The Federal Reserve is about to give America’s biggest lenders an extra $200 billion of capital to play with. Later this week, US regulators will launch fresh proposals to update and, in some ways, loosen US capital rules that will fuel stock buybacks, lending and trading. But there’s a danger here: Too much haste in deploying all this spare cash risks overheating the economy and housing markets in unhealthy ways.

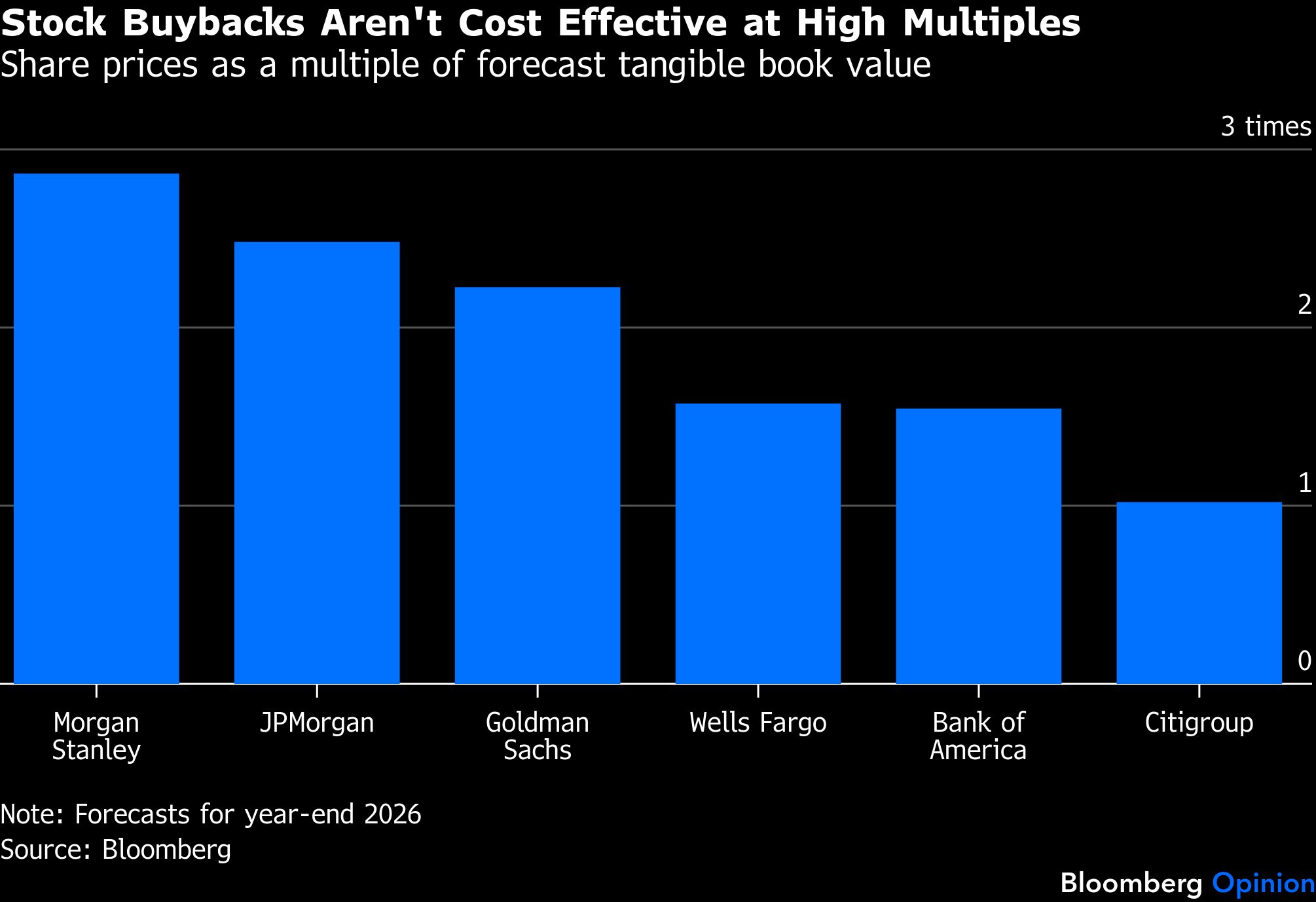

Having so much additional capital will present the biggest banks with tricky choices. Goldman Sachs Group Inc., JPMorgan Chase & Co. and Morgan Stanley will each have to think twice about handing billions of dollars straight back to investors through stock buybacks — an expensive exercise because their shares are so highly valued. But all large lenders should be wary of growing their loan books rapidly because that almost always leads to higher bad debts as lending standards slip.

