Beta: A Powerful But Faulty Tool for Managing Risk

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

When investors want to reduce risk, one commonly used tool is beta. For instance, an investor may sell higher-beta stocks and replace them with lower-beta ones to cushion against an expected market decline. Such a strategy is intuitive and widely used; however, it can be greatly flawed.

We recently received a question from a client about how we use beta to manage our portfolios. Given recent volatility and declining prices, the timing could not be better to explore both the power of beta and its important constraints.

What Is Beta?

In simplistic terms, beta answers one question: When the market moves, how much does a stock tend to move with it?

A stock with a beta of 0.50 should move roughly half as much as the market in either direction. A stock with a beta of 2.0 should move roughly twice as much. In statistics, beta is the slope of the best-fit line through a scatter plot comparing a stock's weekly returns to the market's returns. The steeper the line, the higher the beta, and vice versa.

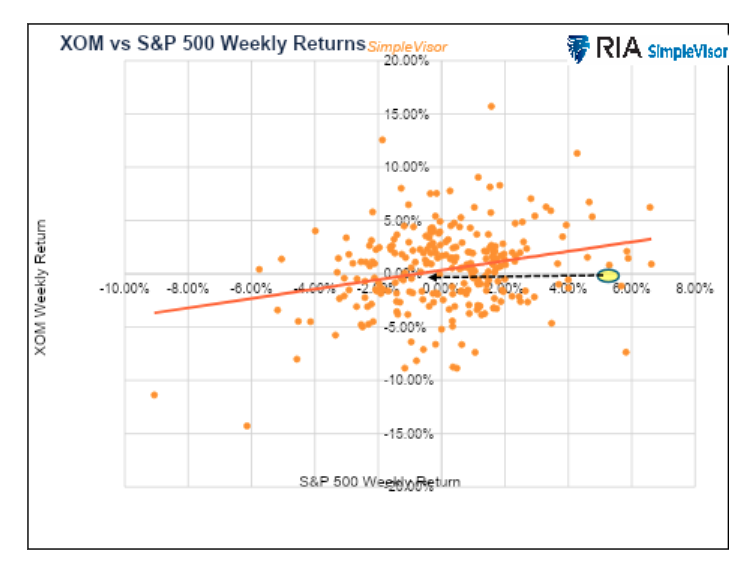

To clarify, consider the graph below. Each dot on the scatter chart shows the intersection of the weekly returns of Exxon (XOM) and the S&P 500 over the last five years. The beta – or the slope – of XOM quantifies the angle of the best-fit line (orange). XOM has a beta of 0.43. Thus, for every 1.00% increase or decrease in the S&P 500, XOM – represented by the orange line – will rise or fall by 0.43%. The yellow circle shows that an approximate 5.00% increase in the S&P 500 equates to an expected increase in XOM of 2.15% (0.43% multiplied by 5%).

If investors fear a market drawdown, they might want to replace higher-beta stocks with lower-beta ones like XOM. Conversely, they might do the opposite if they think the market will move higher. If only portfolio management were that easy!

Correlation Matters: Analyzing XOM

Let's stick with the XOM analysis to demonstrate how misleading beta can be. As noted above, the beta of XOM over the last five years is 0.43. But that figure doesn’t address how much we should trust it.

To quantify our confidence, we calculate the relationship’s R-squared, which measures how closely the dots cluster around the trend line on a scale of zero to one. A reading near one means beta is highly reliable. A reading near zero means the relationship between the stock and the market is essentially random. The R-squared for the XOM graph we showed above is statistically insignificant at 0.0645, indicating a weak correlation between XOM and the market.

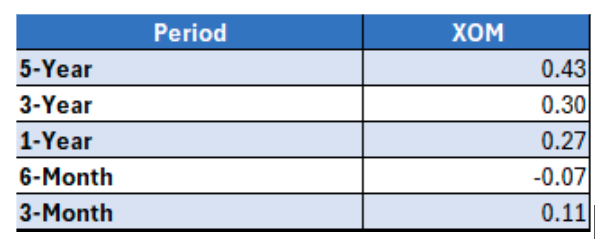

Beyond the R-squared, it’s also important to understand that beta is not static. It changes with new data and with changes to the time frame used to calculate beta. As shown in the table below, XOM’s five-year beta differs markedly from the most recent three- and six-month betas.

