Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

How will AI impact the labor market? That question has become a hot topic following the release of “The 2028 Global Intelligence Crisis” by Citrini Research.

While evaluating the impact of AI on the labor market is complex, we can distill both optimistic and pessimistic views into two straightforward ideas:

- Will AI usher in an era of unmatched prosperity and productivity that frees workers from monotonous tasks, revitalizes old industries, and creates unimaginable ones?

- Or will it replace many white-collar workers faster than the economy can absorb them, triggering a deflationary spiral with consequences that rival the Great Depression?

To better understand how AI might affect the labor market and, ultimately, the economy, we’ve summarized Citrini’s bleak outlook alongside rebuttals from Citadel Securities and Bianco Research. These summaries provide a useful primer on how labor markets may adjust to the upcoming major technological changes.

Citrini: A Warning From the Future

Citrini Research’s recent article, "The 2028 Global Intelligence Crisis,” offers a pessimistic outlook. The article is framed as a memo written two years from now, looking back on an economic catastrophe that is already underway; it is not a prediction.

The article begins with a caveat:

What follows is a scenario, not a prediction. This isn’t bear porn or AI doomer fan-fiction. The sole intent of this piece is modeling a scenario that’s been relatively underexplored.

The scenario builds upon something that is already in motion: agentic software. This is software that is cheaper and easier to develop. Citrini suggests a “mid-market SaaS replica” could be built in weeks.

For background, the software as a service (SaaS) industry is based on initial purchase revenue and recurring subscription income. In Citrini’s view, this business model falters in the face of AI, causing wide-ranging effects across the industry.

What makes Citrini’s outlook concerning is not the impact on software companies and their employees, but the negative feedback loop rippling through the economy.

"AI capability improves, payroll shrinks, spending softens, margins tighten, companies buy more capability, capability improves …. A negative feedback loop with no natural brake,” Citrini wrote.

Citrini on the Intelligence Displacement Spiral

Citrini’s pessimistic outlook extends well beyond the SaaS industry. That is merely the opening act. Next is what Citrini calls "the intelligence displacement spiral:” a self-reinforcing loop in which displaced white-collar workers across many industries are pushed into the gig economy, depressing wages and weighing on economic activity.

Bear in mind that wages and employment have a significant impact on consumer spending, which accounts for 70% of GDP. Moreover, the author reminds us that, in their scenario, the new employees — machines — spend $0 on discretionary goods.

It's not just joblessness and a faltering economy. The U.S. government — a once dependable backstop for the economy — will be dealing with falling tax revenue amidst already large fiscal deficits and a significant preexisting debt load.

As is typical, the economic struggles will spread to the financial markets. They foresee a large number of software-related private credit defaults, which weigh heavily on insurance companies that invest heavily in these assets. Also consider the mortgage market, with approximately $13 trillion in U.S. mortgage debt, the repayment of which depends on borrowers maintaining their current income.

"In 2008, the loans were bad on day one," Citrini notes. "In 2028, the loans were good on day one. The world just...changed after the loans were written."

Furthermore, Citrini concludes that, “As investors, we still have time to assess how much of our portfolios are built upon assumptions that won’t survive the decade. As a society, we still have time to be proactive…The canary is still alive.”

