Will Private Credit Cause the Next GFC?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Believe it or not, it's been 18 years since the Global Financial Crisis (GFC). Despite many detailed investigative reports on the events and the popularity of the box-office hit and bestselling book “The Big Short,” the role of subprime mortgages in the near-fatal collapse of the banking system remains a mystery to many investors. As a result, some view recent rumblings in private credit as a precursor to a new financial crisis.

Given the misunderstanding linking subprime mortgages and private credit, I discuss how leverage and derivatives, layered atop subprime mortgages, were at the heart of the GFC. A better understanding of that event will help advisors and investors better assess whether recent woes in private credit are an omen of another crisis or an overstated concern.

When I started writing this article, I thought I would compare subprime mortgage securities and the GFC with the current situation in private credit funds. However, when writing about the causes of the 2008 subprime disaster, I thought this lesson on the dangers of leverage was important enough to merit a standalone article. Accordingly, this first part focuses on the GFC, while part two will describe the structural flaws of private credit and, importantly, explain why, on its own, it is highly unlikely to lead to another financial crisis like the GFC.

Subprime

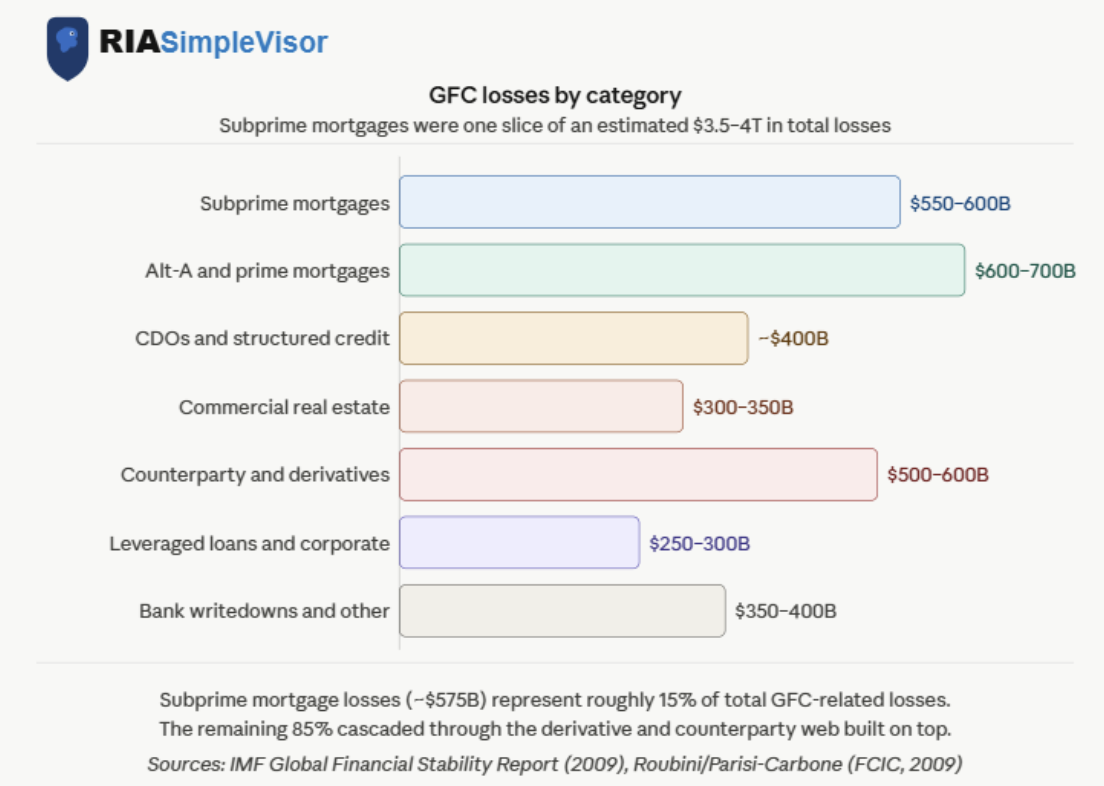

In the early to mid-2000s, leading up to the GFC, the amount of outstanding subprime loans grew rapidly to $1.3 trillion. At its worst, the estimated loss rate on these loans exceeded 40%. An approximate $600 billion loss is certainly significant, but it wasn’t nearly enough to bring the largest banks and brokers, and the entire global financial system, to its knees.