Correlation Matters: Nvidia

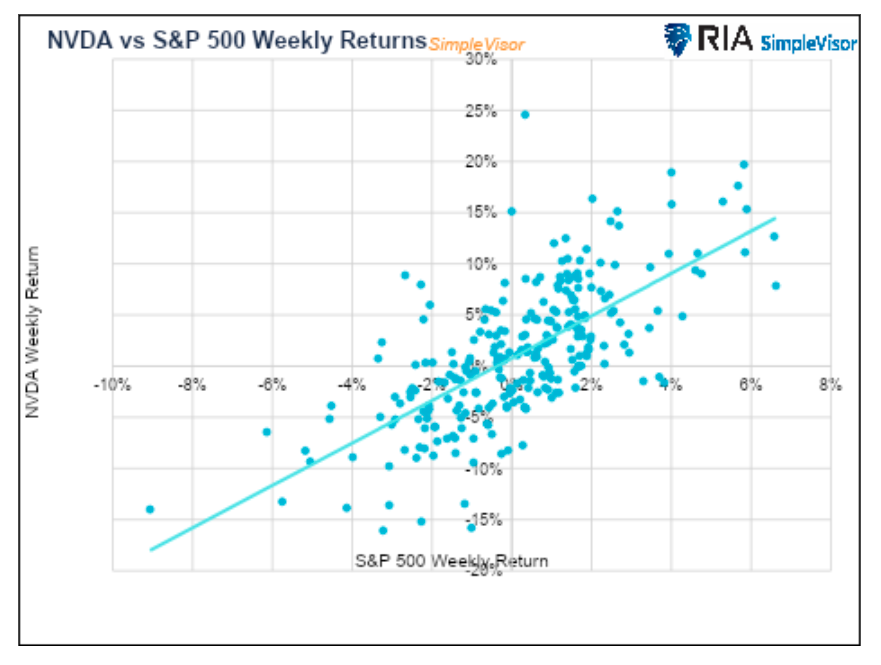

We shift our focus to Nvidia (NVDA), a stock with a higher beta, to further illustrate why correlation (R-squared) is critical to understanding the efficacy of a stock’s beta. As shown below, NVDA has a five-year beta of 2.07; however, like XOM, it has been declining, with its three-month beta sitting at 1.10. This is not surprising given that Nvidia’s contribution to the S&P 500 has surged from about 1% to nearly 8% over the last five years. Its short-term beta implies that NVDA behaves similarly to the market — not twice the market as its longer-term beta claims.

The graph below shows that NVDA's best-fit trend line has a steeper slope ( a higher beta) than XOM's. Moreover, we can see that the dots are more closely clustered around the trend line than XOM's are. The relationship between NVDA returns and the market, as measured by R-squared, is 0.4785 compared to XOM’s insignificant 0.0645.

Idiosyncratic Risk

Some describe beta as if it were like a volume control on a stereo, simply turn the beta up or down, and your risks change accordingly. The dispersion of weekly returns around the trend line indicates that other factors, in addition to market returns, drive individual stock returns. While there are many factors driving returns, they can largely be classified as systematic (beta) or idiosyncratic.

Beta only helps explain the fraction of a stock's return attributable to systematic (market) risks. These are market risks that affect all investments simultaneously and include factors such as recessions, interest rate changes, and geopolitical events.

Idiosyncratic risk, on the other hand, is the company-specific risk. It includes unique factors such as management decisions, product sales, and competitive positioning. It also includes non-company-specific factors, such as investor preferences.

Together, systematic and idiosyncratic risks help us fully quantify risk.

As we discussed, XOM had a very low R-squared because many of the data points were randomly scattered across the graph. We can deduce from the low correlation (low R-squared) that changes driven by idiosyncratic factors greatly outweigh those driven by movements in the S&P 500.

Portfolio Beta

So far, we have only discussed the beta of an individual stock. Given the idiosyncratic risks and low correlation (R-squared) of many stocks, and the fact that beta shifts with the selected time frame, beta can be an inadequate tool.

