Hedge fund activist Boaz Weinstein is on the cusp of his most significant campaign victory yet — overhauling an investment trust whose claim to fame is an early bet on Elon Musk’s SpaceX rocket company. But the beleaguered target is doing a good job of trashing the prize pot.

Weinstein’s Saba Capital Management is likely to replace the board of Edinburgh Worldwide Investment Trust Plc at a shareholder meeting in April. The London-listed trust owns a $1 billion portfolio of stakes in perceived high-growth companies, around 17% of which is SpaceX stock.

Saba’s last attempted coup narrowly failed to get the required shareholder votes. Edinburgh expects a lower turnout next time will give Weinstein’s 30% stake decisive sway.

What would happen next is uncertain as Weinstein’s board nominees haven’t outlined a plan. The activist says they’re independent of his firm. But Saba will clearly have influence. This week it called for shareholders to be given the option of a cash exit, whether immediately or after SpaceX’s expected upcoming initial public offering. The activist also said it would seek the contract to run the Edinburgh trust’s money if a new board jettisoned the incumbent fund manager Baillie Gifford.

Finally, Saba confirmed it wants to change the trust’s strategy to focus on buying stakes in other undervalued investment trusts. That’s potentially lucrative — if less glamorous than scouring Silicon Valley for the next SpaceX.

The investment-trust community is outraged by Saba’s assault. But the status quo is hard to defend. Once SpaceX goes public, Edinburgh’s raison d’être falls away like a gantry in a rocket launch. If investors can buy SpaceX in the market, the case for the trust rests on a wider investment record that is nothing to be proud of.

