Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

The debate over ETFs versus mutual funds has never been particularly useful for advisors who actually build portfolios. In practice, the question was never which vehicle is better — it was always which vehicle is better for this objective, in this sleeve, for this client. In 2026, that discipline matters more than ever.

Markets have grown simultaneously more concentrated and more complex. Passive ETF flows have deepened the dominance of a handful of mega-cap names in U.S. equity benchmarks. Fixed income volatility has made duration management a tactical, not just strategic, consideration. And a broader menu of active strategies, many now available in both ETF and mutual fund wrappers, has made vehicle selection a genuine portfolio construction decision rather than a default habit.

The advisors navigating this environment most effectively are not the ones who have committed to one structure or the other. They are the ones who understand when to use each and how to deliberately manage the combined exposure across asset classes.

The 2026 Portfolio Environment: Key Trends Shaping Asset Allocation

Three dynamics define the construction challenge advisors face today:

1. Navigating Higher-For-Longer Rates

Rates have remained structurally higher than the post-2008 baseline, reshaping the return profile of fixed income and forcing a more active approach to duration and credit allocation. Bonds are back — but not all bonds, and not in all wrappers.

2. Managing U.S. Equity Concentration Risk

U.S. equity concentration risk is no longer a theoretical concern. The top 10 holdings in a standard S&P 500 ETF represent a historically large share of the index. Advisors layering multiple passive equity products on top of each other without auditing overlap are not diversifying; they are doubling down on the same handful of names.