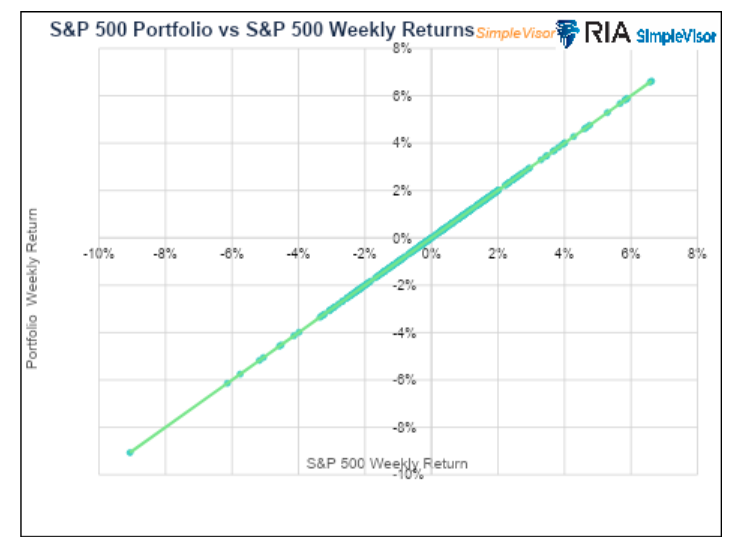

However, when managing a portfolio, beta’s usefulness as a portfolio management tool increases. In the extreme, think of it this way: if you bought all 500 S&P stocks in the same percentages as the index, the portfolio’s beta and R-squared would each be one, thus you would have zero idiosyncratic risk. The idiosyncratic risks associated with all 500 stocks would cancel each other out. The graph below plots this scenario.

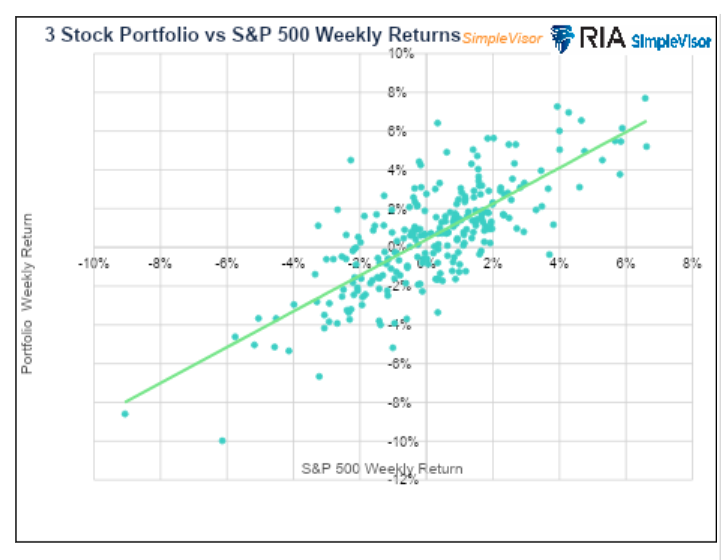

The more diversified your portfolio, the more idiosyncratic risk you remove from your portfolio. To highlight this, we created a simple three-stock portfolio containing equal amounts of XOM, NVDA, and Duke Energy (DUK).

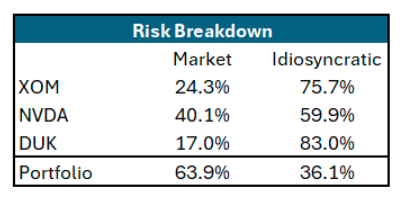

As shown below, the beta of our portfolio is 0.9994, and the R-squared is 0.5855. Below the graph is the summary of market and idiosyncratic risks for the three stocks and the portfolio.

Even with three stocks and minimal diversification in our portfolio, we have substantially reduced the idiosyncratic risk compared to the risk implied by the individual stocks.

Summary

Beta is useful but imperfect. And, unfortunately, its imperfections tend to matter most when the need to manage risk is most critical. As the age-old saying goes: “In the midst of a crisis, all betas go to one.” Simply, beta can be a broken compass when you need it most.

For individual stocks with low R-squared values and high idiosyncratic risk, such as XOM, beta can be a poor predictor of actual price behavior, particularly during periods of sector- or company-specific volatility.

For well-diversified portfolios, beta is considerably more reliable, as idiosyncratic risks of the underlying stocks cancel out and systematic market risk dominates.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All