Public markets give a running commentary on the biggest players in private markets. Over the last year, this has gone from good to bad to worse. The sector’s long-term growth prospects may be more-or-less intact, but the next few years probably won’t feel that way.

Investors are prone to bouts of exuberance and gloom about private-market investment firms. Shares in Blackstone Inc., KKR & Co., EQT AB and peers fell in late 2021 as investors anticipated the end of the low interest-rate era, robbing the industry of cheap financial fuel. They regained their mojo in response to new fee-garnering opportunities from raising private credit funds — which lend directly to companies — and tapping wealthy retail investors (often in tandem). Donald Trump’s 2024 presidential election victory was seen as good for dealmaking and provided a further leg up. Blackstone president Jon Gray said last year the “deal dam is breaking.”

Then came another downswing. Corporate failures such as auto-parts supplier First Brands Group, coupled with fears that artificial intelligence could disrupt software firms, prompted concerns about private credit’s resilience. Retail investors have been yanking what money they can from the asset class. And the prospects for selling companies and realizing gains have dimmed amid the financial fallout from the US and Israeli attacks on Iran.

These developments undermine the sector’s investment case, which rests largely on a simple notion: gathering a lot of sticky client money. The base fees from managing funds (as opposed to taking a cut of investment gains) are the draw. This revenue stream is cherished because private-capital managers lock up client cash for several years. Even semi-liquid retail money has some (entirely appropriate) restrictions on withdrawals. Moreover, this tasty revenue ought to enjoy sustained growth amid the secular shift from public-markets investing to private.