3. Adapting to the Shift Toward ETFs

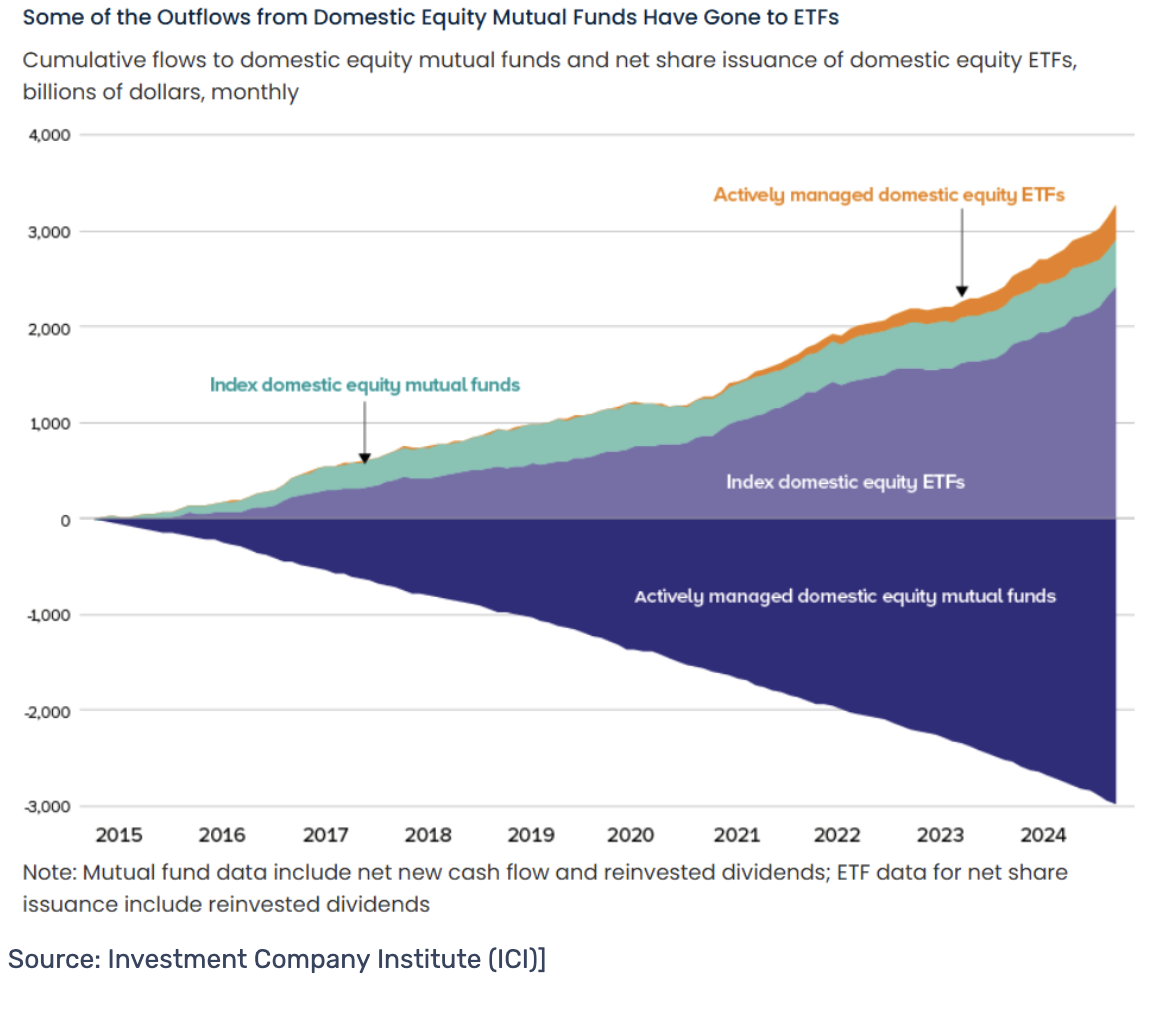

The structural shift from mutual funds to ETFs has accelerated; the flow data tells that story clearly. As shown in the chart below, U.S. ETFs have absorbed trillions in net new flows over the past five years, while actively managed mutual funds have faced persistent and deepening outflows. This migration is not merely a cost story, it reflects a fundamental change in how advisors and investors think about portfolio construction.

ETFs vs. Mutual Funds: How to Choose the Right Investment Vehicle

The case for ETFs in a modern portfolio is well established. They offer intraday liquidity, tax efficiency through the in-kind creation and redemption mechanism, generally lower expense ratios on passive strategies, and ease of implementation across brokerage platforms. For core market exposure — domestic large-cap equity, broad investment-grade fixed income, and international developed markets — ETFs typically represent the most efficient delivery mechanism available.