What made the GFC nearly catastrophic was the extraordinary web of leverage, complexity, and interconnected counterparty risk built around subprime loans. I share below that total GFC-related losses were estimated between $3.5 and $4.0 trillion — more than three times the losses that would have resulted if every single subprime loan had defaulted.

The Leverage Tree

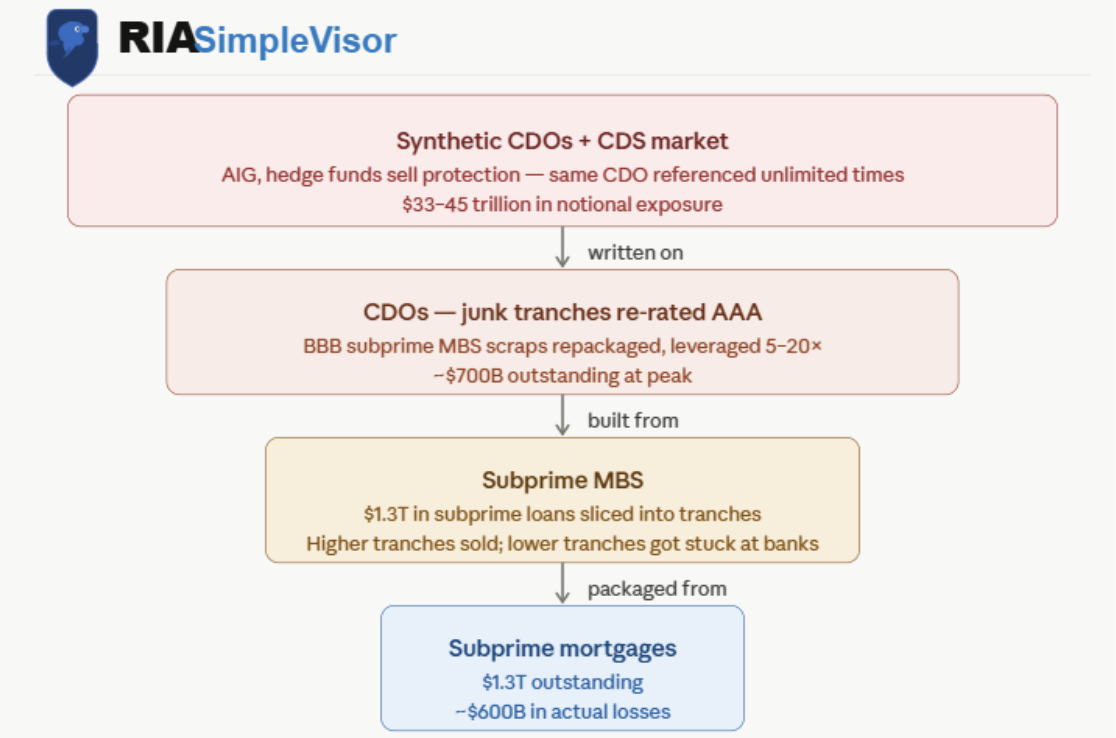

The relatively small subprime market was able to cause such devastation because of derivatives and the leverage built on subprime loans. Think of the GFC as a tree, with subprime loans as its roots. The tree started to grow when banks bought subprime loans and packaged them into mortgage-backed securities (MBS) with multiple tranches that divvied up the cash flows.

Subprime MBS investors in the AAA-rated tranches were repaid first, while the lowest tranches absorbed losses first and were repaid last. Yields varied with perceived risk. These structures attracted a wide array of buyers from the most conservative insurance companies to the most aggressive hedge funds.

Heading into 2006 and beyond, the losses on the underlying subprime loans were growing rapidly, and the lower-rated MBS tranches were quickly losing value. Because it was much easier to sell the higher-rated tranches, banks and brokers were typically stuck holding much of the lower-rated MBS. Given market conditions and mounting losses, they needed to sell them. Since there weren’t many willing buyers at the prices the sellers wanted, they created collateralized debt obligations (CDOs). The bank would take a bunch of lower-rated tranches from numerous MBS and repackage them into a new vehicle (CDOs), in which the cash flows were divided among tranches, as in the MBS.

Despite the poor quality of the underlying MBS tranches, the rating agencies assigned AAA ratings to the senior, first-pay tranches, fooling conservative investors into essentially buying junk-rated debt. Adding to the risk, hedge funds and other investors leveraged the CDO tranches five, 10, and sometimes 20 times over.

