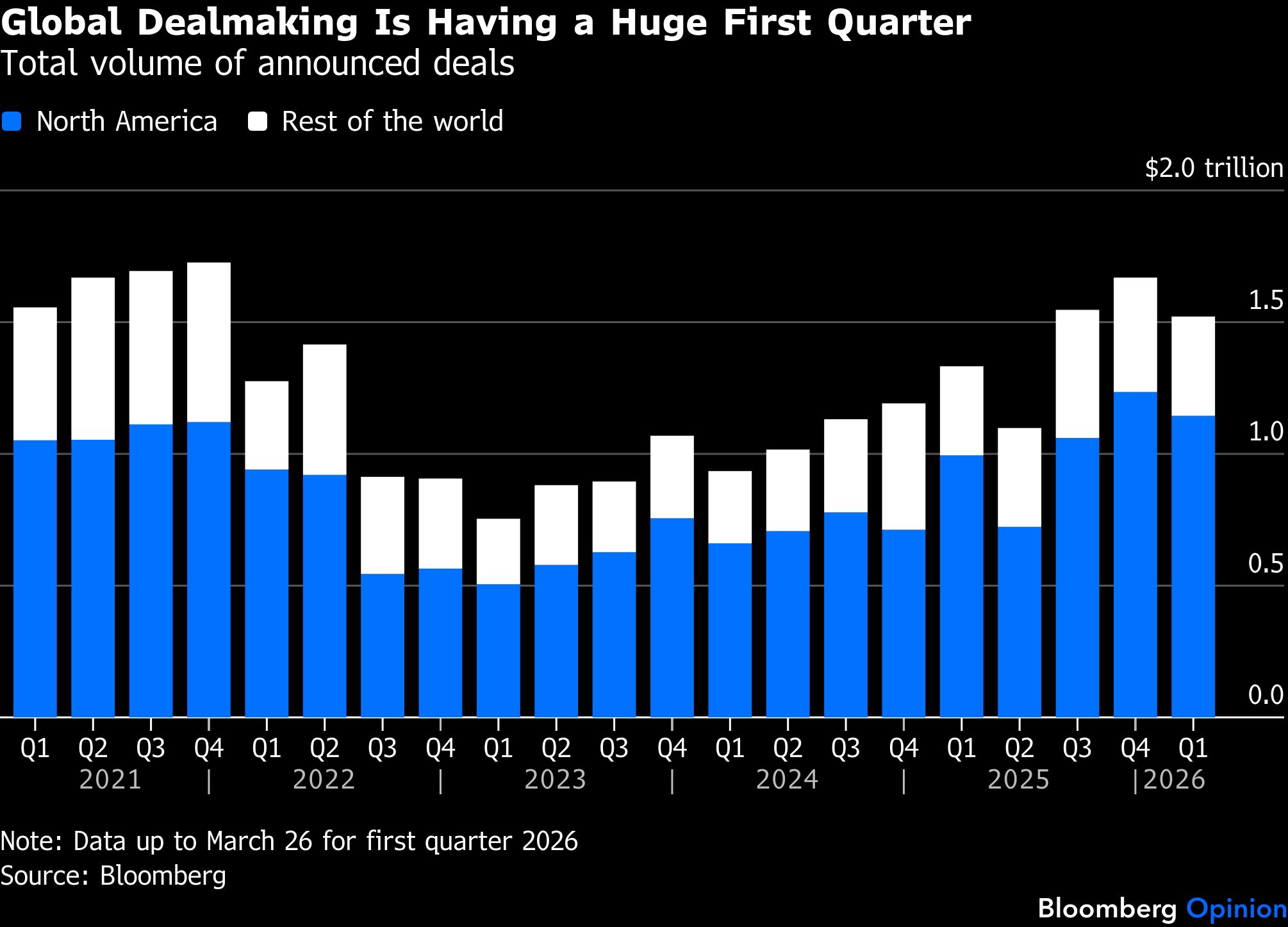

Financial markets have been relatively unaffected by the costly and senseless war the US and Israel are waging against Iran. But what’s really surprising is the ongoing boom in investment banking. Dealmaking and fundraising activities that are usually most sensitive to worsening sentiment and increased volatility are about to close a strong first quarter — but there are plenty of warning signs that things could come to a grinding halt.

Persistently high energy prices, if the White House fails to find a quick route out of the Middle East, would weigh on many economies already facing slowing growth and softening labor markets. That would add to concerns about rising defaults in private credit and the disruptive threat of artificial intelligence, which have been causing wild swings in the fortunes of some companies and fund managers.

And yet takeovers, mergers, new stock listings and debt sales for private equity deals have all posted extremely healthy first-quarter numbers, according to data compiled by Bloomberg. Bankers and their clients are acting quickly to get deals done while they can: They learned last year that an impulsive and unpredictable President Donald Trump is capable of deflating animal spirits in a flash.

Jefferies Financial Group Inc. last week reported record fees from dealmaking and trading in the quarter ended Feb. 28, with its executives talking up the robust activity they anticipate for the rest of the year, assuming a relatively quick and clear end to the fighting in the Middle East. But in a sign of the troubles brewing beneath the surface, the firm missed earnings forecasts because of losses on lending to nonbank finance firms, such as First Brands Group LLC.

Just like last year, bankers were expecting a strong start to 2026. Pent-up demand from executives to do deals and high-flying stock markets helped make last year the second-biggest for M&A volumes in history. For bankers and traders, these buoyant conditions delivered the highest bonus pool in Wall Street history at nearly $50 billion, according to data from the New York State Comptroller. And that was despite the farce of last April’s so-called Liberation Day, when Trump slapped punitive trade tariffs on every nation and rocky island in the world only to walk them back almost entirely several days later.

This year got off to a strong start in the face of growing concern about the impact that rapidly improving AI would have on many businesses, especially software makers, and still wasn’t derailed when Trump joined Israel in bombing Iran at the end of February. There have been some wobbles, but most deals and fundraisings that were underway have got done.