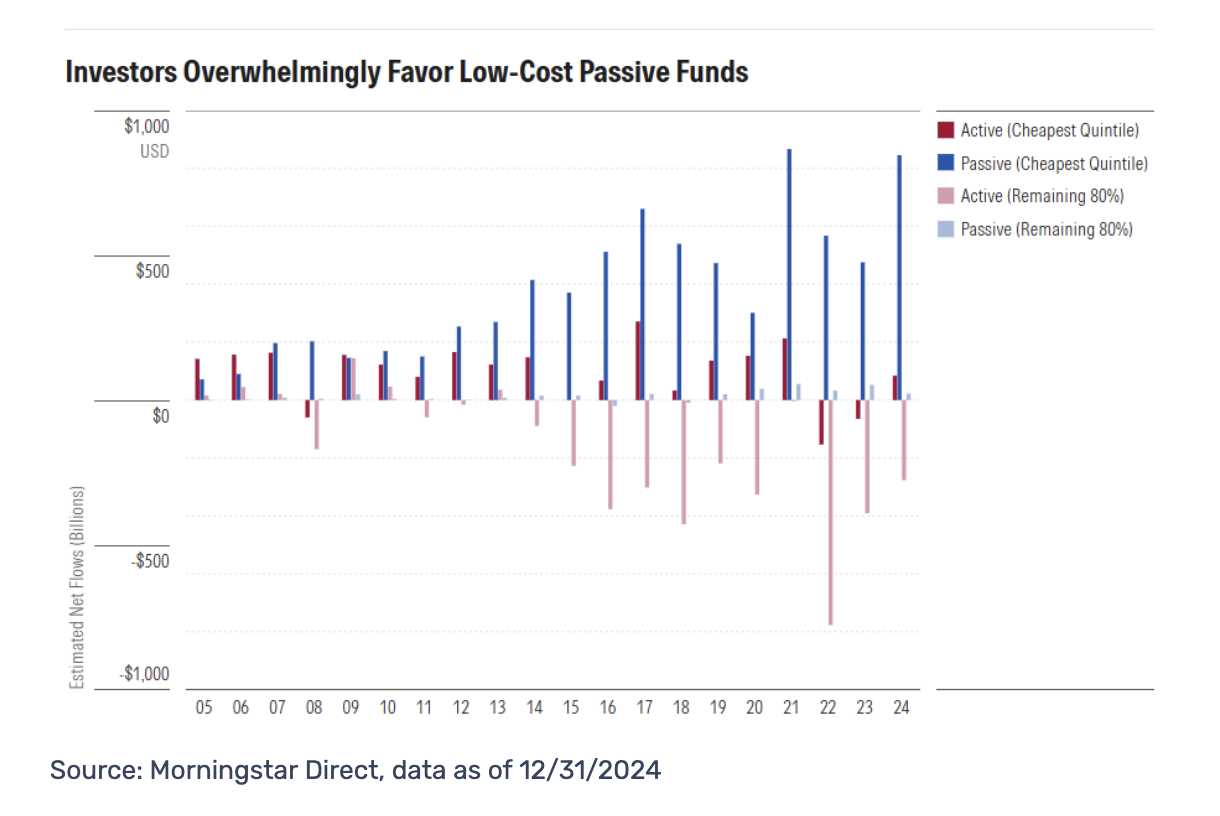

Cost is a meaningful part of the story. According to a recent Morningstar article, ETFs Improve Odds of Success for Active Managers, the author notes that active ETFs are, on average, 37 basis points cheaper than active mutual funds. That structural cost advantage meaningfully shifts the odds in favor of investor success. As Morningstar's broader fee data illustrates, the asset-weighted average expense ratio for passive ETFs has fallen below 0.10% for many categories, while actively managed mutual funds in the same asset classes can carry expense ratios of 0.50% to over 1.00%. Over a 20-year horizon, that fee differential compounds into a significant drag on net returns — making cost discipline a non-negotiable starting point for vehicle selection.

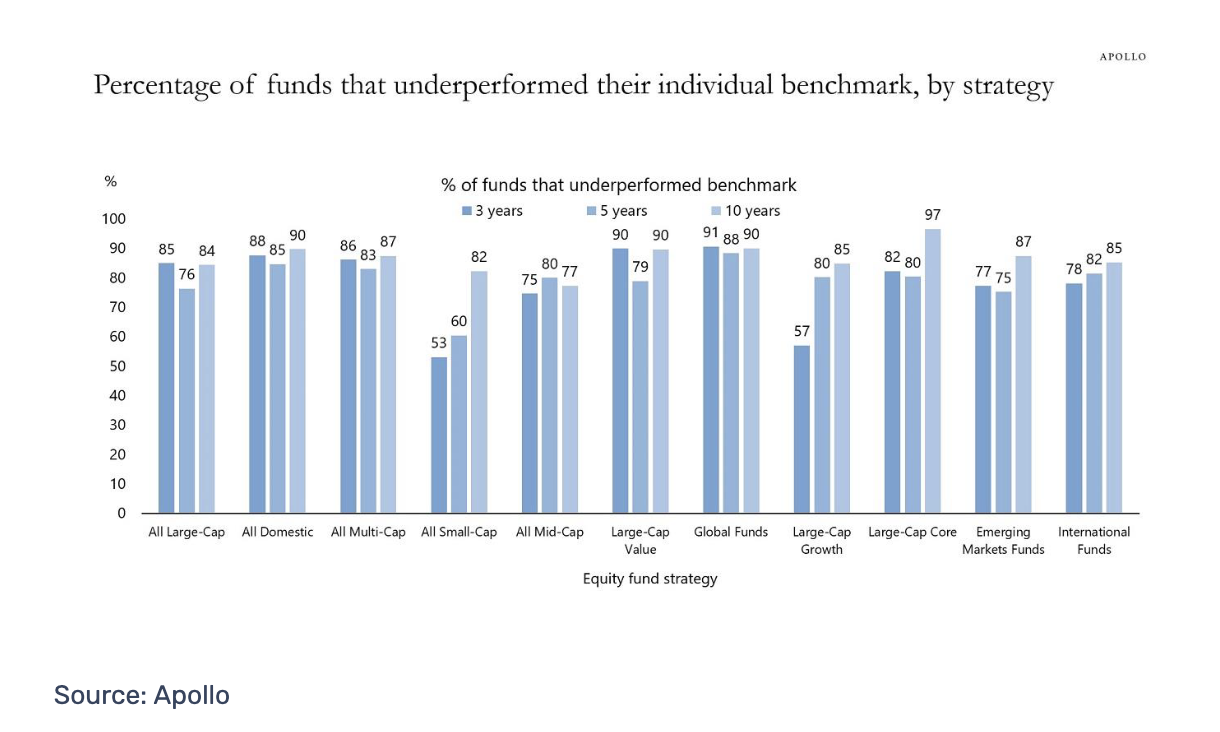

The performance data reinforces the cost argument. According to Apollo's analysis, across virtually every major equity strategy, the majority of actively managed funds have underperformed their individual benchmarks over 3-, 5-, and 10-year periods. Large-cap core funds show the starkest picture, with 97% underperforming over a decade. Even in categories where active managers have historically claimed an edge — emerging markets and international funds — underperformance rates over 10 years run at 87% and 85%, respectively. The one partial exception worth noting is all small-cap, where the three-year underperformance rate of 53% is meaningfully lower than the rest of the universe, pointing to some residual opportunity for active selection in less efficient segments of the domestic market.

Mutual funds retain meaningful advantages in specific contexts. Active strategies with high portfolio turnover can be more tax-efficiently housed in tax-advantaged accounts, where the in-kind ETF tax benefit matters less. Certain asset classes — some multi-sector bond strategies and a range of alternative approaches — still lack ETF equivalents of comparable depth or manager quality. In less liquid markets, end-of-day mutual fund pricing can be preferable to an ETF that swings to a significant premium or discount during a volatile session. However, a counterargument is that the ETF price may be the more honest real-time signal, with the mutual fund NAV simply lagging behind.

Bank loans are a good example of how nuanced this gets. Active ETF wrappers exist — the State Street Blackstone Senior Loan ETF (SRLN) being one example — but carry above-average turnover and fees, and function more as access vehicles than quality benchmarks. The broader ETF universe for bank loans remains thin relative to mutual funds, and several of the most established managers in the sector simply haven't moved their strategies across. For an investor with a strong view on a particular manager, a mutual fund may still be the only way in.

Active ETFs have, on average, posted better net-of-fee returns than their mutual fund counterparts — but it's important to be clear about why. The advantage is structural: lower costs, better tax efficiency, and no cash drag from redemptions. It isn't evidence that the same manager, running the same strategy, somehow picks securities better inside an ETF wrapper. That distinction matters because it leads to an obvious question: If the edge is just the structure, why would anyone still choose an active mutual fund?

For a large portion of investors, the answer is simple — they don't have a choice. Most 401(k) plans were built around mutual funds, and the recordkeeping infrastructure, share class arrangements, and revenue-sharing agreements that underpin them have made ETFs difficult to offer on many platforms. That is slowly changing, but today a significant number of retirement savers can only access active management through a mutual fund, regardless of what they might prefer.

The practical recommendation for most is that the best-constructed portfolios tend to use both. ETFs anchor the core. Active mutual funds fill specific roles — where a favored manager hasn't launched an ETF version of their strategy, where the retirement plan limits the options available, or where there's a genuine case that active management has a realistic shot at beating the benchmark on a risk-adjusted basis and also net of fees.

