The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.

While artificial intelligence is unlikely to replace financial advisors, it can certainly enhance both the quality and the productivity of advisors who embrace it. In fact, Vanguard’s Global Chief Economist, Joseph H. Davis, examined how AI and other megatrends will shape the economy in his book, Coming Into View (Wiley, 2025). Davis predicts AI will raise advisors’ productivity and increase the value of advice.

I agree that AI will boost productivity, but I wanted to put it through the test now to see how accurate and insightful it was. To do so, I gave Anthropic’s Claude a spin. I had it analyze a relatively simple portfolio to see what changes should be made, especially on a recent infusion of $80,000 cash.

While this portfolio isn’t mine or even a client’s, I did have some input in designing the portfolio. A recent study entitled “Offended by the algorithm: The hidden interpersonal costs of clients seeking AI second opinion” showed advisors were more offended by a second opinion from AI than a live person. That said, I was anxious to see how Claude responded.

Methodology

Using Claude’s paid pro plan ($200/year), I downloaded four February 2026 statements in PDF format. They consisted of two Vanguard statements, one consolidated Fidelity statement, and one employer 401K statement held at Fidelity. Because the employer statement didn’t break down the holdings in the Roth vs. the traditional portion of the portfolio, I manually gave this information to Claude.

Next, I gave Claude a target asset allocation of 68% equities with two thirds of those equities in U.S. stocks and the remaining third in international. I asked Claude to summarize the portfolio and make recommendations, including how to invest the cash recently added. I provided Claude a bit of feedback, but not much.

The following are summary reports, analysis, and recommendations from the four statements downloaded to Claude. After which, I’ll share my analysis and just how useful AI could be to financial planners and clients now and in the near future.

Claude produced the following reports and recommendations from about 20 pages of raw statements. The name of the portfolio owner is a pseudonym.

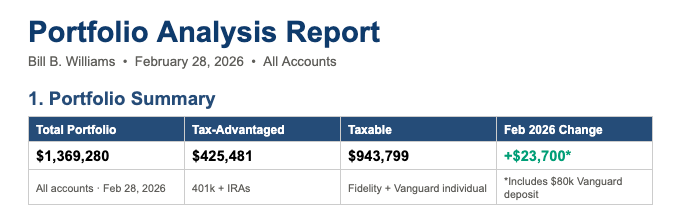

Your total portfolio value across five accounts stands at $1,369,280 as of February 28, 2026. The portfolio is distributed across tax-advantaged retirement accounts ($425,481) and taxable brokerage accounts ($943,799).

Current placement is well-optimized:

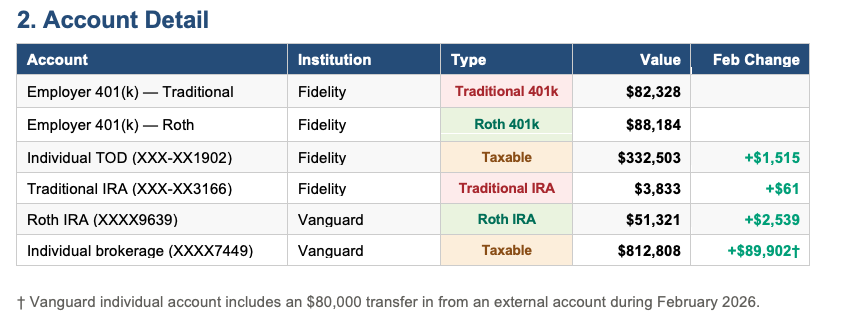

- EMPLOYER 401k Traditional holds FIAM US Bond Index — correct (bonds in tax-deferred)

- EMPLOYER 401k Roth holds SP Intl Index — correct (international stocks in Roth)

- Vanguard Roth IRA holds VXUS — correct (high-growth international in tax-free)

- Fidelity Traditional IRA holds FXNAX bond fund — correct, though Roth conversion worth considering given small balance ($3,833)

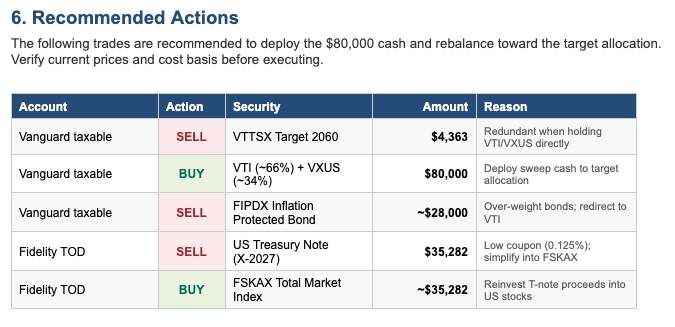

$80,000 cash deployment split: VTI ~$53,000 (fills US stock gap) + VXUS ~$27,000 (boosts international toward target)

Concentration risks:

- Merck (MRK) and Organon (OGN) — ~$16k, ~1.2% of portfolio. Only source of idiosyncratic stock risk. Consider liquidating into FSKAX over time, especially on any loss positions.