Republican leaders at the Fed and two other watchdogs are ripping up the previous Democrat-sponsored proposals for updating capital rules after a disastrous attempt to get tougher on banks that kicked off in 2023. The Fed’s then-vice-chair for financial supervision, Michael Barr, had tried to force big lenders to meet capital hurdles that were nearly 20% higher than existing rules.

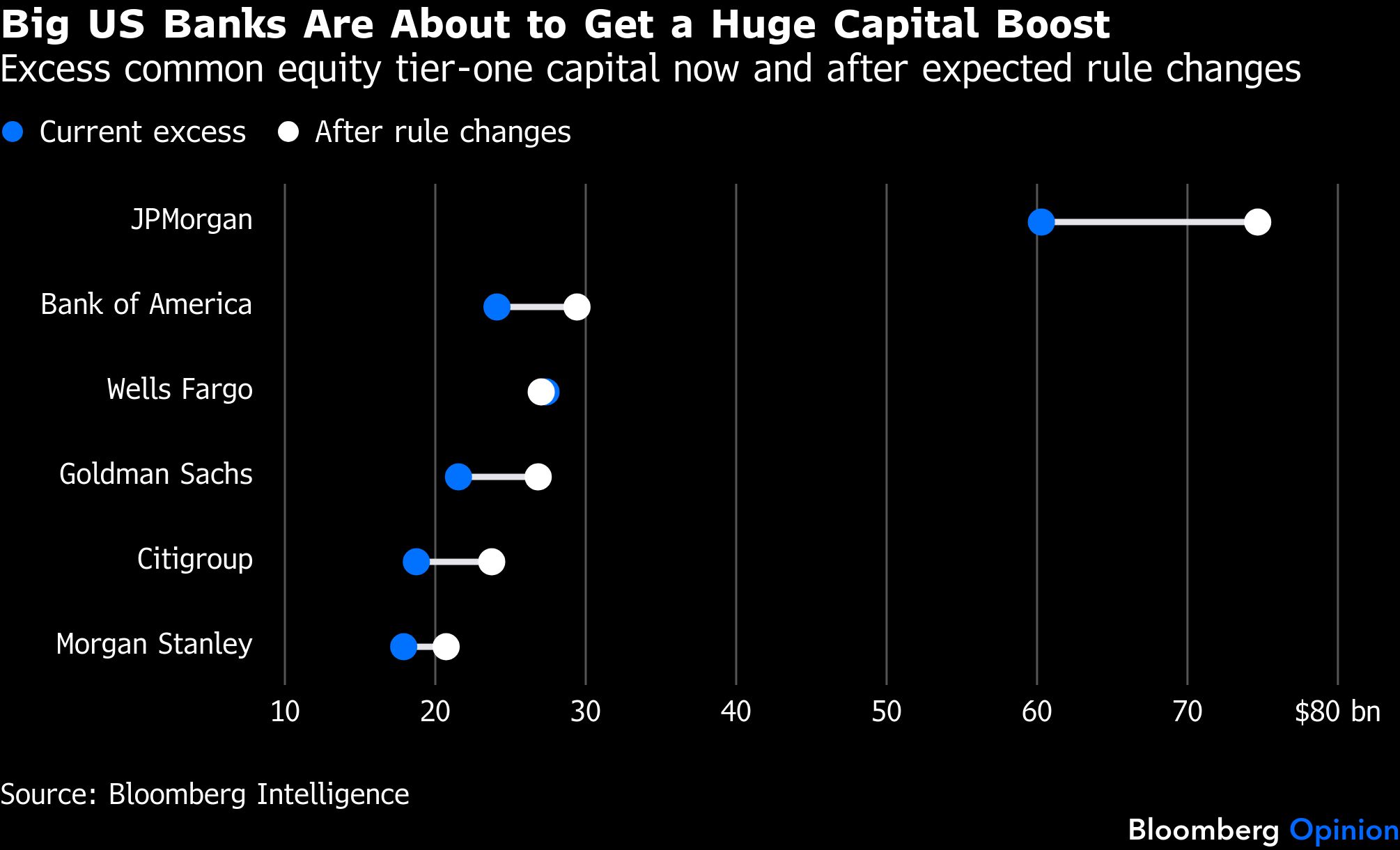

The big six banks held back billions in profits over the past couple in anticipation of Barr’s stiffer standards — most of the $200 billion about to be freed up is just that money being no longer needed. There looks likely to be more gains on top, however. JPMorgan, for example, has about $60 billion of excess common equity tier-one capital (as it is technically known) that was retained to prepare for the Democrat plan. The new Republican proposals could boost that to $75 billion, according to Bloomberg Intelligence.

Michelle Bowman quickly scrapped the previous proposal and started again when she was handed Barr’s role by President Donald Trump last year. She set out to review the capital rules, the extra charges applied to systemically important banks and how all of these requirements interact with stress testing. Bowman and others in the administration also wanted to undo some of the regulatory arbitrage that has squeezed so much lending out of banks and into less regulated funds and other sources of finance, including private credit.

Two new proposals are due to be released after the Fed holds an open board meeting on Thursday, Bowman said in a speech last week. They will aim to bring US rules more in line with the international standards already adopted in Europe and overhaul America’s much tougher systemic risk requirements for its largest banks. “Together, these proposals would decrease the requirements by a small amount,” she said.

In dollar terms, JPMorgan will be the biggest beneficiary through its sheer size, but the rest of the big six will also end up with between $20 billion and $30 billion of spare capital, according to Bloomberg Intelligence. To get a sense of the new lending that could generate, apply a reasonable common equity tier-one ratio of 12% and that supports nearly $1.7 trillion of additional risk-weighted assets — roughly equivalent to adding another Bank of America Corp. to the US financial system.