How to Manage ETF and Mutual Fund Exposure Across Asset Classes

U.S. Equities

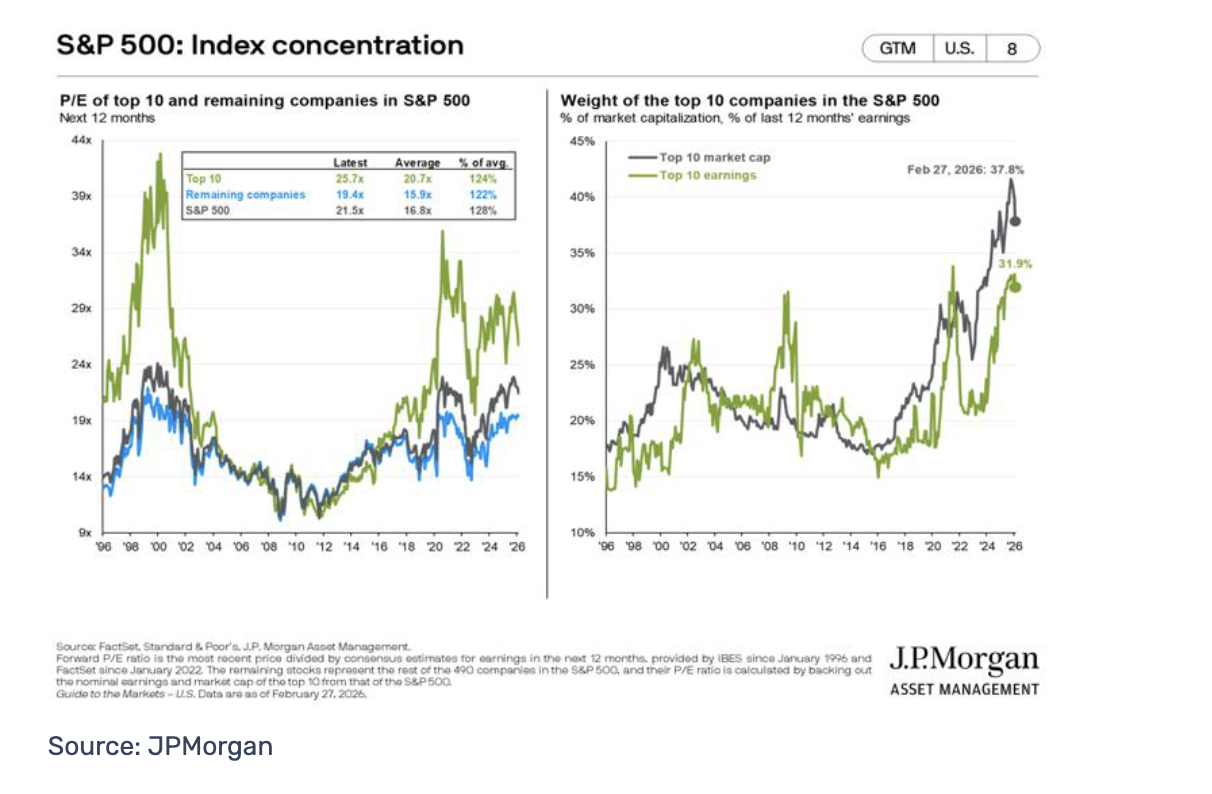

The core risk in domestic equity construction today is unintended concentration. An advisor running a passive large-cap ETF alongside an actively managed large-cap growth mutual fund may believe they have a balance. However, if both portfolios are heavily weighted to the same mega-cap technology names, the diversification is largely cosmetic. JPMorgan's analysis of S&P 500 index concentration illustrates just how acute this risk has become, with the top names commanding a share of the benchmark that is historically elevated by any measure.

The solution is exposure auditing. Tools that aggregate holdings across vehicles and surface factor tilts — growth/value, quality, momentum, size — allow advisors to make active decisions about what the combined portfolio actually owns, not just what each individual holding is supposed to represent. ETFs are particularly useful for surgical tilts: adding a value factor ETF to counterbalance a growth-heavy active mutual fund is a precise and low-cost way to rebalance factor exposure without liquidating the active position.

