet individual retirement accounts are not hedged properly to ensure predictable income in retirement, which should be the goal.

Getting people to save more for retirement was the hard part, and America has mostly succeeded. Sure, it’s always better to save more, but it is hard to argue that Americans aren’t saving enough for retirement. If you’re reading this, you’re probably doing OK in terms of how much you save. And if you avoid high fees or anything fancy, you are probably investing reasonably well and can survive a market downturn.

The federal government does not need to spend more on the elderly. The priority should be putting entitlements on a sustainable path, offering investors better options to reduce risk, and helping people get a predictable income once they retire. That’s easier than getting people to save or promising a shiny new benefit — but it’s not nearly as exciting.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager