“Meet the new boss, same as the old boss,” sang The Who. A similar vibe hangs over billionaire Bill Ackman’s $65 billion takeover proposal to move Amsterdam-listed Universal Music Group NV to the US, sell its stake in Spotify Technology SA and return more cash to shareholders.

The idea that this would be enough for “new UMG” to almost double the current one’s valuation doesn’t add up at a time when artificial intelligence is creating doubts about the industry’s future. And it’s unlikely on its own to tempt dominant shareholders such as French tycoon Vincent Bollore. The proverbial fat lady has yet to sing.

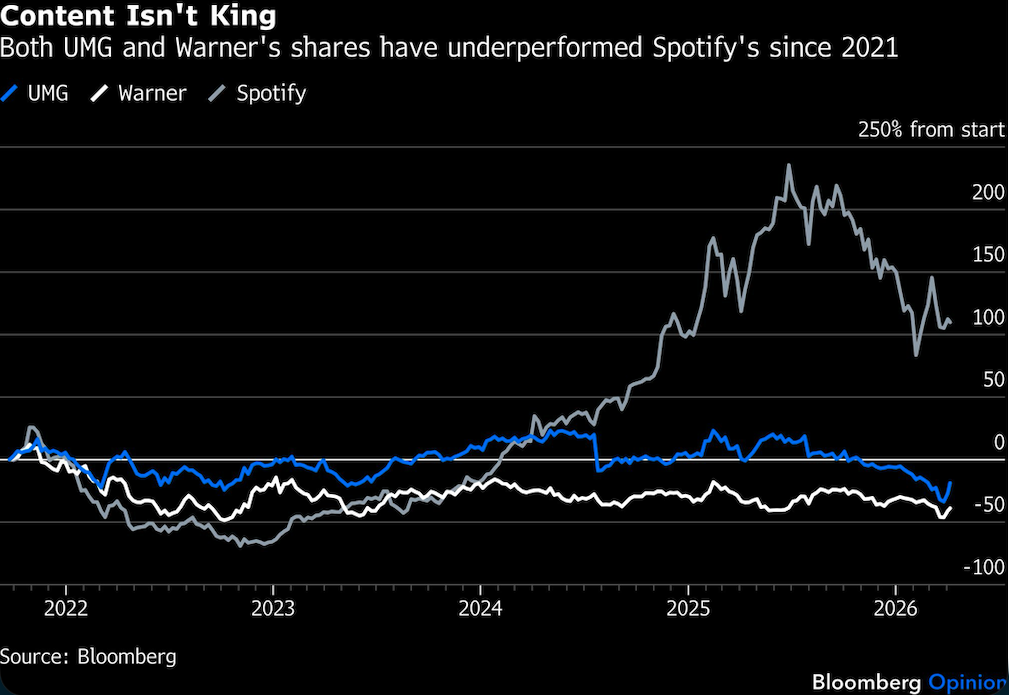

Ackman’s shareholder blues (he controls 4.5% or so of UMG stock) are understandable. Music is everywhere thanks to streamers, industry revenues have risen every year for more than a decade and the modern fandom of Taylor Swift and BTS is every bit as obsessive as Beatlemania was in the ‘60s. So why are shares in UMG, the world’s largest music company, down by about 20% since its 2021 stock-market listing, while those of Spotify — whose ability to hike prices and expand subscriber numbers arguably depends on tunes from UMG icons such as Swift and Billie Eilish — has more than doubled?

The way Ackman tells it, this is about sweating the asset. If only the label and its veteran boss Lucian Grainge were able to take on more risk, hand back more money to investors and relocate to the US, the stock would soar.

But this is a utopian vision verging on the Woodstock-esque. Ackman’s €56 billion ($65 billion) offer incorporates a small cash component of €5.05 per share plus 0.77 shares of the post-deal UMG, which the billionaire reckons together values the stock at €30.40 per share, a premium of 78% to UMG’s last pre-announcement close.

That’s quite a leap of faith considering the changes on offer don’t exactly amount to a revolution, and the UMG share price reaction indicated as much, closing on Tuesday at €19.05. Some analysts moot that a music company with an American listing would have higher-rated stock, but that’s debatable. Shares in UMG’s US-listed rival Warner Music Group Corp. are trading at a roughly similar multiple of expected earnings.

And €1.5 billion in net proceeds from selling UMG’s Spotify stake is unlikely to move the needle much on its long-term prospects aside from helping to fund the bid itself.

The proposal to take on more debt to return more cash to themselves is, in fairness, something other investors are keen on. Doing that might even be enough to keep Ackman sweet without going the whole hog on his proposals. “UMG has a lot of balance-sheet flexibility… It could do more aggressive buybacks,” says Marius Bakker, a portfolio manager at Van Lanschot Kempen.

Yet even this kind of financial engineering demands confidence in the future of big music labels at a time when streaming has commoditized the listening experience and artificial intelligence brings so many unknowns. UMG has arm-twisted Spotify and its ilk to combat “AI slop” and unlock new price tags for superfans. But the fear of AI disruption or falling market share hasn’t gone away. Bloomberg Intelligence’s Matthew Bloxham says a more cautious approach to balance-sheet management, coupled with bolt-on acquisitions in faster-growing markets, might make more sense.

All in all, what’s being pitched here looks a lot like the same old UMG but listed in a new jurisdiction with a small cash sweetener. If they even halfway believe Ackman’s very bullish mooted valuation, it’s hard to see why cornerstone investors such as Bollore and Tencent Holdings Ltd. would cede control unless a bigger sweetener were to emerge. Alphavalue analyst Alexandre Desprez wrote that even in a blue-sky scenario whereby all AI fears disappear, UMG could be worth €27.20, still well below Ackman’s reckoning.

When the US hedge fund billionaire bought into UMG in 2021, he compared music to an essential need just after food and water. He was right, but for now it is Spotify making the most money from meeting that need. If pop stars’ content is indeed king, rather than the technology that distributes it, it will take more than this proposal to prove it.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Lionel Laurent