A Rebuttal From Citadel Securities

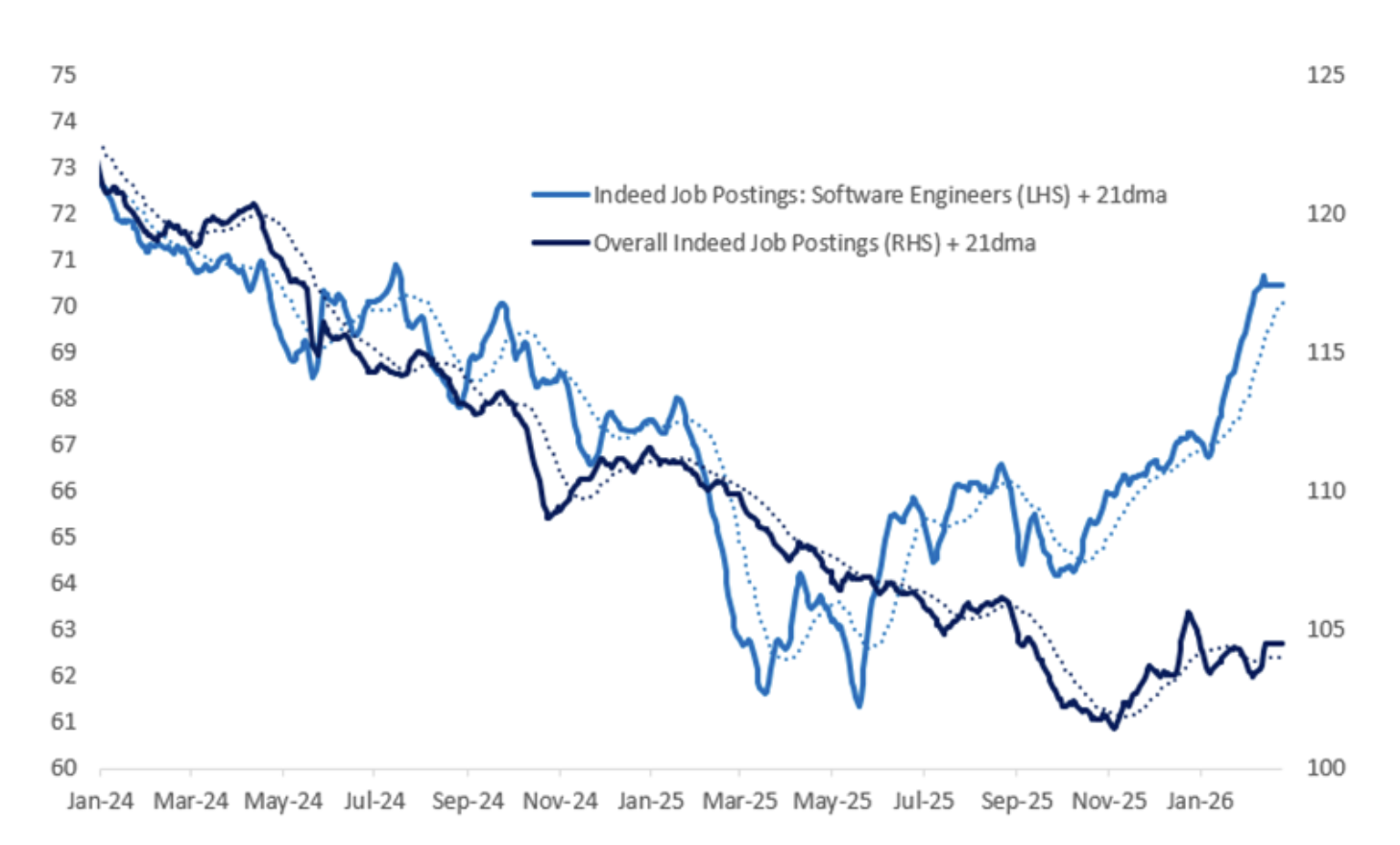

As the title — “The 2026 Global Intelligence Crisis” — suggests, Citadel’s rebuttal was clearly motivated by their disagreement with Citrini. It starts by directly challenging Citrini’s pessimistic assessment of today’s software job market. The graph below shows that job postings for software engineers are rising, up 11% year-over-year. Furthermore, Citadel states that St. Louis Fed data on AI adoption at work “presents little evidence of any imminent displacement risk."

Citadel’s core argument is that Citrini is wrong about AI's recursive potential, specifically the speed and breadth of its spread throughout the economy.

“‘Technological diffusion,’ or the rate at which a new technology spreads through the economy, has historically followed an ‘S-curve,’” Citadel wrote.

Essentially, Citadel argues that even if Citrini is right about where AI is eventually headed, the pace of getting there is likely far slower than Citrini assumes — and that slower pace gives the labor market, businesses, and governments time to adapt.

Citadel also directly challenges Citrini’s macroeconomic logic. It claims that, “AI-driven automation is a productivity shock. Productivity shocks are positive supply shocks: they lower marginal costs, expand potential output, and increase real income. They are in isolation disinflationary and growth-enhancing in the medium term.”

Citadel supports the opinion by noting how steam power, electrification, the internal combustion engine, and, more recently, computing, have followed the S-curve pattern. Furthermore, it argues that lower prices due to productivity growth increase consumption.

Citadel reaffirms the argument with the national income accounting identity.

The national income identity states that all spending in the economy (Y) comes from four categories: consumption ©, investment (I), government spending (G), and net exports (X-M, exports minus imports)

Or:

Y = C + I + G + (X − M)

Because this is an identity, it always holds true. Citadel states:

If output rises and real GDP increases then by national income accounting identity something must be rising on the demand side: Consumption, investment, government spending, or net exports must be increasing (more here). A scenario in which productivity surges but aggregate demand collapses while measured output rises violates accounting identities.

More simply, everything produced is ultimately purchased by someone. Consumers © buy it, businesses (I) invest in it, the government (G) spends on it, or foreign buyers (X-M) import it. Those are the only four options. If total economic output (Y) is rising — which Citrini's scenario assumes, since AI is driving a productivity boom — then by definition someone must be doing more buying. You cannot have an economy producing more and selling less at the same time. The basic math and capitalist motives do not allow for it.

