As private credit managers mount a spirited defense of their industry to discourage investors from fleeing, they’ve found at least one persuasive argument for why much of the cash they lent to software firms at the start of the decade shouldn’t be at risk. If the leveraged buyouts they financed do get into difficulties because of competition from artificial intelligence, the private equity owners are first in line to lose money.

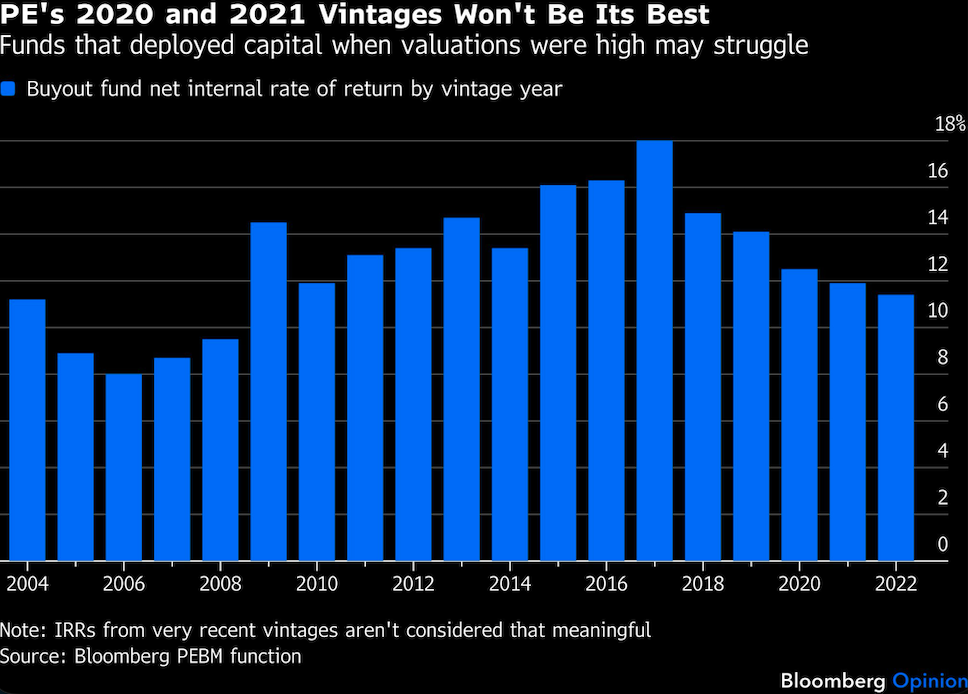

That could be bad news for the pension plans, sovereign wealth funds, university endowments and rich folk that funded private equity’s massive bet on software when euphoria peaked in 2021. It’s shaping up as a poor vintage.

To understand why PE firms are on the hook, remember that in a typical software-company buyout they will often have contributed more than half the purchase price as equity, with private credit providing the remainder as debt.

The latter’s senior secured loans have a priority claim on the company’s cash flows and assets. So, in theory, the software firm’s value would need to fall by roughly 60%-70% to wipe out that loss-absorbing equity cushion and expose creditors to losses too.

Private equity, of course, has form in forcing creditors to take the pain when a company hits trouble, but that’s when it has tapped the broadly syndicated loan market, where banks underwrite the debt and then parcel it out to a large group of lenders. Private credit is different because it usually involves only a small group of lenders who are harder to divide and conquer. Their debt also tends to have better legal guardrails than the weak terms on BSLs.

Still, such is the potential AI disruption that I’m not convinced even a 60%-70% equity buffer will be enough to let private credit lenders avoid losses — or that PE firms will always stump up extra cash when there’s a problem. Software valuations have been under serious pressure amid fears that Anthropic PBC’s AI tools will cause tech firms to lose customers and pricing power, perhaps even making them obsolete.

At the same time, it’s hard to disagree with Doug Ostrover, co-chief executive officer at Blue Owl Capital Inc., one of the firms at the center of the recent private credit selloff, who says: “If you're worried about direct lending at all, you've got to be really worried about PE.”

During the 2010s it was relatively easy to make money as a PE shop. Low interest rates and buoyant markets meant firms could be confident of selling assets for more than they paid. But the buyout barons got carried away in 2020 and 2021, when borrowing became even cheaper and tech valuations went stratospheric as people worked from home.

Encouraged by the stellar returns previously enjoyed by software-focused PE firms such as Thoma Bravo and Vista Equity Partners, their peers piled in too: The tech industry made up almost a third of buyout deals in this period. Rather than prudently spread their investments over five years, some funds spent almost all their cash within a year or so.

Their timing was unfortunate, to put it mildly. Most PE firms weren’t aware of how profoundly artificial intelligence might upend software business models — OpenAI unveiled ChatGPT in November 2022. They were also caught out by the end of the cheap money era as central bankers hiked rates that year to quell inflation. That saddled scarcely profitable PE-owned companies with much higher interest payments because their loans are usually floating rate.

The private credit industry has experienced an abrupt and public comeuppance as retail investors have rushed to withdraw their money from funds that lent to these businesses. In contrast, the reckoning for the companies’ private equity owners is more of a slow-motion car crash happening largely out of sight.