International & Emerging Markets

Developed international markets have become increasingly ETF-friendly, with deep, liquid products covering regions, countries, and factor exposures globally. For broad, developed market exposure, a passive ETF is generally the right tool.

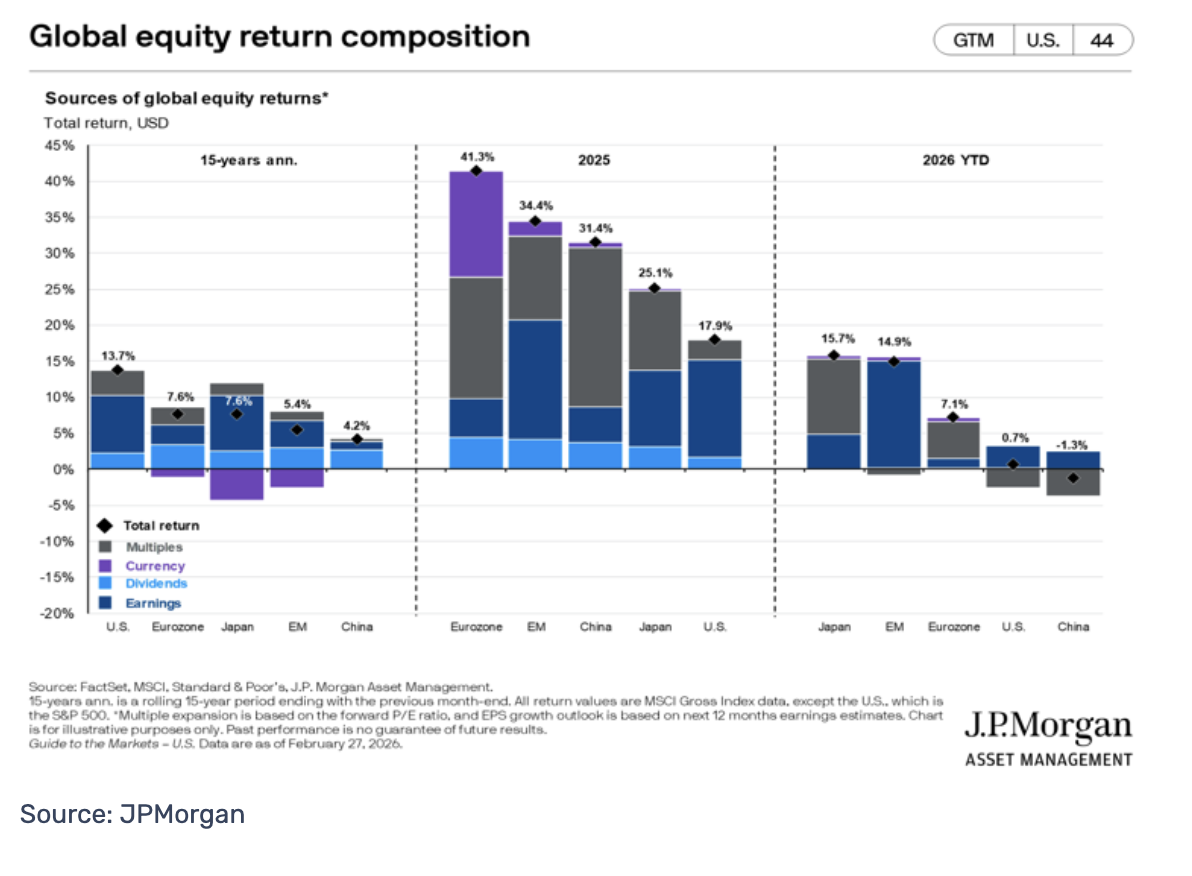

Emerging markets are a different story. Market inefficiency, corporate governance variability, and significant dispersion of returns across countries and sectors create a genuine opportunity for active managers to add value. JPMorgan's return dispersion data makes this case visually. The gap between top- and bottom-performing managers in emerging markets is substantially wider than in developed markets, which means manager selection matters far more than the vehicle choice alone.

