Modern markets have gotten used to central bank support whenever the global economy wobbles. But as the world confronts a fresh energy shock unfolding against brittle labor markets, investors need to prepare themselves for the possibility that central bankers won’t have their backs — quite the opposite.

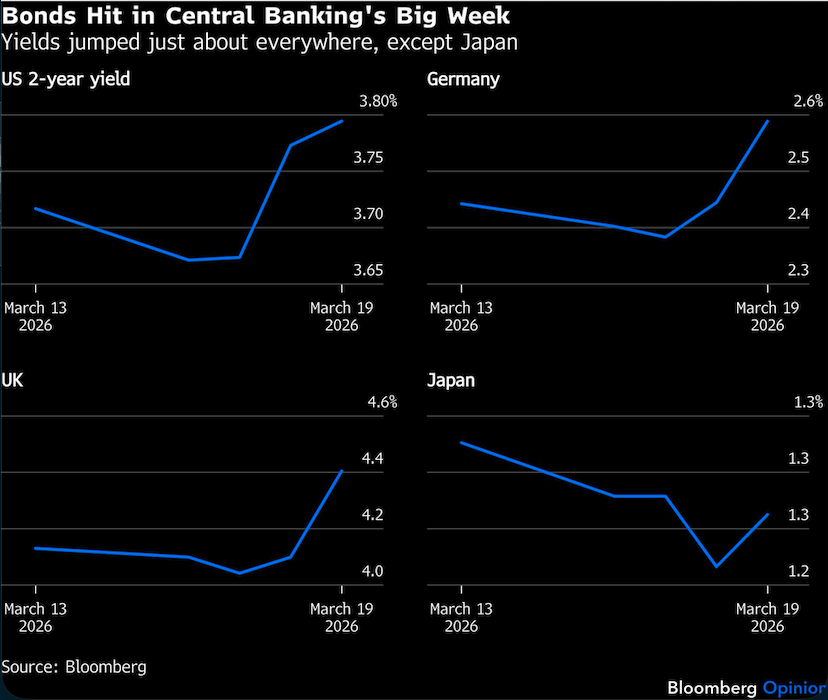

Markets had a relatively hawkish read on one of the busiest weeks in central banking in recent memory. Two-year government bond yields jumped in the US and across Europe’s major economies as the Federal Reserve, European Central Bank and Bank of England sprinkled more than an ounce of inflationary caution into their decisions to leave interest rates unchanged. Traders largely abandoned the pre-Iran war idea that benchmark rates would tick lower in the US and UK this year to support job growth.

The outlier was Japan, a market that’s uniquely susceptible to the conflict given that it gets over 90% of its oil from the Middle East. Short-term yields were relatively stable on the week even though the Bank of Japan’s decision was widely characterized as a “hawkish hold.”

Whether policymakers end up focusing on inflation or growth will depend on the duration of the US-Israeli conflict with Iran. The effective closure of the Strait of Hormuz is hammering economies around the world, albeit in subtly divergent ways. Although Europe doesn’t rely as directly on Middle East supplies as Asia, it’s still highly vulnerable to spikes in global energy prices, as the Russian invasion of Ukraine laid bare in 2022. The United States, now a net energy exporter, is a consumption-dominated economy. While oil-rich states such as Texas may see a windfall, consumers across the country are losing confidence as gasoline prices at the pump surge toward $4 a gallon. At another extreme of the commodity exporting spectrum, the Reserve Bank of Australia actually hiked rates on Tuesday amid already-elevated inflation.

Economic orthodoxy would typically have central banks “look through” temporary supply shocks, but policymakers generally agree that all bets are off if the public’s inflation expectations lose their anchor. In the past six years alone, the world has confronted the supply-chain bottlenecks of the Covid-19 pandemic, the war in Ukraine, Donald Trump’s sweeping tariffs — and now this. Whatever the textbooks may say, these types of inflationary episodes may no longer feel temporary. Clustered together like this, the risk is that inflation is starting to get embedded in the global psyche and could, therefore, be harder to root out.

It is, of course, important to differentiate between the various shocks. This latest rupture, for instance, finds the world in a vastly different place from where it was when Russia invaded Ukraine. Policy rates are starting from a higher base, and unemployment has been subtly moving higher in many advanced economies including the US and Germany. Gone are the post-pandemic impulses to spend with abandon after being locked inside for many months. And in the US, consumers have spent down the excess savings that cushioned the world’s largest economy in recent years.

Policymakers must remain vigilant about fragile inflation expectations, but they also can’t rule out the possibility that rising energy prices may deliver a more consequential hit to growth and zap confidence.

The problem is that the threats can still break in either direction, making central bank communication extremely difficult — and forward guidance impossible.

The BOE said it “stands ready to act,” triggering a wave of hawkish bets in markets, although Governor Andrew Bailey subsequently came out and cautioned against “strong conclusions.” The ECB would be ready to raise rates as soon as their next meeting, though a later date may be more appropriate, Bloomberg News reported Thursday, citing people familiar with the situation. In the US, the median Fed policymaker in the Summary of Economic Projections revised their forecast for PCE inflation for this year to 2.7% from a prior 2.4% (their target is 2%), while leaving their policy rate outlook unchanged at one cut in 2026. But Fed Chair Jerome Powell characterized the uncertainty thusly:

The thing I really want to emphasize is that nobody knows. You know, the economics effect could be bigger, they could be smaller, they could be much smaller, or much bigger... if we were ever going to skip an SEP this would be a good one... because we just don’t know.

It could be months before policymakers are able to take concrete action to cushion any hit to economic growth. The timing will depend on each country’s varying exposure to the energy supply chain and the differing mandates of central banks. The Fed’s focus, for example, is on stable prices and maximum employment, while the ECB’s single mandate is inflation.

For now, the world’s most important monetary policy authorities have a common message: They are in wait-and-watch mode and almost certainly won’t be coming to the market’s rescue anytime soon. From an investor standpoint, that means proceeding with extreme caution.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.