Historically, technological revolutions have altered task composition rather than eliminated labor as an input. To produce a negative demand shock large enough to overwhelm output expansion, one must assume near-total automation of economically relevant labor combined with extremely weak redistributive responses. To frame this debate correctly, one can simply ask if the advent of Microsoft office was a complement or substitute for office workers. Previously, the concern skewed towards substitution; now, it appears a clear complement.

Citadel brings up an important historical note. In 1930, John Maynard Keynes, in “Economic Possibilities for our Grandchildren,” predicted that rising productivity would reduce the workweek to fifteen hours by the early twenty-first century. He was right about productivity growth but dead wrong about the labor market implications.

It ends by reminding us, “It is also worth recalling that over the past century, successive waves of technological change have not produced runaway exponential growth, nor have they rendered labor obsolete. Instead, they have been just sufficient to keep long-term trend growth in advanced economies near 2%. Today’s secular forces of ageing populations, climate change and deglobalization exert downward pressure on potential growth and productivity, perhaps AI is just enough to offset these headwinds.”

Jim Bianco’s Perspective

Jim Bianco’s piece “An Alternate View Of The Post-AI Labor Market,” like Citadel's, is a more optimistic take than Citrini's article. Bianco approaches the rebuttal from a different angle than Citadel — the nature of business itself.

Bianco writes, "At its core, every business exists to solve a human problem," calling Citrini's fatal flaw "the assumption that humanity has a finite number of problems."

Bianco’s argument leans on Jevons Paradox: When technology makes something more efficient, demand for that thing tends to explode, rather than contract. If AI reduces the cost of drafting a lawsuit to near zero, lawyers do not go home; instead, they file more lawsuits, creating new demand for legal defense and judges.

Bianco also makes a useful distinction between automating parts of a job. He uses GPS as an example. He writes:

When a job is disrupted, the outcome depends entirely on which part is automated. For 150 years, the hard part of driving a London taxi was passing the knowledge test. This involved memorizing 25,000 streets and nearly 20,000 landmarks. This took three or four years, often riding around London on a moped. This knowledge created a scarcity of qualified drivers, allowing them to command a premium wage. GPS automated this scarcity into a free app, flooding the market with new competitors (Uber/Bolt), which flattened wages. Technology took away the hard part of being a taxi driver, making the role less valuable.

Bianco’s “flipside” of less valuable London cab drivers is the story of accountants. Computers eliminated the easy part of accounting, which in turn allowed accountants to provide “more valuable” financial advisory services along with accounting services.

The outcome on the labor market depends on whether AI automates the scarce, high-judgment part of a role or the repetitive overhead.

Bianco believes AI removes the easy, repetitive parts of knowledge work, making workers more valuable. This counters Citrini, which claims it does not matter which part gets automated — if it happens fast enough and at a large enough scale, the labor market cannot absorb the displacement, regardless of whether the remaining work is more interesting.

Bianco closes with what he considers the most critical variable — the speed of transition. He introduces us to a historical parallel: the Engels’ Pause of the Industrial Revolution.

The Engels’ Pause: Where Everyone Agrees

The Engels’ Pause, named after Friedrich Engels, who co-authored “The Communist Manifesto,” describes a harsh fifty-year period from 1790 to 1840. During the Industrial Revolution, this interval was marked by significant job losses that were not immediately offset by new employment. According to Bianco:

That gap between job destruction and job creation sparked a massive collective pushback against capitalism that the world came to know as Communism. Karl Marx directly observed this dangerous dynamic, writing that when an instrument of labor takes the form of a machine, it immediately becomes a competitor of the worker himself.

Citrini's scenario is, at its core, a modern Engels’ Pause playing out again, but much more quickly. Therefore, its immediate impact could be greater. Bianco and Citadel do not deny the transition risk; however, they seem to argue that the gap can be managed if the pace of adoption is measured and institutional responses are timely.

The three articles implicitly agree that if job destruction outpaces job creation for long enough, the political and social consequences could be severe, despite improvements in productivity and corporate profits.

Summary

Technological revolutions have consistently created more jobs than they destroyed. While that statement is 100% true, we must caveat it by describing the transition with the word “eventually.” If the AI transition is unbalanced, the negative economic, social, and political ramifications become more worrisome.

From our perspective, the Citrini scenario is a tail risk and not a base case. That said, we certainly don’t turn a blind eye to its opinion.

To assess the ongoing labor market transition, we will closely monitor economic indicators, including white-collar job openings, real wage growth in knowledge industries, and consumer spending patterns among higher-income households. If those metrics deteriorate simultaneously, the feedback loops Citrini describes could be a force to reckon with.

The canary, Citrini notes, is still alive, but we need to watch it closely.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Michael Lebowitz

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.