The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

Last March, I attended the 2025 VettaFi-Exchange Conference. Of all excellent speakers, Ian Bremmer, President of the Eurasia Group, stood out to me. He was articulate and compelling in his talk on geopolitical market risk (summarized here). Regarding Europe, he stated (emphasis added):

Will they succeed in helping to ensure that they can have independent defense separate from the U.S.? I’m skeptical. I think [European countries will] fail [. . . ] Will they be able to implement on the Mario Draghi plan for competitiveness and build world-class technological corporations — their own serious unicorns — with supply chain that will support them, independent from the U.S.? And the answer to that is no. So, Europe is in serious trouble . . . this is late for them.

It was a talk I’ll never forget. Later that day, I spoke to Bremmer one on one and told him how much he depressed me, especially because I thought his logic was sound and his talk was brilliantly delivered. When we spoke, I found him every bit as personable as he was compelling. And he was mostly right. The relationship between Europe and the U.S. continued to sour, and the war in Ukraine seems to have no end in sight. I also suspect even Bremmer didn’t think European countries would be sending troops to Greenland to defend against a possible invasion by the U.S.

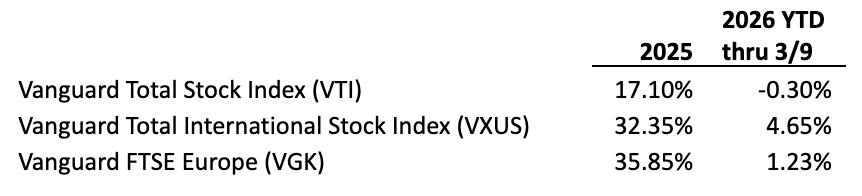

Both during and after the talk, my instincts were to immediately tell my clients to get out of European equities and to follow that plan myself. Fortunately, I learned a long time ago not to act on my instincts or even economic forecasts. I say “fortunately” because European stocks more than doubled the return of U.S. stocks in 2025 and are besting U.S. stocks so far this year.

To be clear, Bremmer never said to jettison European stocks, though I suspect I wasn’t the only one in the audience that wanted to dump those holdings after his talk. Why did European stocks do so well? I could list several reasons and some might actually be right. But the real lesson is that markets constantly fool us. The bleak forecast and logic were already priced into European stocks.

Are Bonds Easier to Predict?

Many people seem to think they know where interest rates are heading. Certainly, the Federal Reserve Open Market Committee signals the direction it is leaning on the Fed Funds rate. But that is only the overnight rate, and it only affects very short-term bonds. What about intermediate-term rates like the ten-year Treasury bond?

One study shows those economists have been consistently wrong, with a bias of rate increases that never happened. Another study by the Federal Reserve of St. Louis examined the historical accuracy of professional forecasters in predicting the 10-year Treasury bond rate the following year between 1993 and 2004. They then looked at the range of the average bottom 10 and average top 10 forecasts. The actual number fell within that range only 47% of the time. Similar dismal results were found on forecasts of unemployment, real GDP growth, and inflation, measured by the CPI.

Why We Love Expert Predictions

In the book “What’s Wrong with Expert Predictions?”(Cato Institute 2011), Dan Gardner and Philip Tetlock make the argument that experts must love making predictions. They keep right on predicting, even though by any reasonable standard, they're terrible at it. In fact, Gardner and Tetlock make the argument that economists are no better than the proverbial dart-throwing chimp at predicting the economy.

In the same book, John Cochrane, University of Chicago professor and senior fellow at the Hoover Institution at Stanford, says economic forecasting isn’t very accurate and financial forecasting is next to useless. He argues that if there were easy or mechanical ways to tell with any certainty that the market would go up tomorrow, forecasters could make a fortune. He then says all the people following the forecast would bid up prices today, to the point where no one could tell with any certainty whether markets would rise further or fall.

Professor Cochrane once told me, “Economic forecasters using fancy models don’t do substantially better than simple forecasts using historical correlations.” He believes that some economic forecasting is better than random guesses, but it’s next to useless when it comes to investing.

What Makes a Good Forecast?

The simple question of what makes for a good forecast result is a complicated answer. I’ll start with bad predictions. I ignore forecasts from stock gurus such as those on the financial TV channels. They mostly do the following:

- Come across as very sure of themselves

- Give numbers and dates, but never both at the same time

- Brag about their winners

- Appeal to emotions

- Forecast the past

- Tell followers they are beating the market

- Call themselves “contrarian”

I’ve found good forecasts are probabilistic using longer time horizons. They give ranges of returns rather than specific numbers. They also focus on risks, clearly stating what can go wrong, and are delivered with humility rather than overconfidence and boastfulness. The forecast I value the most is Vanguard’s Market Perspectives, which meets the characteristics of a good market forecast. However, while I enjoy reading forecasts periodically as it satisfies the part of my brain that wants to know the future, I have yet to make a single change in my portfolio or recommendations to clients based on one.

Conclusion

It’s human instinct to want to know what the future holds and to protect and grow our nest egg based on our perceived knowledge of the future. It takes courage to ignore those economic forecasts from brilliant, well-meaning experts with very impressive credentials. Their logic is always compelling, but investing based on that logic can be hazardous to your wealth.

Before you make changes to portfolios based on forecasts, ask yourself these three questions:

- Have you checked the track record of the forecaster or economic forecasts in general?

- Do you have any evidence that this forecast hasn’t already been priced into the market?

- Do you want to make changes to your portfolio based on this forecast, even though you know the herd is also making these changes and following the herd typically ends badly?

I’m a believer that rules, such as those that determine asset allocations and rebalancing schedules, work better than investing based on forecasts.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.