Tesla Inc. and its Chief Executive Officer Elon Musk are a font of big numbers, real or imagined: A million robotaxis deployed, 20 million electric vehicles sold per year, “tens of billions” of Optimus robots stalking the Earth. Here is another that, with the release of what are likely to be dreadful first-quarter results fast approaching, ought to be more relevant: $43.9 billion.

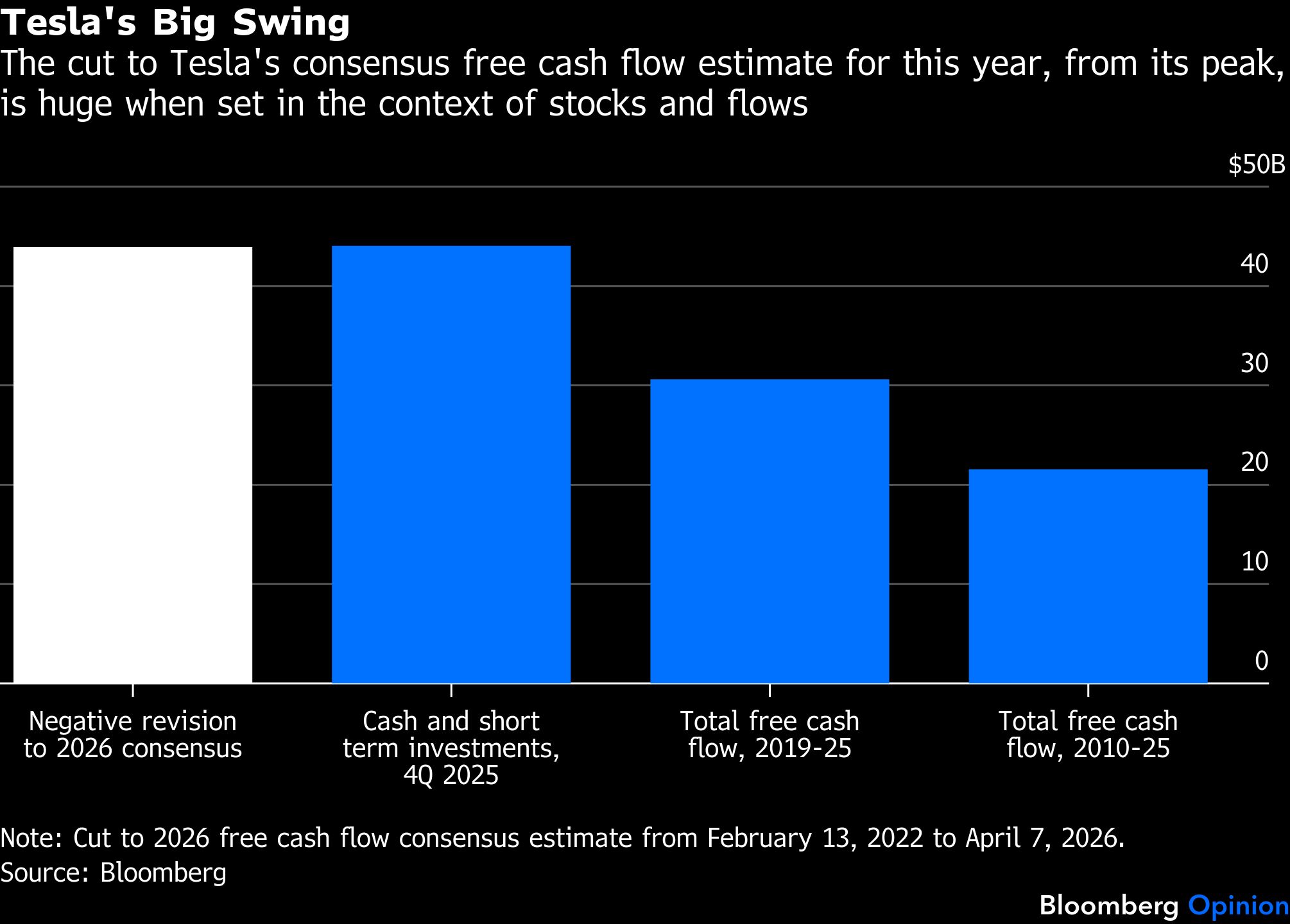

That amount represents the swing in analysts’ consensus forecast for Tesla’s free cash flow in 2026, from a peak expectation of $38.8 billion in February 2022 to today’s projection of negative $5.1 billion. The flip from self-funding to cash burning is notable on its own, but it’s the sheer scale that is significant. More specifically, it is almost exactly the same amount of cash and equivalents Tesla had on its balance sheet at the end of December. It is also double the entire amount of free cash flow Tesla has generated across all its years as a public company. It even outstrips the total amount generated if you count only the years when Tesla’s free cash flow was positive.

For most companies, a slump of such epic proportions would be a disaster. At the very least, it would hit valuation models like a stick of dynamite.

With Tesla, it has underpinned a massive rerating of the stock… upwards. Earnings are an accounting proxy for free cash flow, and while the consensus for those in 2026 hasn’t gone negative, they have also collapsed over the past four years or so. Yet the stock has risen over the same period, meaning the implied multiple — a numerical expression of confidence, in essence — has jumped by a factor of five, to 178 times expected earnings for this year.

Tesla dropped the bombshell that it would burn billions of dollars in 2026 during its earnings call in January. Its sales and production figures for the first quarter, released earlier this month and showing 358,023 vehicles delivered falling short of an already low average forecast of 372,160, signaled the match was lit immediately. Even though deliveries rose 6% from a year earlier, the gain looks less impressive when you consider that sales in the first quarter of 2025 were the lowest in more than two years.

Worse, Tesla’s factories churned out more than 50,000 vehicles in the first quarter that went unsold, a record amount of excess units for the company. It implies a working capital headwind on finished goods inventory alone of about $1.7 billion.The only other period in which Tesla overproduced to a similar degree, the first quarter of 2024, saw free cash flow swing to negative $2.5 billion. The big miss on grid-battery sales, which generated a fifth of Tesla’s gross profit in the fourth quarter of 2025, will compound the hit. Meanwhile, sales of regulatory credits that Tesla gathers for selling zero-emission vehicles, an important crutch for earnings over the past two years, should also come under pressure due to the roll-back of US tailpipe regulations under a president Musk helped get elected.

Rather than constituting a mere miss, a business that is now anticipated to burn $5 billion in a year is simply not the same business that was forecasted to generate eight times that amount. For some, including many Wall Street analysts covering Tesla, that is actually a plus. Remarkably, the average price target on Tesla today implies a bigger premium to the stock price, 20%, than in February 2022. The combined proportion of holds and buys, 79%, is also higher. This is despite the collapse in financial and operational projections put forth in countless reports across that period.

One analyst, JPMorgan Chase & Co.’s Ryan Brinkman, had the clarity to point this out in a report published this week (his price target implies almost 60% downside). But what mostly fills the void is a narrative of ever bigger numbers, some of which have been missed already, such as for robotaxis, or are speculative to the point of fanciful.

In this inverted dimension, Tesla spending beyond its cash flow isn’t a cause for concern but instead a portent of success. Expect such self-justifying logic to feature prominently when the numbers drop, in all senses, later this month.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.