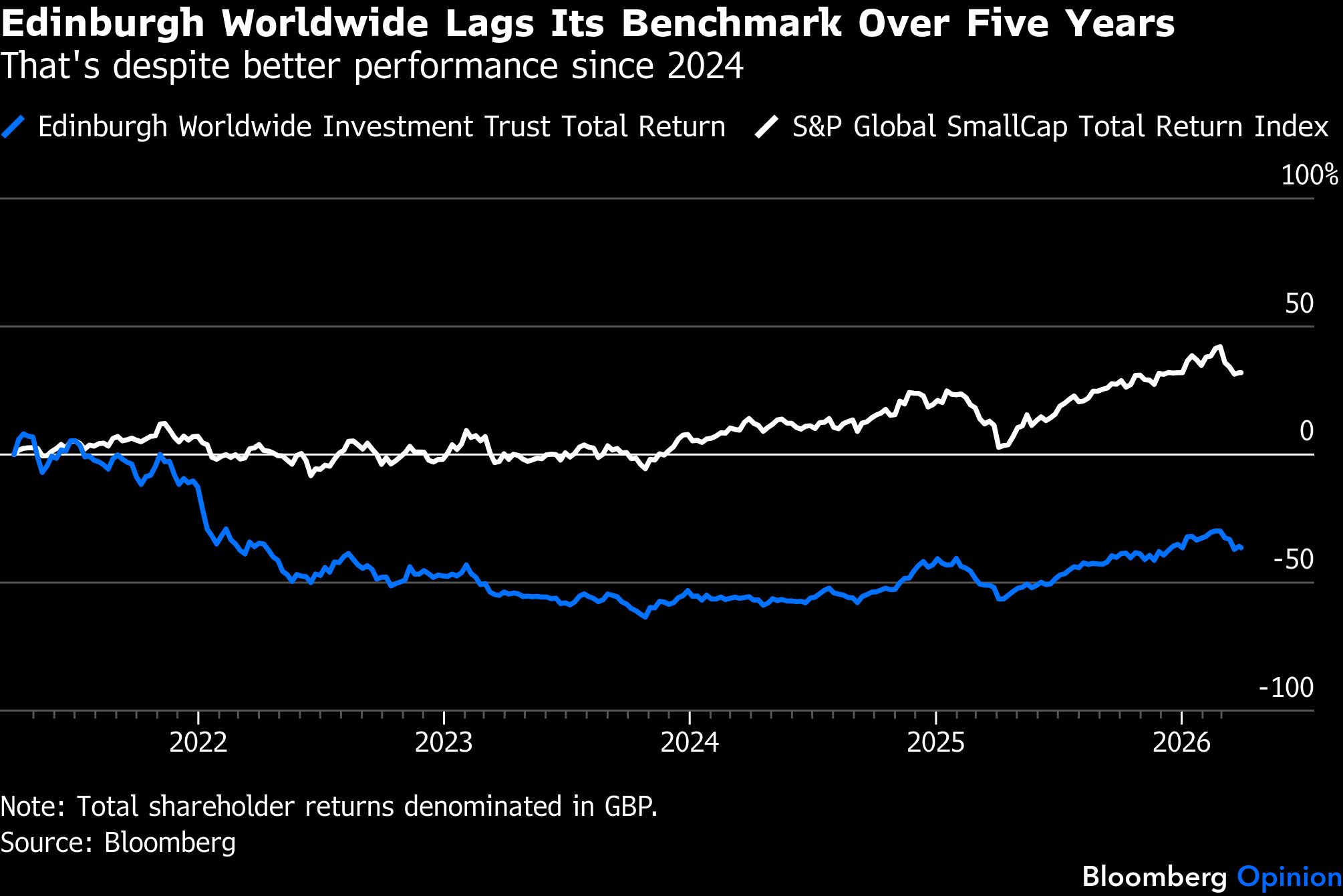

Its five-year history is dire. Things have improved somewhat since a new chair arrived in 2024 and secured changes to Baillie Gifford’s fund-management team and approach. But a pickup in the share price is partly thanks to Saba’s stake-building. The recent record is also tarnished by a decision to trim the SpaceX stake months before Musk’s firm was valued at $800 billion and subsequently linked to a possible $1.5 trillion IPO valuation. The idea was to create headroom for other investments. Those prospects had better be hot.

Despite this charge sheet, almost all of Edinburgh’s non-Saba shareholders are furious with Weinstein and not their own board. Putting up with bad service is a British stereotype, after all. As is disdain for noisy Americans. Whatever the explanation, Saba’s large stake is the likely decider: Committed capital is a hedge fund activist’s killer app when persuasion fails.

Mindful of the uncertainty arising from a Saba victory, Edinburgh’s board has made a guaranteed counteroffer to investors. It’s promising them a cash exit to be funded by selling down its listed portfolio immediately and their pro-rata stake in SpaceX probably around the time of the mooted IPO.

This looks attractive. The snag is that it could trigger a capital-gains tax liability for some shareholders, depending on when and how they invested. Worse, the plan could make life grim for those investors who stay on board.

Suppose a lot of non-Saba shareholders did cash out this way. The leftover portfolio would largely comprise illiquid investments, which probably means the stock would trade at a big discount to the underlying value of its holdings. Meanwhile, Saba’s percentage stake would arithmetically increase. That more concentrated share register could jeopardize Edinburgh’s trust-related tax privileges, forcing Saba to sell down. Again, bad for the stock price.

Just because the board’s escape plan is available to all shareholders in equal measure, that doesn’t mean it treats stayers and leavers equally.

