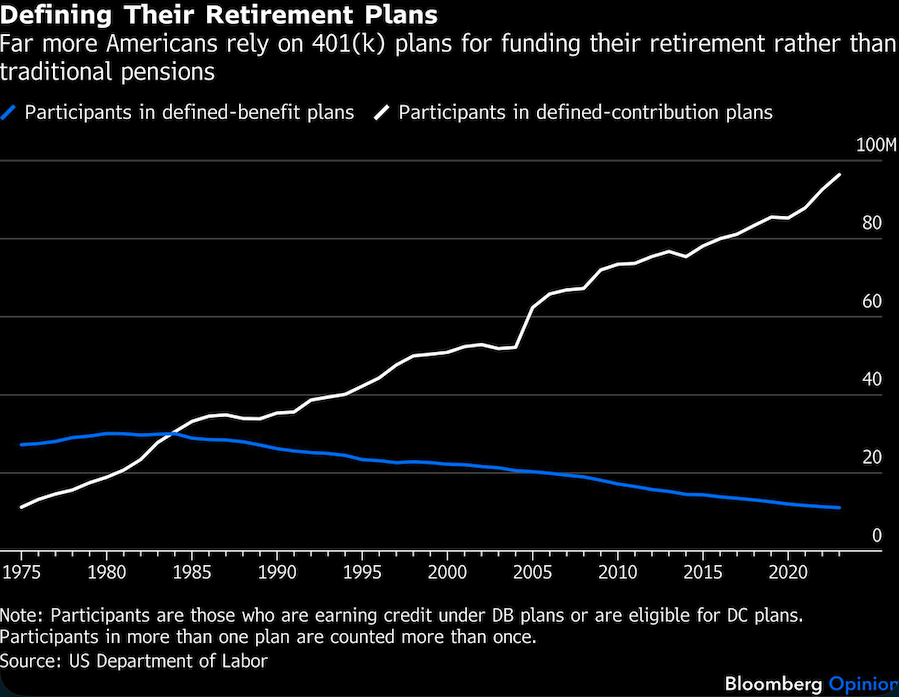

Once upon a time, not so long ago, about a third of all American workers had a gold-plated pension: When they retired, someone paid them nearly their full salary for the rest of their lives. They didn’t have to worry about the market, or inflation, or running out of money.

That time did not last, in large part because the someone who was paying for those pensions realized how expensive they were and how much risk they carried. So employers and governments around the world tried something different: Individual retirement accounts, which required everyone to manage their own risk.

The main attribute of this new system has been to clarify all the problems of the old one — and to create some new ones, too. And the Trump administration’s proposal to remedy these new problems incorporates some of the worst features of the old system.

One part of the new proposal would create a safe-harbor provision — essentially protection from liability — for a retirement plan’s fiduciary to offer alternative assets, such as private equity, as an investment option. (A fiduciary is a person or organization required by law to act in the client’s best interest.) The hope is to make defined-contribution (DC) pensions such as in a 401(k)s more like the defined-benefit (DB) plans so many Americas idealize.

There is a good argument that 401(k)s should be more like DB pensions. In fact, I spent the first half of my career trying to do exactly that. But DB plans are not better than 401(k)s because they can invest in alternative assets.

Despite all their training and expertise, many DB fund managers do not outperform index funds, once you account for fees. The idea is that private assets offer higher returns because they are less liquid and work on a longer time horizon. That may have once been true, but it’s not so much lately. For some pensions, private assets just enabled managers to ignore how underfunded they are. It’s not something 401(k) sponsors should want to emulate for their participants.

A better argument in favor of DB plans is that they pool risk across cohorts and individuals. If you retired when the market is down, your pension can be subsidized by someone who retired when the market was up. If you live to be 105, your pension is subsidized by someone who died when they were 72.

The proposed rule has more promising elements on this score. The safe-harbor provisions also apply to annuities, which pool longevity risk through an insurance company the way pensions do. The proposal also includes the possibility of offering a variable annuity as an investment, which allows the participant to opt for lifetime income at retirement at a favorable rate.

There is also guidance for plans to offer “lifetime income longevity-sharing pools.” Translation: a way for workers to pool their longevity risk without having to deal with an insurance company. One way this might work is through a modern tontine, where participants put their retirement wealth in a fund that earns a return and makes payouts each year. As each person dies, they forfeit their money to the fund, and they subsize those who live longer.

There have been proposals that included a safe-harbor provision for fiduciaries who offered insurance products, around As it now stands, any investment that reduces liquidity and has high, opaque fees (which describes many variable annuities) invites lawsuits. It’ s a risk few plan fiduciaries are willing to take — more so when the plan puts participants in these investments by default. The new proposal is an improvement to earlier rules, but it may not be enough to make fiduciaries comfortable offering variable annuities, let alone making them a default.

Annuities have never been popular, mostly because people don’t like to hand their wealth over to an insurance company or investment pool, and then not be able to get it back when they need it. Ironically, this is pretty much what people did back when DB pensions were more common.

The proposal’s guidance about annuities and tontines got less attention than the idea to allow access to private assets. But the guidance on annuities is potentially the best part of the new proposal because it takes what makes DB pensions better — pooling of risk — and adapts it to a 401(k).

The larger problem, on which I have made myself hoarse and which no regulation can fix, is that too many people still see their retirement accounts as wealth, not income. The real risk that fiduciaries should take on — and one that would pay off for them and the US economy — is trying to change how their clients think about their retirement accounts.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Allison Schrager