- The portfolio has no dedicated real estate (REIT) or commodities exposure — optional tilts, not a gap.

* FIAM 401k CIT share class expense ratios are not publicly disclosed. Figures are estimates based on typical institutional pricing. Check your EMPLOYER plan's annual fee disclosure for exact amounts.

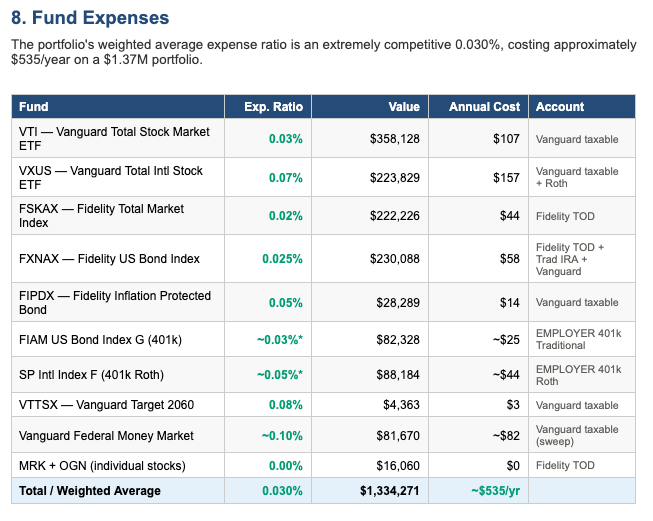

Over 20 years at 7% annual growth, the expense ratio advantage vs. the industry average compounds to approximately $180,000+ in additional wealth retained.

Disclaimer: This report is for informational purposes only and does not constitute financial, tax, or investment advice. Portfolio values are based on account statements dated February 28, 2026. Prices and balances will have changed since that date. Consult a qualified financial advisor before making investment decisions.

Analysis of Claude’s Work

I thought Claude did a beautiful job of summarizing what was most important and displaying it in a visually appealing and understandable way. It correctly noted several important points such as:

- The fact that the cash was recently added and needed to be invested.

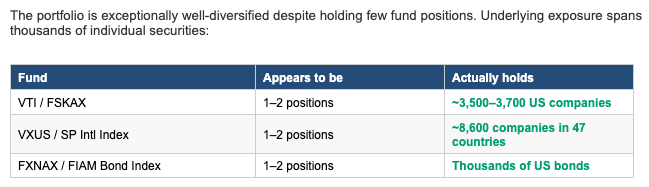

- The portfolio was well diversified. It recognized that diversification is more about the holdings of each fund rather than the number of funds. It actually displayed the number of companies in each fund.

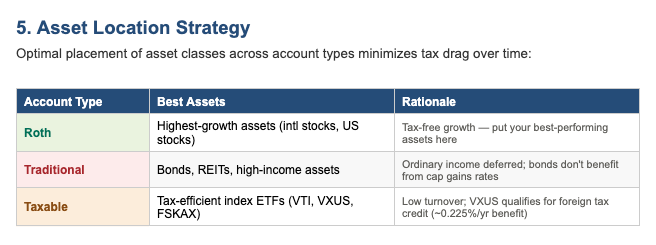

- The asset location from a tax perspective was generally good.

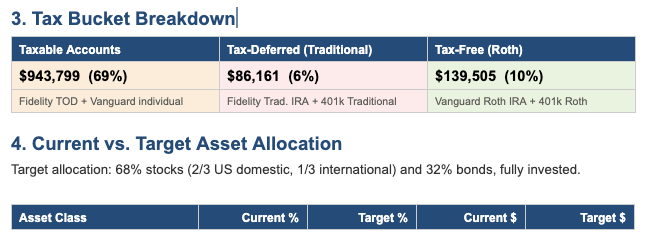

- The equity allocation was below the target given.

- The expense ratio of the portfolio was very low.

If this analysis had been done by a student in an intro to investments class (which I taught for several years), it would have received a passing grade — but certainly wouldn’t have aced the project.

There were several material errors, mostly related to bad math.

- The first three tables show breakdowns of the totals in three different and useful ways. However, the totals should be the same but aren’t. Claude excluded over $200,000 of taxable investments.

