Banks making loans to specialist fund managers instead of directly to companies is meant to act like a firebreak protecting traditional lenders against the risks of businesses going bust. But losses from financing private credit firms and other nonbank lenders are coming back to bite them — and it’s making their investors antsy.

While the direct exposure of most banks to private credit is a sliver of their lending, they still need to reassure shareholders that standards have been exacting and that they have proper oversight of the collateral pledged by borrowers.

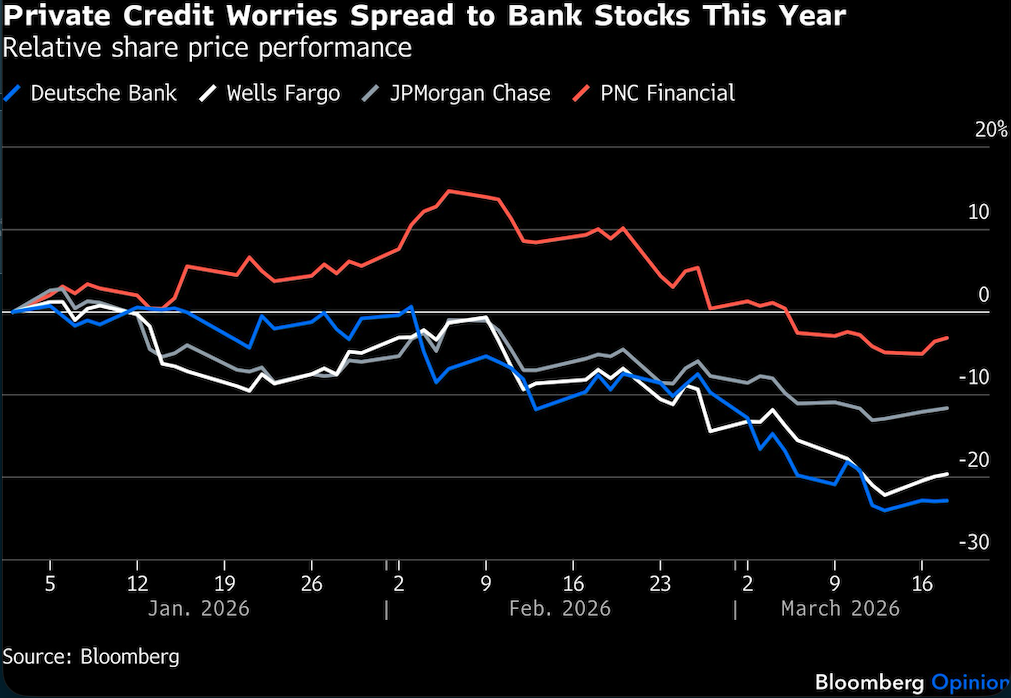

A string of blowups in recent months has already led to losses for banks that loaned money to firms including Tricolor Holdings LLC, First Brands Group LLC and Market Finance Solutions Ltd. Now, growing worries about the creditworthiness of private equity-backed software companies in particular has hit the stock prices of US and European banks.

Deutsche Bank AG Chief Executive Officer Christian Sewing had to reassure investors after the German lender’s stock fell 7% earlier this month when its annual report revealed it was owed €26 billion ($30 billion) by private credit firms. Sewing told a conference in London last week that his bank had never lost money on such deals in a decade, and was very comfortable with its underwriting. Executives from Societe Generale SA and UBS Group AG also aimed to tackle investor concerns about the sector at the same event.

