Unilever Plc’s Fernando Fernandez has lucked out by selling the company’s food businesses, including Hellmann’s mayonnaise and Knorr stock cubes, to McCormick & Co. But Fernandez, who’s been chief executive officer for just over a year, shouldn’t squander his good fortune; he needs a clear vision for what comes next.

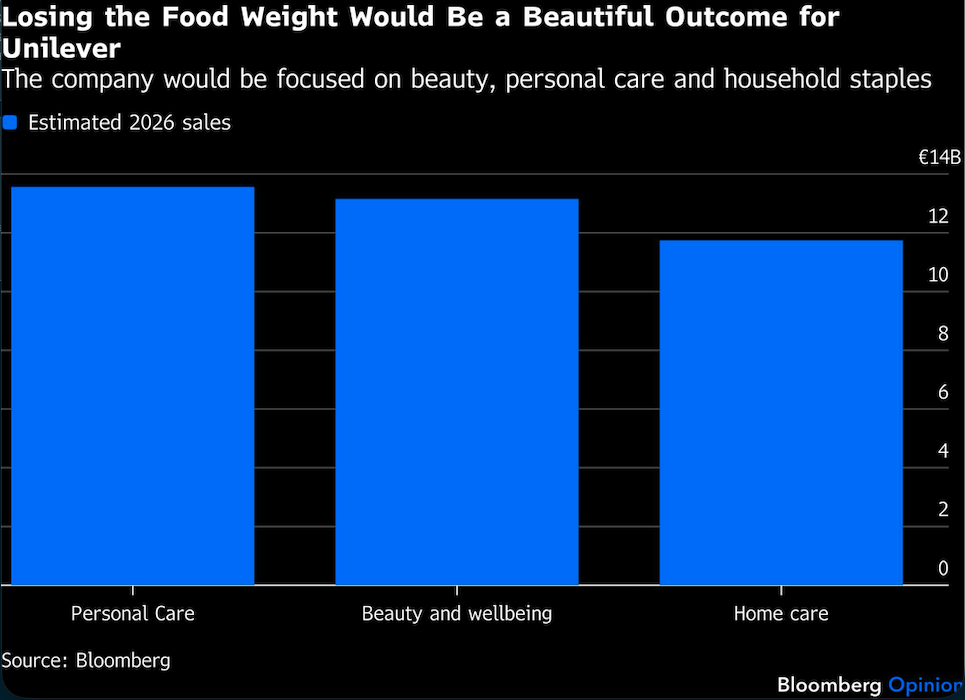

After spinning off ice cream in December, combining most of the food division with McCormick in a $44.8 billion deal leaves the consumer giant with about €38 billion ($44 billion) of sales generated by its beauty and wellbeing, personal care and homecare divisions, according to data compiled by Bloomberg.

What’s effectively a breakup of Unilever is part of a broader reshaping of the global consumer goods sector, as the industry grapples with cash-strapped shoppers becoming more thrifty and the impact of GLP-1 weight-loss drugs on eating habits. Manufacturers are seeking to shed tired brands and focus on businesses capable of generating superior sales growth — and valuations.

Against this backdrop, Fernandez could choose to do more slicing, separating names such as Cif cleaner, Comfort fabric softener and Domestos bleach from beauty and personal care products such as Dermalogica skincare and Liquid IV hydration powder. Household products, which would contribute about 30% of sales once the food units are shed, are not as disconnected from cosmetics and body washes as comestibles are, but they’re still more sluggish categories.

There’s a snag, though. These brands are crucial to Unilever’s emerging markets business, where Fernandez spent much of his career. It’s notable that Unilever’s food business in India is excluded from the McCormick agreement. Consequently, the CEO may be reluctant to let the household staples go, and could instead look to bulk up the new Unilever.

He said in December that he was allocating €1.5 billion a year to M&A, taking Unilever further into upmarket beauty and personal care and focusing on the US and India. He added that transformative acquisitions were “off the table.” But with Unilever set to receive $15.7 billion in cash upfront from McCormick — the rest of the transaction will be in shares — he may change his mind. One benefit of a more substantial purchase is that it could help Unilever address a cost base — post the food sale — that’s too big compared with its revenue.