- The total values in many tables kept changing.

- Though most recommendations were directionally correct, the calculations were wrong.

- Some recommendations were downright wrong. For example, Claude recommended selling a Treasury because it was yielding only 0.125%. It failed to recognize the bond was bought at a discount and the yield was quite good.

- Claude advised selling a low-cost Fidelity inflation-protected bond fund because it was overweighted in bonds. The portfolio was not overweighted in bonds. It also didn’t tell me what to buy in its place.

Today’s bottom line

Overall, I was impressed with Claude. It summarized the portfolio in useful ways, though that could be dangerous when materially inaccurate. The notably faulty tax wrapper allocations of taxable, tax-deferred, and tax-free wrappers exemplified this.

Much like I might treat a junior analyst, I asked Claude why it didn’t check its math to make sure the numbers added up to and accurately reflected totals. Claude responded:

Language models aren't calculators. Claude and similar models are trained to predict text, not to compute. When doing arithmetic, the model is essentially pattern-matching against how math looks in training data rather than actually executing operations. Small arithmetic — adding two numbers — is usually fine. Multi-step calculations with many variables accumulate errors fast.

The model is genuinely useful for structuring the problem, identifying what to calculate, and interpreting results. But any numbers that matter should be verified by executed code, not trusted from the model's prose alone.

But Claude offered a solution:

The fix — which is why running Python alongside the analysis matters — is to treat Claude as the analyst and let actual code do the arithmetic.

Since I don’t know the programming language Python, I thought that was of no use. I was wrong. Claude told me:

That's completely fine — you don't need to know Python to benefit from it. When you ask me to "check the math" or "run the numbers," I'm the one writing and executing the code behind the scenes. You just ask in plain English and I handle the rest.

Indeed, it fixed much of the math, and the solutions were better. However, it still would require human oversight to correct recommendations.

What’s Next?

I gave Claude a simple task. Financial planner Mike Piper, is extremely tech savvy, and I reached out to him. Piper is the creator of Open Social Security and publishes the Oblivious Investor blog. He told me that his experience using the browser-based LLM chatbots was similar to mine. He noted it can explain things clearly and do everything mostly correctly, but there will be errors here and there. And if you don't already know the subject matter, I imagine it would be very hard to catch the errors.

Piper said that he installed Claude Code, an AI-powered assistant, on his desktop and had it start building a financial planning application, step-by-step, per his specifications. In about 20 hours of work (over several days), he had something that was almost on par with a well-known financial planning software program he uses. He said he is now comfortable with the math as he hardcoded many mathematical checks into the application that Claude cannot alter on its own or circumvent.

Piper stated that Open Social Security took about 2,000 hours to build. He said if he was starting from scratch today and building it with Claude Code, he thought he could have it done in five to six days.

Piper ran the following scenario through Claude:

For John and Sarah [an existing sample set of data for two hypothetical retirees], we want to maximize spending, and we want to keep probability of portfolio default (using mortality table, rather than assumed death ages) below 5%. So allow the "overall spending" input to vary (high spending is goal). Assume spending will follow an inflation-adjusted path. The secondary (tie-breaker) metric of concern is after-tax estate left to heirs.

Keep asset allocation fixed. Rebalance annually. Consider a "tax strategy" to be a combination of Roth conversion, asset location, and which-accounts-to-spend-from-first inputs. Find the tax strategy that achieves the goal above. And tell me what else you learn.

It crunched numbers for several minutes, then gave an extremely detailed/insightful output. Piper said it's like having custom-built software and a coworker willing to spend all day running it to test different stuff. He said he has not used any real client data yet, as he wants to be absolutely rock-solid in his confidence. There’s more testing to do. But he views the entire experience as mind-blowing, right from the start.

Conclusion

AI has already been useful in the field of financial planning, and Piper and I were both blown away with what it can do. Notably, we have very different programming skill levels – Piper’s is strong while mine is nonexistent.

AI will only get better and likely very quickly. Advisors who embrace AI will have a huge competitive advantage over those who don’t. AI is no longer some futuristic theoretical tool. It’s here now, and it’s a game changer.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Allan Roth is the founder of Wealth Logic, LLC, a Colorado-based fee-only registered investment advisory firm. He has been working in the investment world of corporate finance for over 25 years. Allan has served as corporate finance officer of two multibillion-dollar companies and has consulted with many others while at McKinsey & Company.

Read more articles by Allan Roth

The views presented here do not necessarily represent those of Advisor Perspectives.

The views presented here do not necessarily represent those of Advisor Perspectives.