While some PE firms are publicly listed, the businesses they own aren’t traded on stock markets and don’t disclose earnings. Investors in private equity funds often commit money for a decade or so and can’t get it back easily.

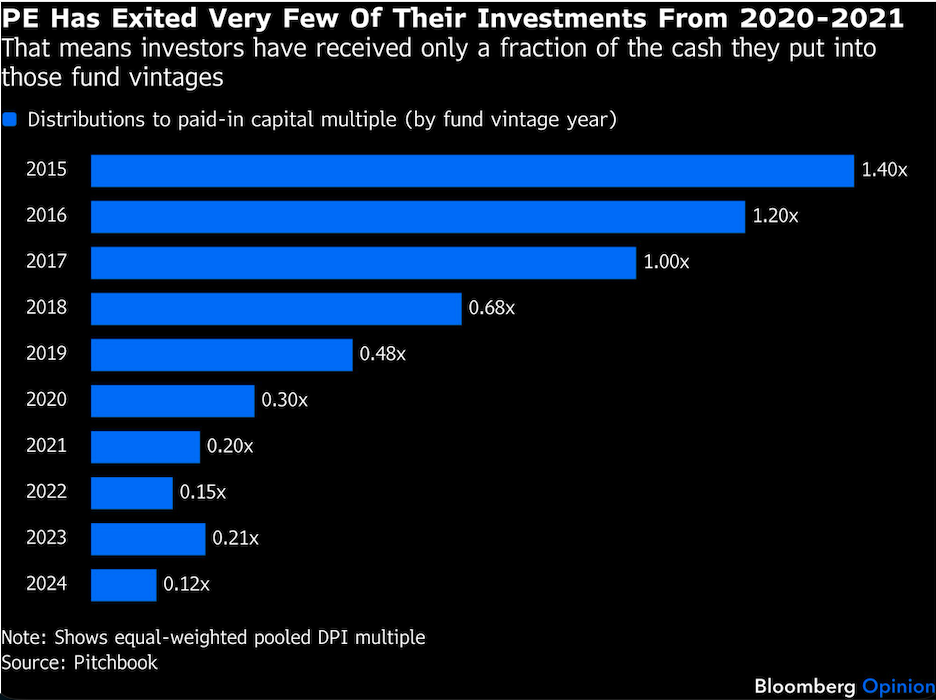

Even prior to the AI shock, PE firms were struggling to sell their more humdrum companies. The time between when assets are acquired and sold has extended to around seven years on average compared with five years or so in 2010, according to Bain & Co. This threatens to drag down returns.

In the absence of sales, PE firms have had to resort to alternative methods to make payouts to their investors, such as raising debt to fund dividends or effectively selling portfolio companies to themselves via “continuation funds.” This financial kicking the can down the road can’t go on forever.

Buyout firms can afford a few misses, so long as some assets in their portfolios are winners. The AI threat will take a while to crystalize and some mission-critical software should prove resilient. If portfolio companies can manage to increase earnings through cost-cutting and streamlining,

the broad decline in this sector’s valuations needn’t be disastrous.

The danger, though, is software companies becoming even harder to exit as the rise of Anthropic and its ilk makes buyers nervous. PE firms often sell stuff to each other but AI disruption fears could make lenders warier of backing such deals, warns Allianz Research. Furthermore, if these assets start being sold for much less than buyout groups anticipated, the paper gains they report to investors may need revising downward.

Another risk is that when a PE firm is stuck with a company that it can’t sell and whose valuation is in the doldrums, it will at some stage have to refinance its debt. Lenders may then tighten the screw as their loans will make up a much greater share of the business’s value than at the time of the buyout.

The PE owner may need to chip in more money to roll over the debt, warns Armen Panossian, co-CEO at Oaktree Capital Management. But they might not do so if a software business’s problems look terminal or if the buyout fund has already spent most of its cash.1

Recent strife at Medallia, a software firm taken private by Thoma Bravo for $6.4 billion in 2021, shows the sorts of difficulties awaiting PE firms, even though this company’s challenges predate AI fears. Medallia is struggling to keep up its interest payments. If its lenders end up taking control, Thoma Bravo and its co-investors risk losing the roughly $5 billion of equity they sank into the deal, Bloomberg reported this month.

A $17.8 billion Thoma Bravo fund that was partly used to acquire Medallia has a 6.2% net internal rate of return, according to data compiled from limited partner filings by Bloomberg. That puts its performance in the lowest quartile of funds from that troublesome 2020 vintage.

This ranking could improve if Thoma Bravo pulls off some decent exits, and the poor showing didn’t stop the firm raising an even bigger fund last year. Its co-founder and managing partner Orlando Bravo has said his investors are relieved because “for the most part our companies are crushing it” and “incredibly positioned” to be winners in the AI era.

For some PE managers, however, failing to profitably exit deals and return cash could mean the end. The last decade’s buyout boom bought a lot of loyalty from investors in this asset class, but the 2020-2021 vintage is threatening to spoil that. Will pension funds and life assurers be willing to pony up money for the next fund raising? If you think private credit has it bad, private equity probably has it worse.

1. PE firms sometimes resort to risky Net Asset Value loans to shore up portfolio companies, adding yet more leverage, only this time at the fund level.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Bryant