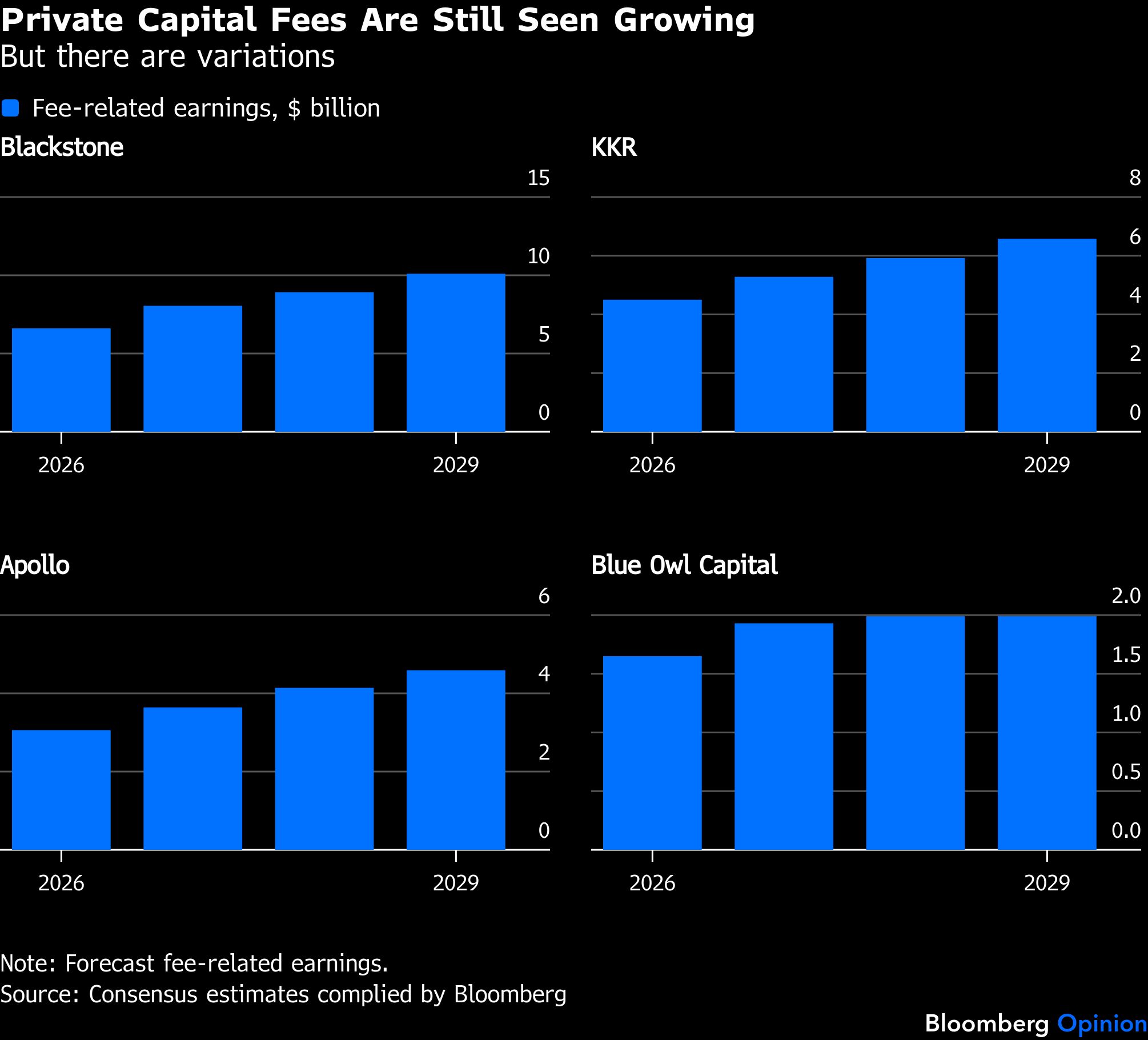

The most closely watched metric is “fee-related earnings,” usually made up of management fees plus certain performance fees that don’t depend on asset sales. Analysts typically value predicted 2027 FRE on 20-something multiples. For comparison, the S&P 500 index — which includes all of the Magnificent Seven tech stocks — trades on 18 times earnings, according to Bloomberg data.