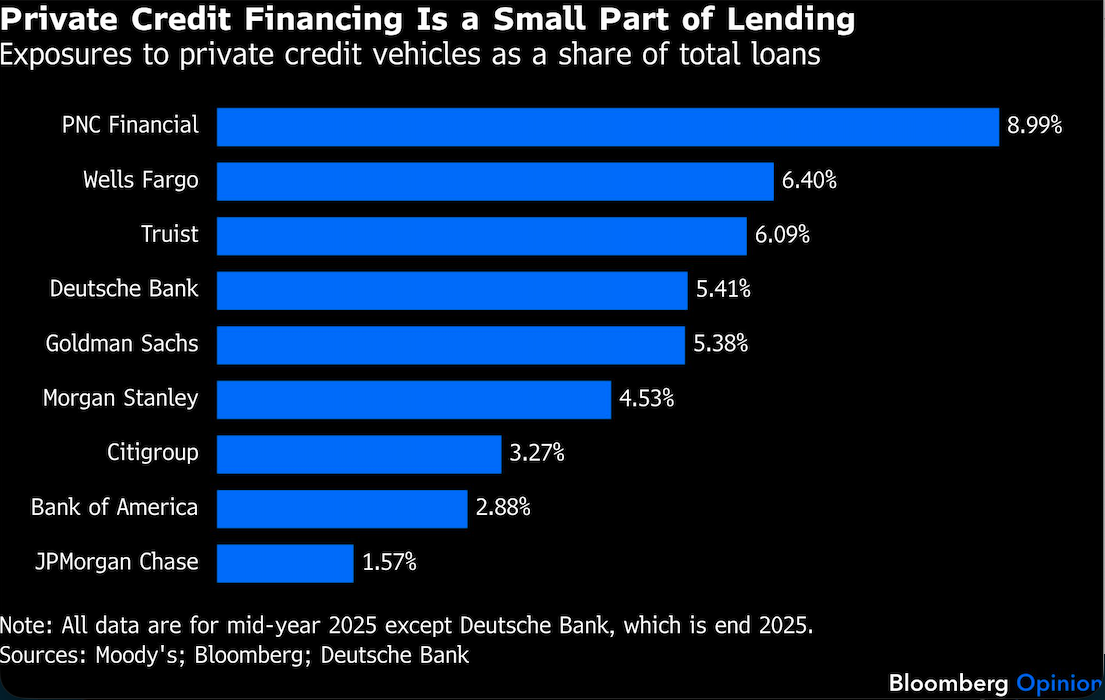

JPMorgan Chase & Co., meanwhile, laid out details of its exposures to all nonbank financial firms at its full-year results in January. It took a hit from the collapse of Tricolor last year, prompting CEO Jamie Dimon to warn that more cockroaches would emerge from lax credit underwriting. The US bank’s total exposure to nonbank lenders is about $160 billion, but within that its financing of private credit funds, business development companies and other vehicles that lend to buyouts was only about $22 billion in the middle of last year, according to Moody’s Corp. That ranks it behind four other US banks; Wells Fargo & Co, the leader in this market, is owed nearly three times as much. Yet even at Wells Fargo, private credit funding amounts to only 6.4% of total loans, while at Deutsche Bank it’s less than 5.5% and at JPMorgan less than 2%.

The exposures are bigger as a share of core capital — the loss-absorbing equity that makes up a fraction of a bank’s balance sheet — and that’s what shareholders look at in times of trouble. Loans to private credit are equivalent to nearly half of Wells Fargo’s common equity and more than half of Deutsche Bank’s. Meanwhile, PNC Financial Services Group Inc., a super-regional lender, has provided private credit financing equivalent to 65% of its core capital, according to Moody’s.

Still, banks would only suffer a painful knock to profits — not a mortal wound — even if private credit defaults spike as high as 15%, an extreme forecast from UBS strategists, and recoveries from failed loans are as low as 20%, the worst predicted by an Apollo Global Management Inc. executive in recent remarks reported by the Wall Street Journal.

But banks need to worry about the cost of lawsuits and reputational hits, too. JPMorgan, Barclays Plc and Fifth Third Bancorp are being sued by investors who bought notes issued by Tricolor, for example. Jefferies Financial Group Inc. faces claims from fellow lender Western Alliance Bancorp alleging fraud over the failure of First Brands last year. Ken Vecchione, Western Alliance’s CEO, said in his career he’d never seen a counterparty so deliberately place its reputation and integrity at risk as Jefferies had. Jefferies has denied the allegations. The hard-charging investment bank and its asset management arm are also in legal fights related to other nonbank finance firms it’s involved with; it was also one of the biggest creditors of the UK specialist mortgage business Market Financial Solutions that failed this month.

The key question for bank shareholders is whether this is all a relatively normal turn in the credit cycle after a long period of free-flowing capital, or if banks have been inattentive in assessing the firms they financed and their collateral. Fraud is fraud, but keeping track of the assets you are lending against is supposed to be a pretty basic skill for a banker.

Some of the worst risks may be on the books of second- and third-tier lenders in the US and Europe who’ve grown this kind of business aggressively in recent years, according to Moody’s. But even at the biggest lenders, there is often a lack of diversification — most have made almost all of their loans to their 20 biggest private credit clients.

JPMorgan is already cutting back, by marking down the value of individual loans in its clients’ portfolios, which clips the maximum amount of debt those clients can take on. Many others didn’t include similar defenses in their documentation, but may still be able to trim the loan-to-value limit up to which clients can borrow.

All banks should look to protect themselves better right now. Smart investors in business development companies may be pulling their money out to exploit the unwillingness of fund managers to mark down the value of loans they hold. Those investors might be getting an artificially high price, which is a bad deal for their peers who aren’t withdrawing cash — and for the banks lending against overvalued portfolios.

Private credit markets are being forced to grow up and deal with the errors of youthful exuberance. Some of the outcomes won’t be pretty. Investment and commercial banks should always have been the adults in the room while the party was raging, but many of them look like they’re going to have to relearn some painful credit lessons too.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.