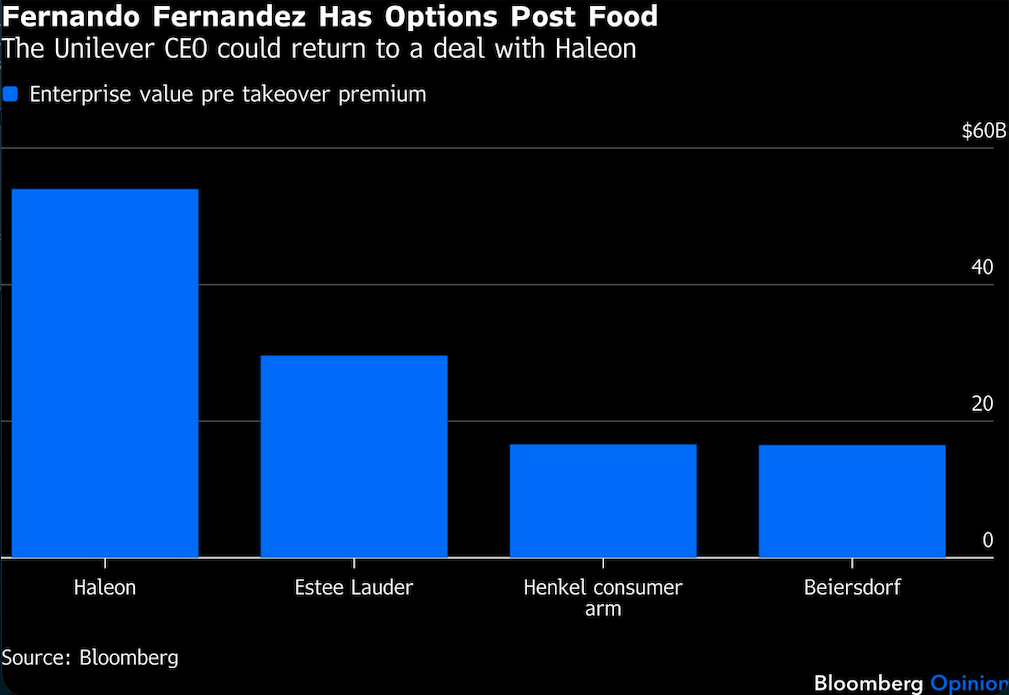

In early 2022, Fernandez’s predecessor before one, Alan Jope, wanted to acquire GSK Plc’s consumer health arm, which listed six months later as Haleon Plc. The logic of adding Haleon’s Panadol painkillers and Sensodyne toothpaste to Unilever’s portfolio, including Dove and Vaseline, and pumping them through the Unilever distribution and marketing machines, particularly in developing markets, was never in doubt.

But Jope failed to get shareholders onside for a £50 billion ($66 billion) deal after a lackluster performance and his mantra that brands should have purpose, which drew criticism from some investors. Haleon has been underwhelming since its listing, with weaker than expected growth.

Assuming a standard 30% takeover premium, the price for buying Haleon today would be around the £50 billion Unilever offered last time. But Unilever could use a mix of cash from the food sale and its own shares to make the transaction more affordable. And, unlike Jope, Fernandez seems to have credibility with investors.

Alternatively, Fernandez could turn his attention to Estee Lauder Cos. Adding the beauty giant would tick the boxes of exposure to the US and premiumization, with the stable of brands led by Tom Ford but also including Clinique, Le Labo and Deciem. What’s more, Estee Lauder shares have fallen more than 20% since news of talks to buy Puig Brands AG emerged last week.

The beauty company is smaller than Haleon. Assuming a 30% takeover premium the enterprise value would be about $37 billion. However, a deal would require the blessing of the Lauder family, which still holds about 80% of the voting rights. Estee Lauder buying Puig has significant risks. One of the factors that could make it work is that Puig is also family run, so the two controlling shareholders understand each other.

If Haleon or Estee Lauder look too chunky, then smaller bites may include Beiersdorf AG or the consumer arm of Henkel AG. Beiersdorf, with an enterprise value of about €14.5 billion before any takeover premium, owns Nivea, as well as upmarket skincare line La Prairie. A drawback is that it is majority-owned by the Maxingvest AG holding company, which has never shown any intention of selling.

Henkel’s portfolio includes the Schwarzkopf haircare brand as well as US teen favorite Not Your Mother’s. (Underlining the many moving parts currently at work in consumer goods, Henkel has itself agreed to buy Olaplex Holdings Inc., best known for its hair-strengthening treatments, for $1.4 billion.) While haircare would fit in Unilever’s portfolio — it bought brand of the moment K18 two years ago, and Fernandez said in December that it remains a priority area — I’m not convinced Unilever would want the rest of Henkel’s consumer arm, including Jeyes cleaning fluids and Dylon dyes. Assuming a multiple of 8-10 times earnings before interest, tax, depreciation and amortization, the consumer division could have an enterprise value of as much as €16 billion. So far, though, Henkel has been reluctant to split the consumer arm from its adhesives business.

None of these potential deals are perfect, and of course Fernandez needs a willing seller too. But the McCormick transaction won’t be completed for another year. Amid the shifting sands of global consumer goods, he should be considering his next move. As Unilever, the owner of chichi beauty brand Hourglass Cosmetics knows, any good glow up starts with a flawless foundation.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.