Here, a high-conviction active mutual fund — run by a manager with demonstrated local market knowledge — may warrant a place alongside or instead of a passive EM ETF. The key is evaluating whether the active premium is justified by the opportunity, not assumed by default.

Fixed Income

Fixed income construction has become one of the more nuanced vehicle-selection questions in the current environment. ETFs offer precision. For example, an advisor who wants to express a specific duration view, shortening to three years, while the yield curve normalizes, for example, can do so with a targeted ETF in a way that would be cumbersome using a mutual fund with a defined mandate.

For credit selection, active mutual funds often have the edge. Skilled fixed income managers can navigate sector rotation within investment grade, identify relative value in high yield, and manage credit risk in ways that a market-cap-weighted passive ETF structurally cannot. A blended approach — passive ETF for duration management, active mutual fund for credit alpha — is increasingly common among advisors running sophisticated fixed-income sleeves.

Alternatives and Real Assets

In alternatives, mutual fund structures still dominate for most advisory channels. Liquid alternatives — managed futures, long/short equity, market-neutral strategies — are available in mutual fund form with daily liquidity and established track records. The ETF wrapper for true alternatives remains limited in depth and manager quality, though the product landscape is evolving.

Real assets, including REITs and commodities, are areas where ETFs have become fully mature delivery vehicles. For infrastructure and direct real estate exposure, closed-end structures or interval funds may be more appropriate — a reminder that the vehicle conversation extends beyond the ETF/mutual fund binary.

Practical Portfolio Construction Considerations

Several operational considerations shape how advisors implement a blended ETF and mutual fund portfolio.

-

Overlap analysis tools can surface redundant exposure across vehicles and help advisors make deliberate decisions rather than allow unintended portfolio drift. While a few semi-transparent active ETFs exist, most active mutual funds only disclose holdings every few months (or even quarterly), making timely overlap detection more challenging. This highlights one of the longstanding advantages of ETFs: their superior transparency compared to traditional active mutual funds.

-

Tax management is an area where the two vehicles interact directly. ETFs are well-suited to tax-loss harvesting — swapping between correlated ETFs to realize losses while maintaining market exposure. Active mutual funds held in taxable accounts require more care, particularly around year-end capital gain distributions. Where possible, tax-inefficient active mutual funds belong in tax-advantaged accounts.

-

Fee budgeting across a blended portfolio requires discipline. The cost advantage of passive ETFs can be partially or wholly offset by high-cost active mutual funds in sleeves where the active premium is not justified. Advisors should evaluate the all-in cost of the combined portfolio against the expected value-add of each active sleeve.

-

Rebalancing mechanics differ meaningfully between vehicles. ETFs can be traded intraday in fractional amounts, making precision rebalancing straightforward. Mutual funds may carry minimums, redemption fees, or short-term trading restrictions that affect implementation. Advisors should understand the operational constraints of each vehicle before designing a rebalancing framework.

Matching Investment Vehicle to Portfolio Objective

The most durable framework for portfolio construction in 2026 is deceptively simple: Match the vehicle to the objective, not to habit or convention.

ETFs offer efficiency, liquidity, and precision. Use them for core exposures, factor tilts, and tactical adjustments. Mutual funds offer access to active management, deeper strategies in less liquid markets, and established track records across a wider range of approaches. Use them where manager skill is demonstrable, and the structure is suited to the underlying market.

The advisors who will serve their clients best in the years ahead are not the ones who have picked a side in the ETF-versus-mutual-fund debate. They are the ones who have moved past it — building portfolios that use each vehicle for what it does best, auditing exposures deliberately, and adapting as the product landscape continues to evolve.

— — —

About The Author

Nadeem, CFA, MBA, is a chief investment strategist and portfolio manager with 20+ years’ experience across major global banks. Extensive senior-level tenure across premier global and Canadian institutions, including RBC, Raymond James, CIBC, Deutsche Bank, and Citigroup. At Marnoa, he leads investment strategy and portfolio management with a focus on North American equities.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Nadeem Kassam

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.