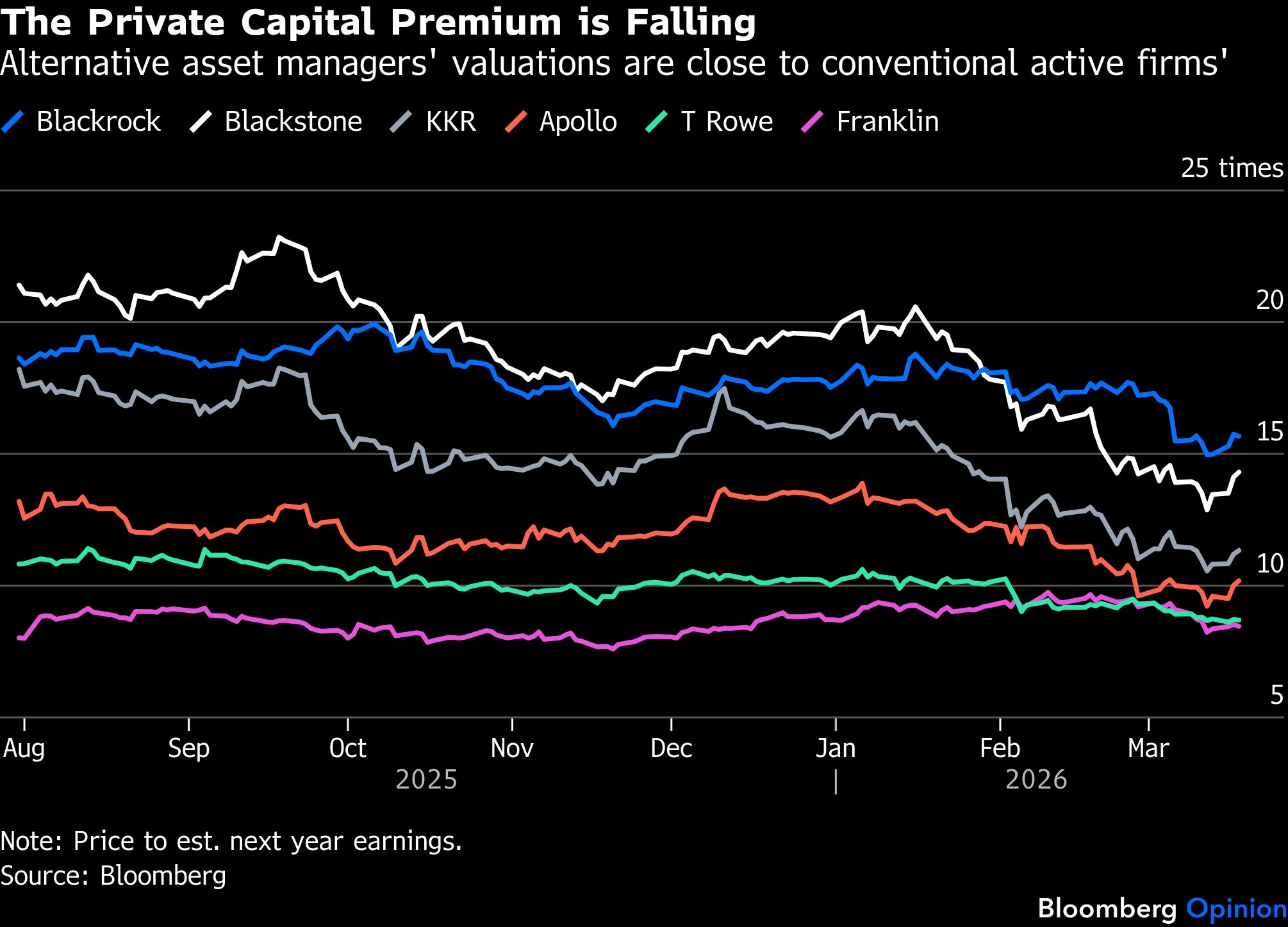

The overall price-to-earnings ratio for these private-capital giants — also known as alternative-asset managers — is typically a few notches lower as it’s diluted by less highly valued profit streams, such as the unpredictable fees on capital gains. Some firms also own an insurance business and that lowers the valuation multiple further still.

Even so, the market values of these larger firms (roughly 9 to 14 times 2027 earnings, and about 12 on average) imply valuations for those fee-related earnings that are far lower than what most Wall Street analysts have modeled.

Indeed, valuations are sliding closer to those of the old active-fund managers that the private-capital firms have been usurping. Price-earnings ratios are back to 2023 or 2022 levels, and below their five- and 10-year averages. That may look like a buying opportunity. But the sheer uncertainty of the outlook for management fees justifies caution. If earnings forecasts fall further — and analysts are already snipping — those shares won’t quite look so cheap.

The rush for retail money has turned into a near-term problem rather than a reliable boost for fee earning. Goldman Sachs Group Inc. research anticipates a 20% to 30% hit to the value of private credit retail products over the next two years caused by net client outflows.

Assume also that the war means more difficulties this year in selling companies and other investments, of which there’s already a huge backlog. That would make fresh fundraising harder and weaken the sales pitch. If fears of severe private-credit defaults materialize, things just get worse.

This isn’t a homogeneous industry. Some firms, including Blackstone and Partners Group, have put more faith in tapping US retail clients than others. Some are more diversified than others. Maybe institutional money will in step where retail clients exit; maybe retail investors will keep their money with these firms but divert it away from credit funds.

Flows into private equity and infrastructure funds have generally increased as private credit flows have slowed in recent months, notes JPMorgan Chase & Co. research, and private equity returns have generally improved as direct-lending returns have slid. CVC Capital Partners Plc last week said its latest fundraising could match or beat the €26 billion ($30 billion) record it set in 2023. Quite a statement in the current environment.

Alternative-asset management hasn’t gone “ex-growth” — the financial jargon for mature and stagnating industries — unlike their conventional active rivals. Moreover, sentiment toward private-capital managers has a habit of turning rapidly. But, as UBS Group AG’s Michael Brown warns, the sector is in a “positive catalyst desert.” To regain stock-market favor, these firms will need to offer solid evidence that the asset-gathering juggernaut is motoring again.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes