Private credit funds lent a lot of money to software companies at the beginning of the decade when they were being snapped up in a rush of expensive buyout deals. Now many of these tech businesses are braced for disruption by artificial intelligence, and some might end up defaulting on that debt. I fear private credit firms won’t recover as much of their loans as they’d hoped.

Lenders expect a certain amount of trouble when backing riskier midsized companies. Losses depend on the number of defaults in their portfolio as well as how much value they’re able to claw back if there’s a problem. While the number of these businesses defaulting on their borrowing isn’t high by historic standards yet, creditors need to worry about the second part of the equation.

In years past, lenders relied on their ability to recoup much of the value of a soured loan, meaning even a largeish number of defaults could be managed. Things might be different this time. A private credit loan made to a generic small or midsized software company might recover 20-40 cents on the dollar, according to comments attributed to Apollo Global Management Inc.’s John Zito in the Wall Street Journal this month.

He could be right. If enterprise-software business models are made obsolete by AI, the underlying assets might retain little value.

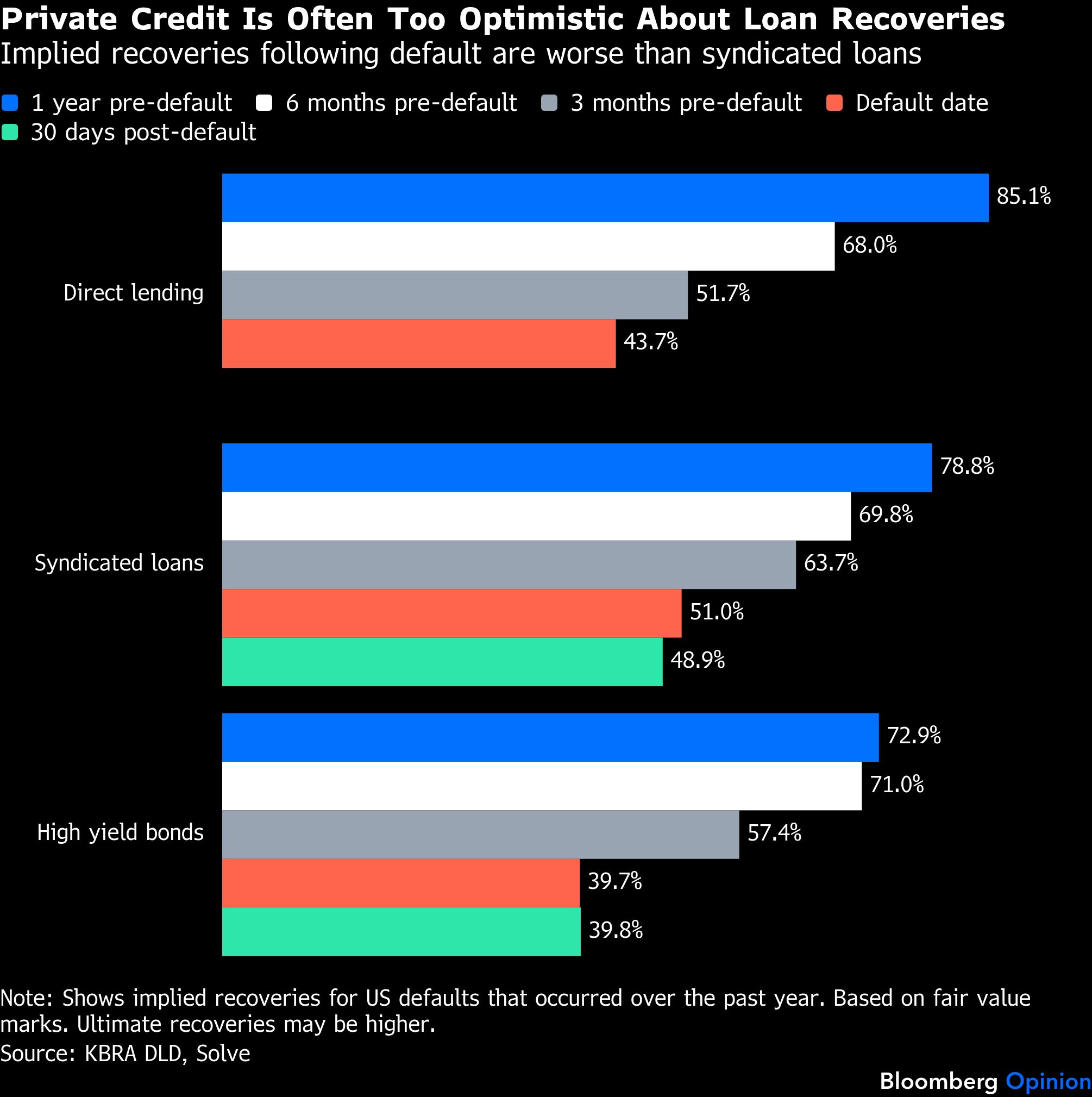

Of course, these AI-related losses will take time to materialize but it’s already looking questionable that private credit — where either one fund or a select group of them lend directly to a company — will conserve more value than broadly syndicated debt arranged by banks. “The thing to worry about in direct lending isn’t the default rates, it’s the implied recovery rates,” Eric Rosenthal, head of default research at industry intelligence provider KBRA DLD, tells me.

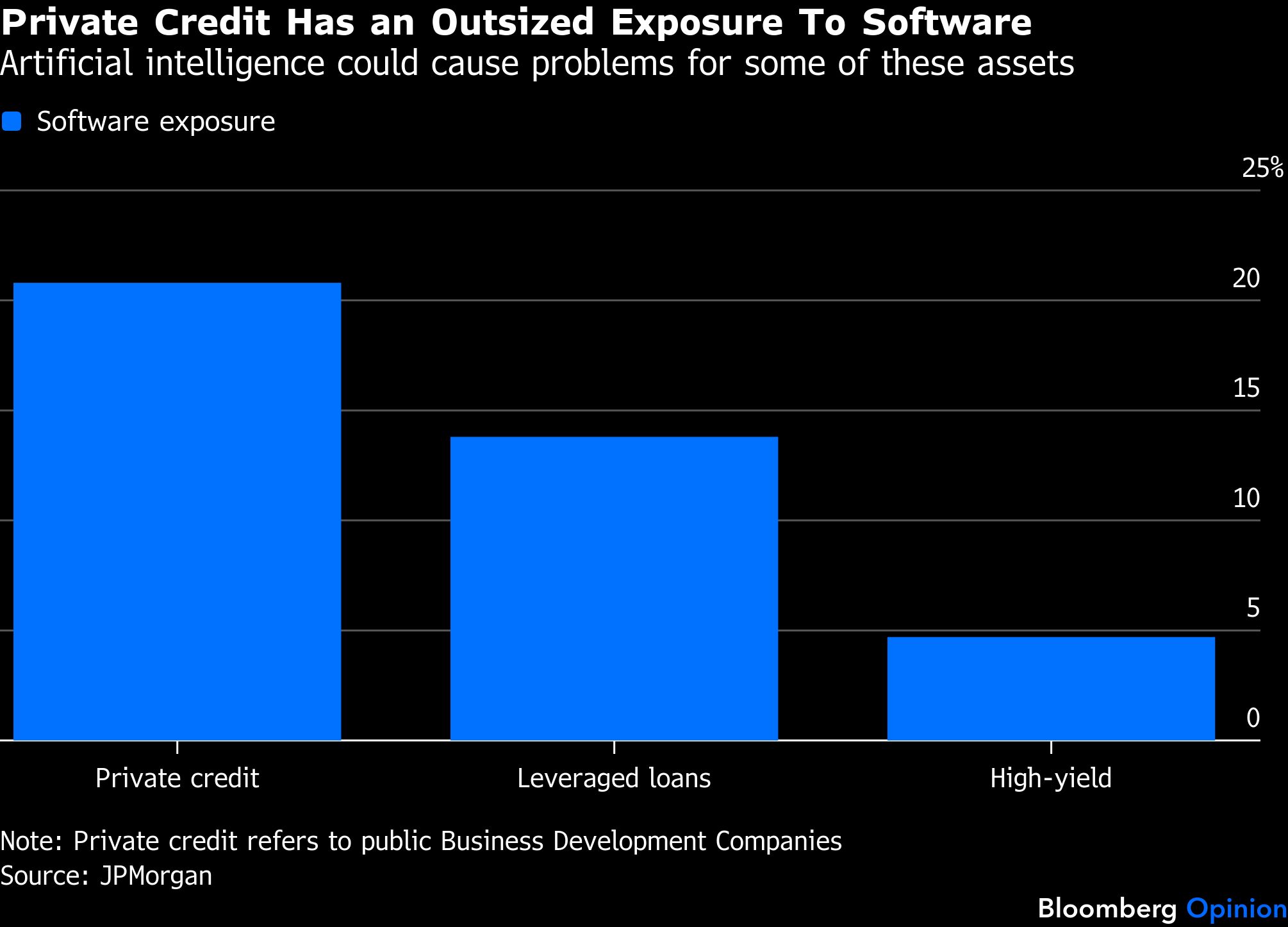

The next big wave of defaults will probably be different in at least two respects to prior periods of credit stress. For one, it will be one of the first big tests for the relatively young private credit industry, which has a hefty exposure to software compared with other creditor types.

Second, the nature of the businesses hitting trouble will doubtless be different. During Covid, firms with physical locations and unsold inventory suffered most (while tech thrived in the work-from-home era). As with the telecoms implosion at the turn of the century and last decade’s shale-oil bust, creditors were at least left with hard assets they could try to sell.

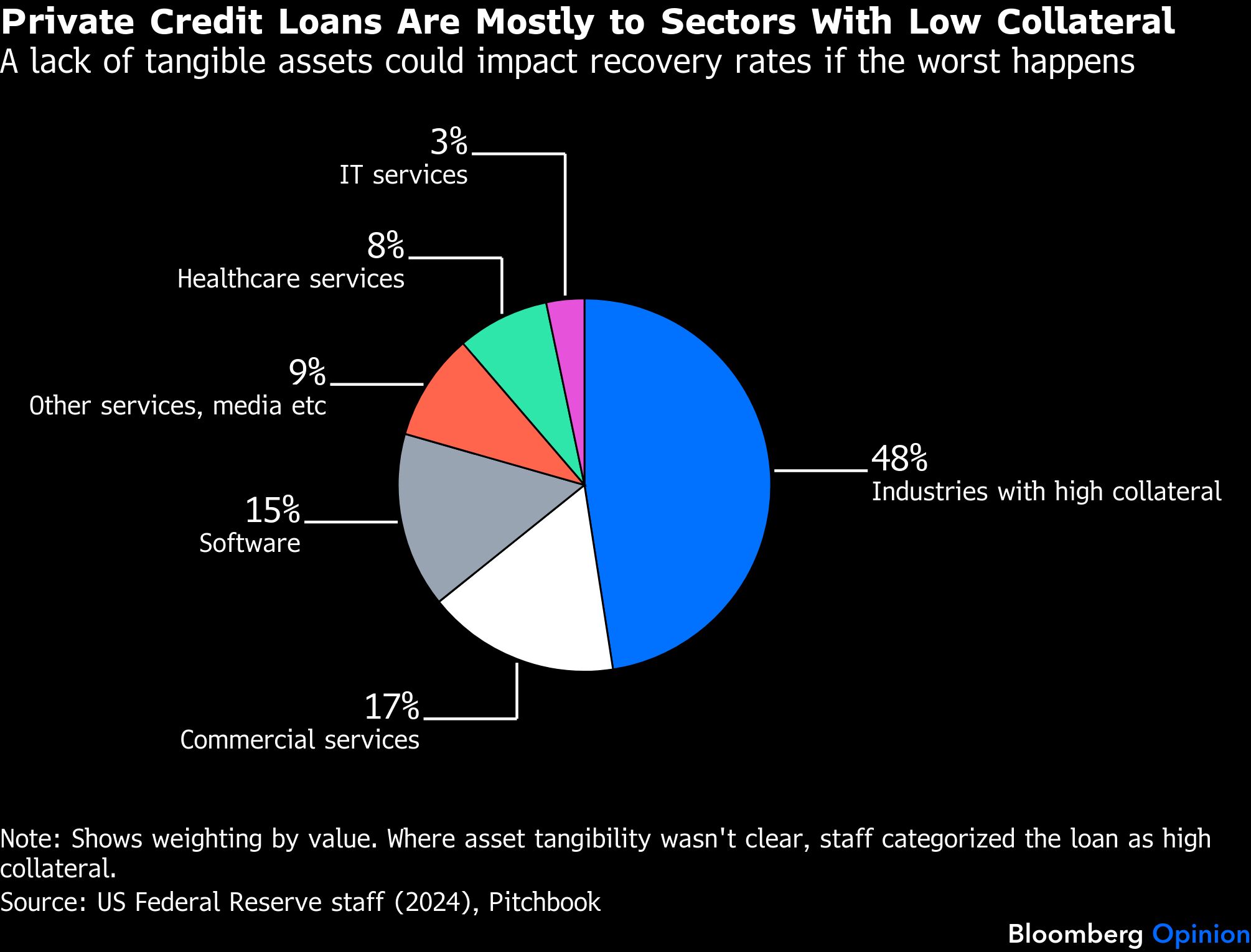

Today, the companies most vulnerable to AI disruption are asset-light. The stuff they own is mostly intangible — things like intellectual property, customer relationships and computer code.

Of course, such assets can be extremely valuable when business is good. America’s most prized companies get much of their worth from intangibles. But this can be tricky to monetize when a company gets into difficulty. Private credit is meant to be relatively safe because it is “senior secured,” meaning it should be paid out first when things go wrong. But when you’ve lent to firms that don’t own physical things, this “provides less downside protection than in asset-intensive sectors,” Allianz Research strategists warn.

Worryingly, more than half of all private credit loans by value are to sectors “with relatively low collateralizable or tangible assets,” according to a 2024 study published by US Federal Reserve staff.

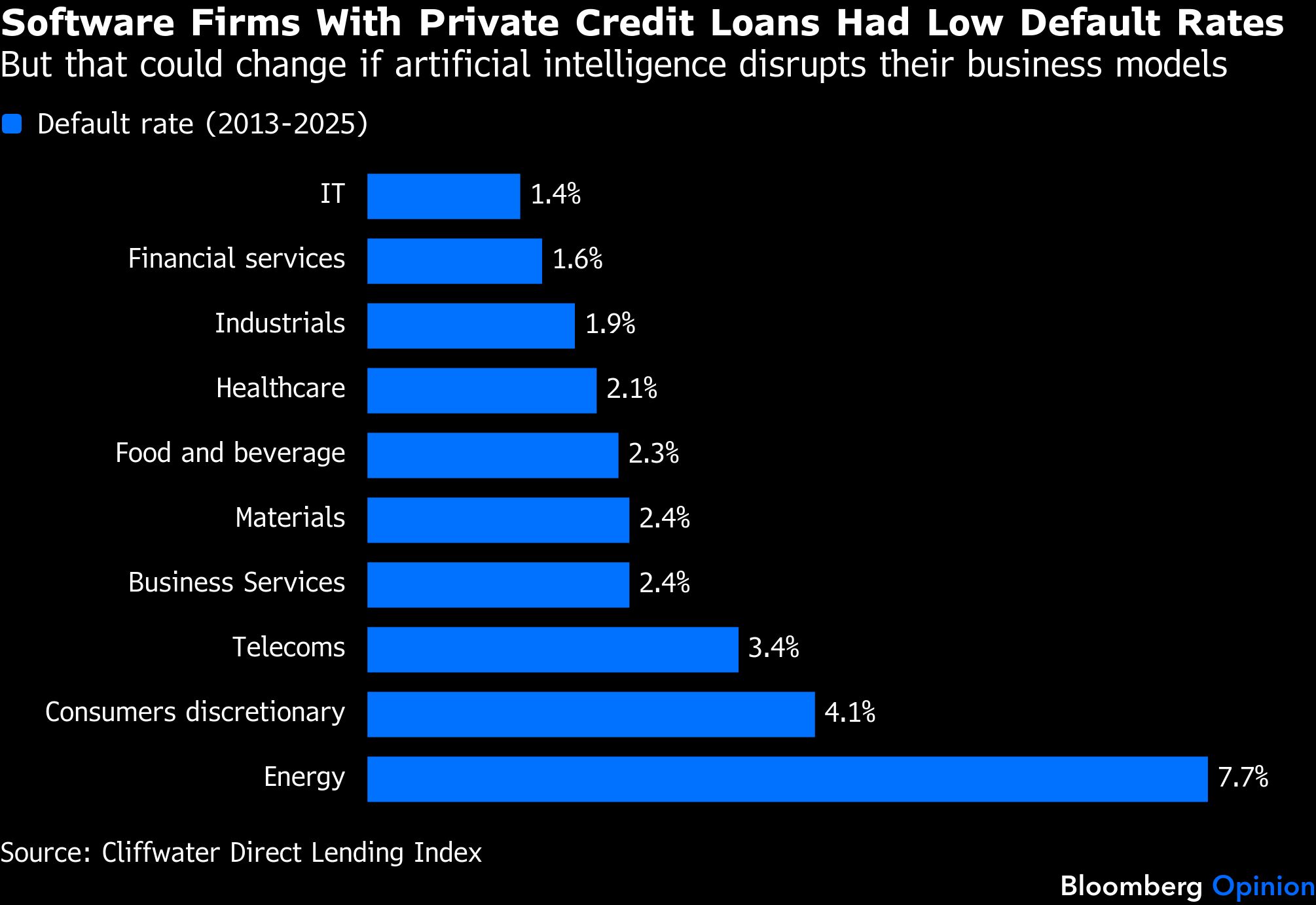

With few hard assets to recover, lenders have a strong motivation to avoid the bankruptcy court and cut borrowers slack to keep a business operating. But if AI causes a software company’s customers to flee, finding an acquirer or refinancing debt might be difficult. Armen Panossian, co-chief executive officer at Oaktree Capital Management, has warned of some potentially binary outcomes in software AI, which could lead to a “pretty rapid degradation of performance” and “quite problematic” recoveries.

“If the underlying case utterly fails in an asset-light business, recoveries can be very poor,” Robert Dodd, an analyst at Raymond James, told clients.

Software companies used to carry little debt, and startups were typically financed with venture capital. This caution was abandoned over the last decade or so as tech-focused private equity firms such as Thoma Bravo and Vista Equity Partners figured software might make attractive leveraged-buyout candidates after all.

The fact that these software-as-a-service firms were asset-light was a key attraction. Once software code is written, attracting more customers doesn’t require a lot of extra investment. And once it is part of a corporate customer’s workflows, these revenues have tended to be sticky.

But as tends to happen in any market boom, software valuations became bloated. Companies without any earnings were loaded with debt. Now values are tumbling amid fears that some companies won’t survive the AI onslaught.

From the lender perspective it’s reassuring that the private equity owners of these companies are first in line to take the hit if things go wrong. As valuations rose, PE buyers were forced to write larger equity checks, which now make up well over half of their average purchase price of US midsized companies. With so much skin in the game, buyout firms have good reason to financially support their struggling companies.

Sorting out problems also tends to be more collaborative when private credit is involved because of the smaller number of lenders. If PE owners do give up and hand the keys to creditors, some direct-lender firms have in-house restructuring teams to assist.

Still, if a private equity sponsor does walk away from a company, the latter’s “business model may be so impaired that lenders can incur significant losses,” warns Lyle Margolis, Fitch Ratings’ head of private credit.

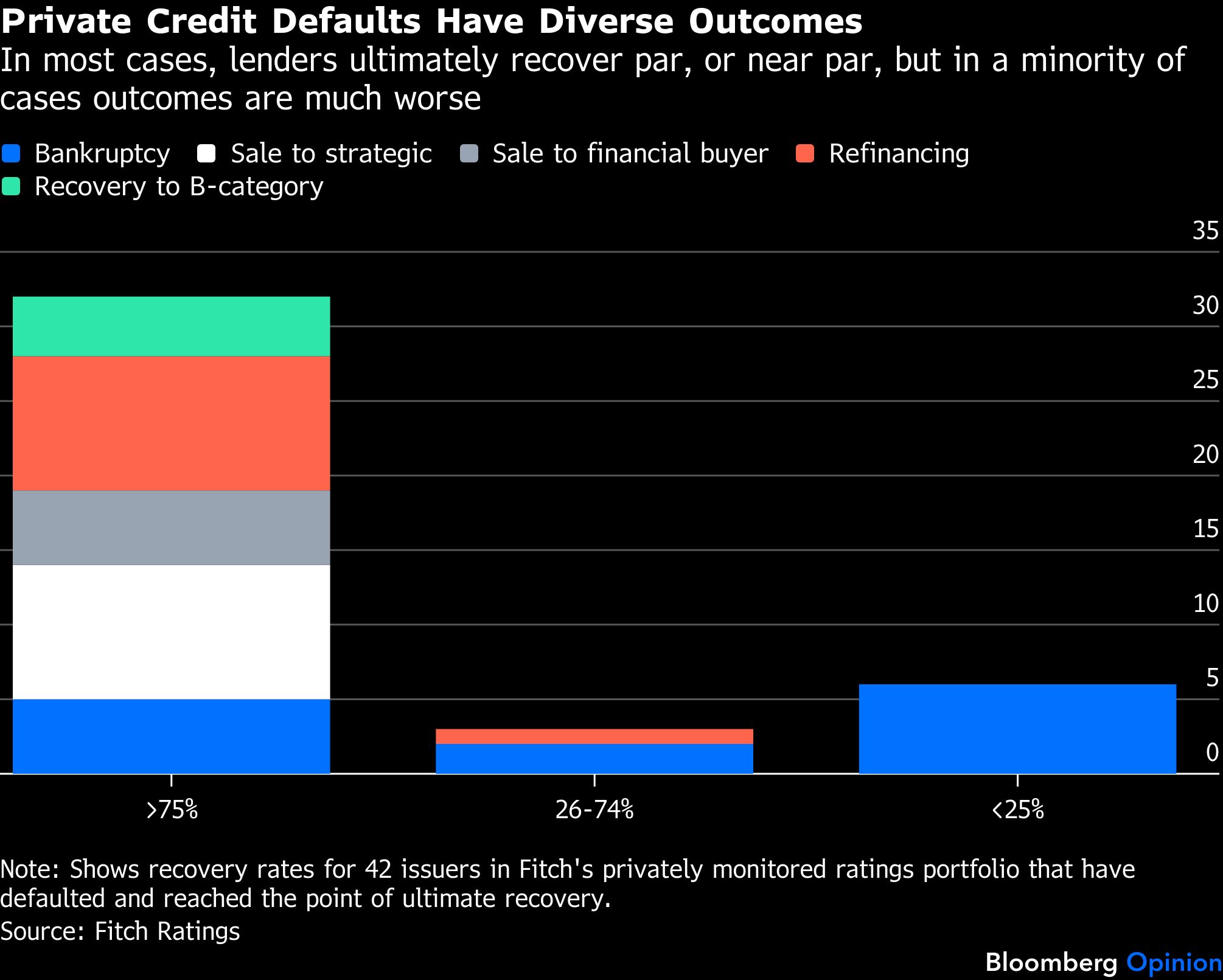

The rating company’s data shows most direct lenders have until now got back more than three-quarters of their money after defaults, but in multiple cases they’ve recovered very little. Lenders to enterprise-software companies will hope to be in the former camp, but the targeting of this market by Anthropic PBC, Amazon.com Inc. and other corporate AI pioneers is sowing doubts.

One of private credit’s selling points was that its simpler debt structures and more patient investors, allied with stronger legal protections on its loans, would ensure better outcomes than its biggest rival in financing private equity buyouts: the syndicated loan market, where investment banks underwrite the debt and parcel it out to a large group of lenders.

Direct lenders were meant to be less prone than their rivals to accepting riskier “covenant-lite” loans, which make it harder to step in when a company starts to struggle. Yet in multiple cases private credit firms’ desperation to win new business has forced them to grant borrowers more leeway, too. They’re also deferring cash interest payments when borrowers can’t afford to make them, often just storing up trouble for later.

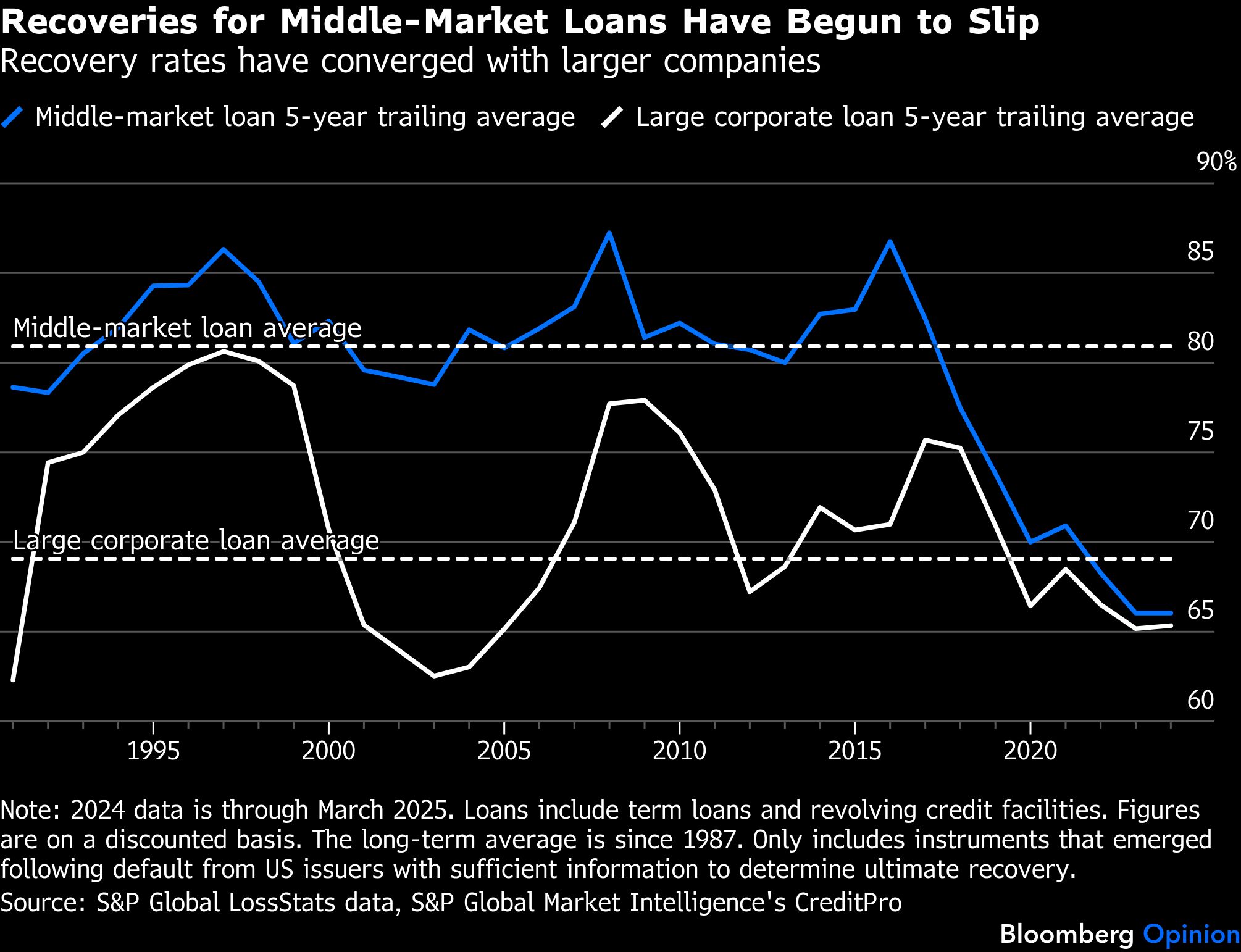

While private credit has historically got more of its money back from companies than broadly syndicated lenders, Citi Research credit strategists reckon “this advantage is eroding.”

Data I got from KBRA shows private credit funds tend to be more optimistic than syndicated lenders about loan recoveries 12 months before a default, yet their implied recoveries at the time of default are worse. The days of midsized credits recovering 80 cents on the dollar are “long gone,” the company says.

If AI does indeed spark a software reckoning, private credit has a problem.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.