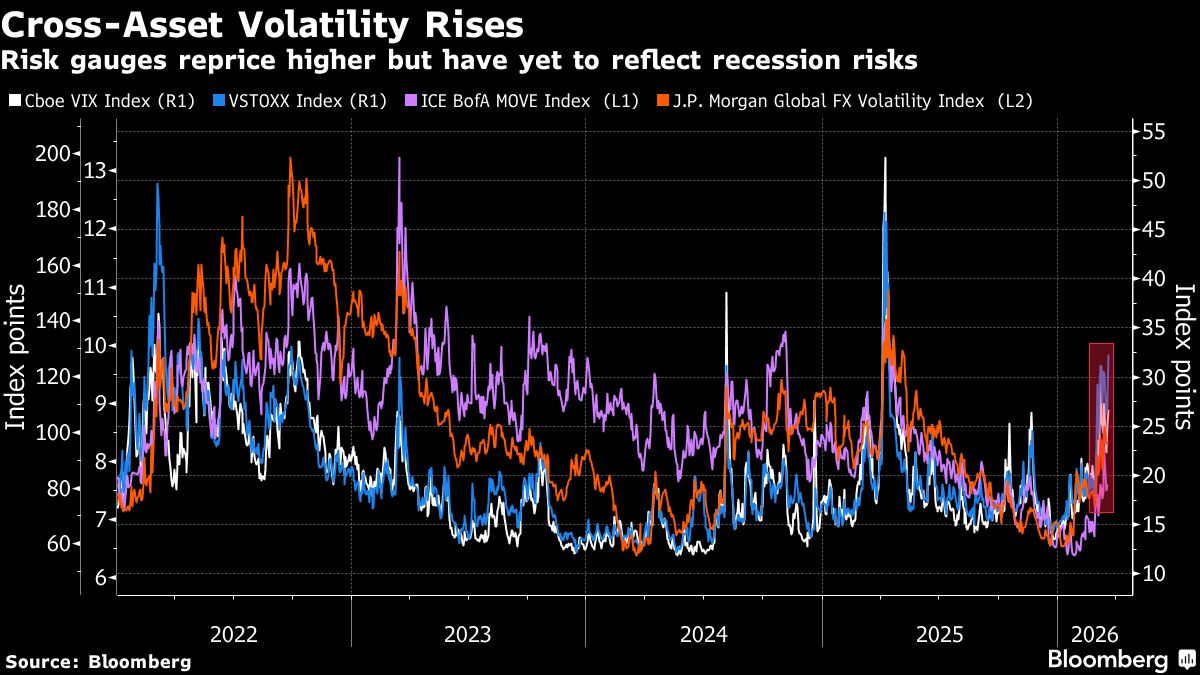

Confidence among global stock-market investors, who largely kept their cool in the face of an escalating conflict in the Middle East, is starting to wear thin.

Three weeks since the war in Iran began, concern is now growing that the conflict won’t end anytime soon — and that its impact on the economy and the stock market will be more severe than previously expected. The S&P 500 is down 1.6% over the past two sessions, breaking below its 200-day moving average and hitting a four-month low. Europe’s Stoxx 600 benchmark plunged 2.4% on Thursday, hitting a three-month low.

According to Goldman Sachs Group Inc.’s trading desk, clients who previously expected a quick resolution to the Iran war are starting to have doubts. While some remain bullish, another cohort of clients now either anticipates a stock-market correction or a slow and steady grind lower similar to that of 2022, Goldman’s Shawn Tuteja wrote in a note.

“While there remains a camp that believes the situation resolves in the next week or two, a narrative is starting to form that there’s no end in sight,” Tuteja, who oversees the ETF volatility options trading businesses at the firm, wrote in the note on Thursday. “We’ve seen clients express both of these latter views of a move lower.”

The conflict in the Middle East is adding a new stress point to the market already dealing with artificial intelligence’s potential disruption to many companies’ business models, as well as worries around writedowns to private credit and sticky inflation.