Turning all that financial firepower onto the US economy in one go would be disruptive, to say the least. So where will the money go? Citigroup Inc. could buy back stock at the best rate of return for shareholders because of its lower valuation; Bank of America and Wells Fargo & Co. are also likely to increase buybacks, although at higher multiples of book value their returns won’t be as good.

The investment banks could also use this extra balance-sheet capacity to trade more in financial markets. However, Bowman’s speech suggested that measures of market risk will be tightened, by capping the benefits investment banks get from using their own internal models to make these assessments rather than standard models created by regulators. This is similar to the rules Europe and the UK are also waiting to implement. So US banks could still increase their dealing activities because they’ll have more capital available, but they won’t necessarily make a better rate of return than they do today or suddenly become even more competitive versus non-US rivals.

The third option is growing loan books, and Bowman was clear last week which areas she expects to benefit. The existing rules have been overly tough on low-risk activities such as mortgage origination and servicing, and lending to businesses, she said, which had pushed these traditional products into less regulated markets.

The changes to mortgages will be welcomed by many hoping to lower borrowing costs and improve affordability for wannabe homeowners. Unfortunately, the perennial lesson of housing markets is that cheaper debt typically just boosts house prices instead.

Consumer credit and small-business loans should also get a boost, according to research by Morgan Stanley analysts, as should lending to private companies, but only for relatively safe investment-grade borrowers and not riskier private equity buyouts. That last tweak will please European lenders; Deutsche Bank AG and others are trying to persuade their regulators to make a similar treatment for non-public companies permanent in local rules.

Ultimately, a lot of what Bowman is likely to propose looks sensible and in line with other jurisdictions. However, the buildup in extra capital at the biggest US banks means they’re about to have a lot of extra financial power to unleash. If it hits the economy quickly, it will be like a big injection of stimulus — at the very least that will make it much harder for the Fed to cut interest rates, as Trump wants. Bowman and her fellow regulators should look to slow the huge capital release that’s coming, or within a few years they might come to regret it.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul J. Davies