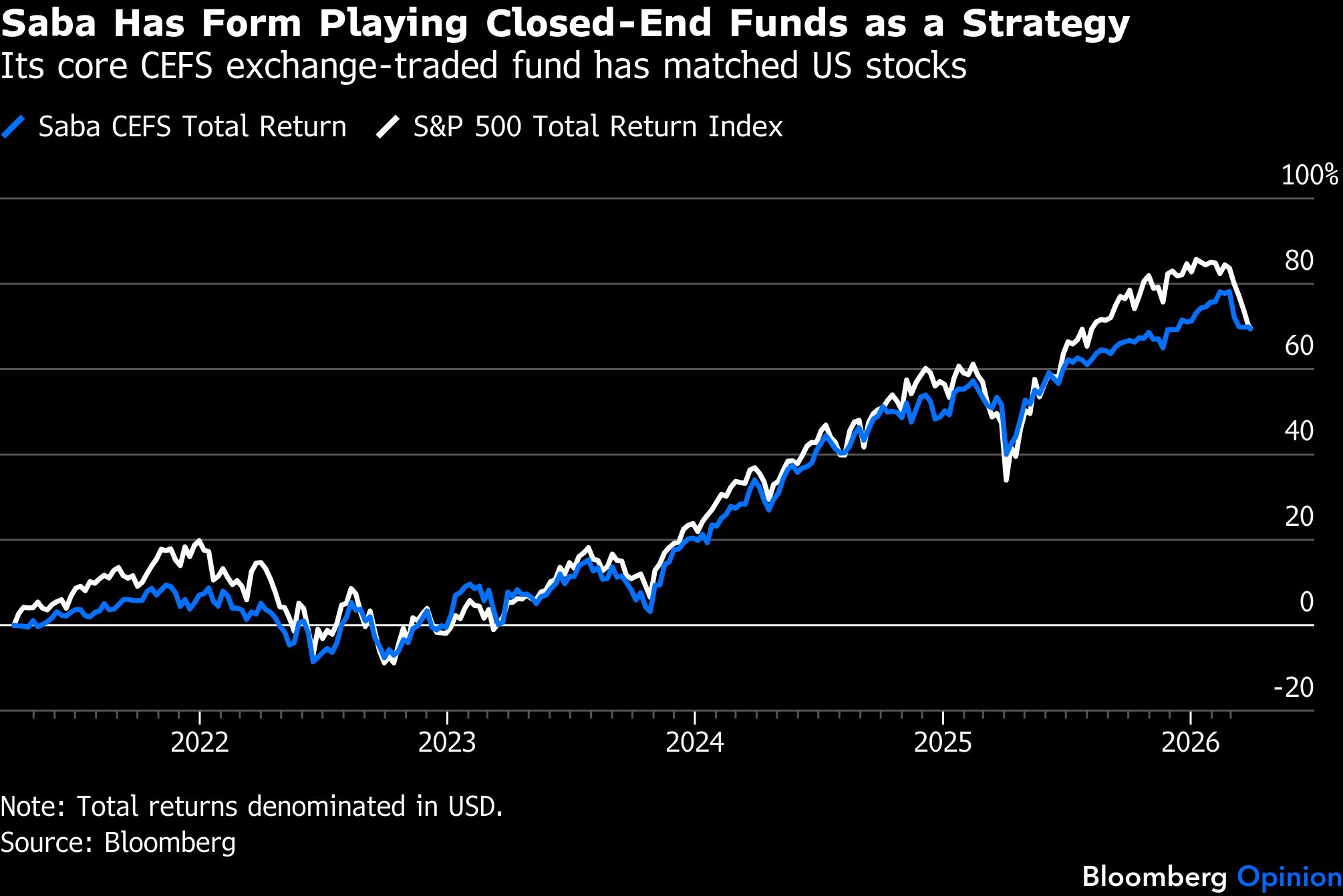

The prospect of Saba becoming the trust’s investment manager should, of course, put the spotlight on its own track record. The activist’s existing US-listed investment-trust vehicle, CEFS, has roughly matched the soaraway S&P 500 over five years and vastly outperformed Edinburgh in terms of total returns.

Saba also has two investment trusts running more esoteric strategies, investing in public and private credit, derivatives, reinsurance and other less mainstream assets. These trade at notable discounts to the underlying portfolio value, attracting activist interest of their own in the form of Gamco Investors Inc., an asset manager led by value investor Mario Gabelli. While these funds’ strategies aren’t comparable to what Saba envisages for Edinburgh, Weinstein needs to address their discounts.

The UK Financial Conduct Authority is rightly resisting calls to make life harder for corporate and financial interlopers like Weinstein. One-share, one-vote is a solid principle of good governance. Saba has built its many activist positions precisely because shareholders in its targets have wanted to sell, and they got a better price thanks to Weinstein pumping up demand.

If shareholders’ apathy plays to an activist’s advantage, the remedy is better communication. And if investment trusts don’t want predatory hedge funds trying to worm their way into the asset-management contract, they should take steps to avoid trading at a discount in the first place.

Investors in the vehicles under attack may rue Weinstein’s intervention. They should ask themselves if their shares would be where they are now if such activists didn’t exist.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit bloomberg.com.