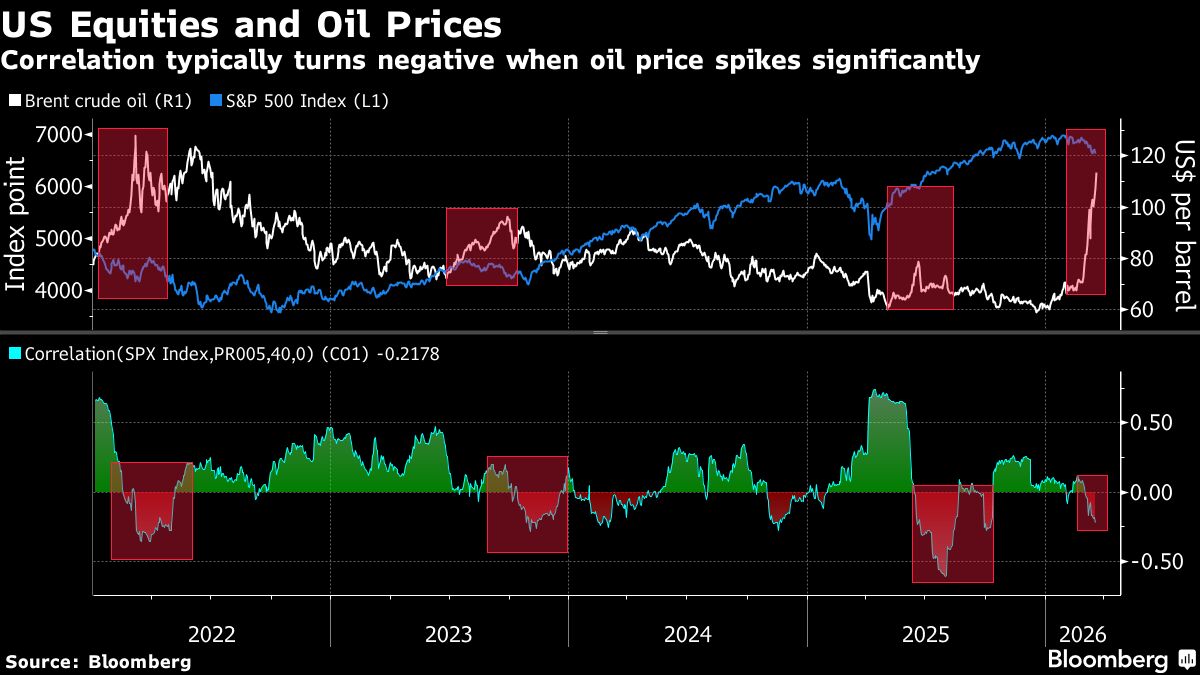

For strategists at JPMorgan Chase & Co., investors have initially failed to price the potential economic damage from soaring energy prices and other strains caused by a prolonged shutdown of the Strait of Hormuz, despite the fact that four out of five oil shocks since the 1970s have led to recession.

“While some of the froth has been taken out of high-risk factors and speculative areas of the market, we still see complacency,” the strategists said in a note. They added that correlation between the S&P 500 index and oil typically turns “increasingly negative” when crude prices spike by about 30%.

Higher for longer oil prices would not only rekindle inflationary pressures, weighing on consumer spending power in the process, but would also cause Wall Street to downgrade its growth outlook, the JPMorgan team warns. Should oil remain at current levels for the rest of the year, earnings estimates for S&P 500 firms could shed as much as 5 percentage points, strategists said. And each sustained 10% increase in oil could shave 15 to 20 basis points off economic growth.

“The immediate, first-order effects of the Iran conflict, such as rising oil prices, are well appreciated by markets,” said Daniele Antonucci, chief investment officer at Quintet Private Bank. “What’s less examined are the second-order consequences such as the impact on oil-importing and oil-exporting industries, and on sectors indirectly linked to energy flows.”

Still, optimists expecting the stock market to find a floor near current levels may have history on their side. The S&P 500 has declined about 4% in the 14 trading sessions since the war in Iran began. Historically, that’s about where the gauge found a bottom after similar conflicts.

Strategists at Deutsche Bank AG analyzed more than 30 major geopolitical shocks going back to 1939 and concluded that the S&P 500 found a floor on average around the 15th day into a conflict. At its lowest point, the gauge traded on average a little more than 4% below its pre-conflict level.

“Investors are stuck in geopolitical pinball right now,” said Max Gokhman, deputy chief investment officer at Franklin Templeton Investment Solutions. “Literally and figuratively explosive developments are bouncing global market sentiment all around a board that seems tilted to the downside given that any claims of the war ending soon lack the substance of a clear offramp.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Joel Leon, Natalia Kniazhevich