Even if the story ended here, the risks stemming from the original subprime loans were tremendous. But the story gets even crazier.

Synthetic Exposure

Investors’ appetite for the extra yield offered by subprime mortgages and CDOs could not be filled by the existing mortgages. Accordingly, Wall Street created synthetic CDOs.

While MBS and CDOs were backed by real cash flows of subprime mortgages, synthetic CDOs were backed by nothing. They used reference mortgages to determine the cash flows to and from investors.

The synthetic CDO seller, or issuer, collected premiums from investors who were buying protection to hedge their subprime mortgages or seeking to profit from subprime defaults. In exchange for receiving premiums, the issuers absorbed losses on the bonds referenced in the agreement.

Unlike a regular CDO, a synthetic CDO could reference the same CDO an unlimited number of times. If there were $100 million of a particular CDO in existence, $1 billion, $5 billion, or more synthetic CDO exposure could be written against it. For instance, if a homeowner defaulted on a $200,000 loan in Omaha, Nebraska, the issuers of synthetic CDOs could collectively lose $2 million, or much more in some cases.

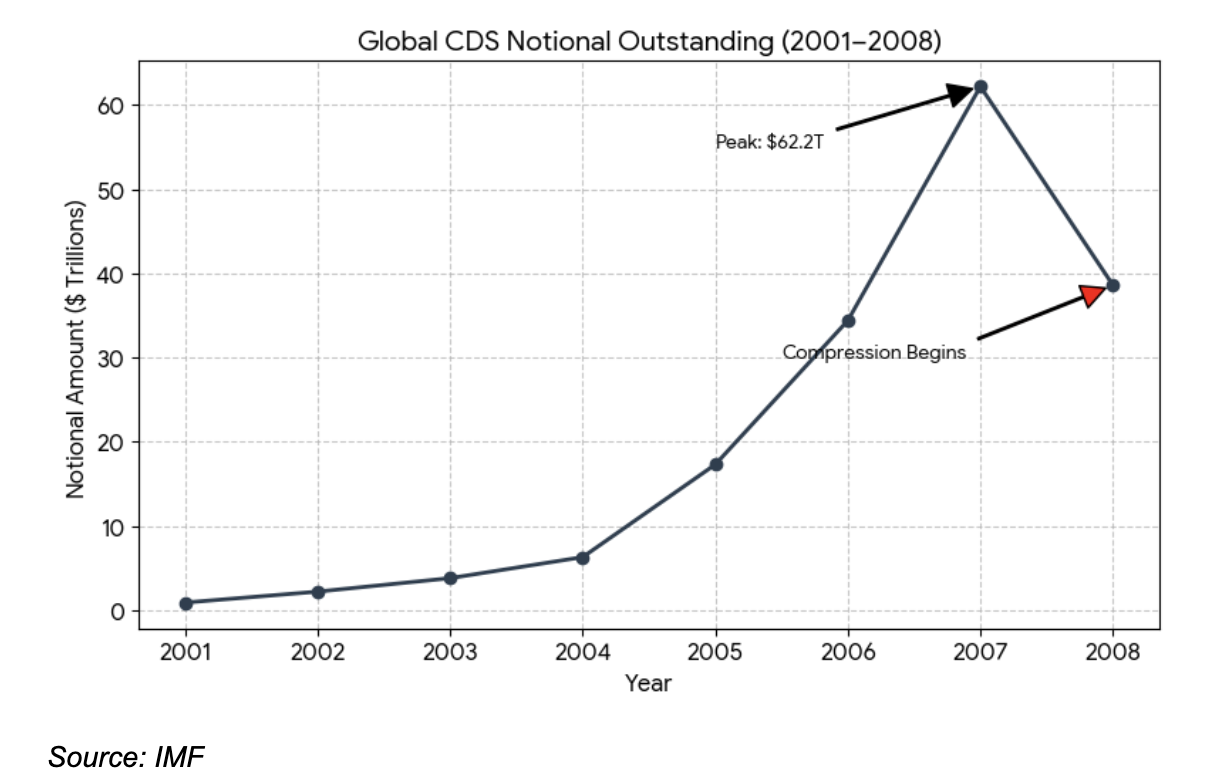

It has been estimated that there was between $33 trillion and $45 trillion in synthetic credit exposure, based on the cash flows of $1.3 trillion in subprime loans. The graph below shows the massive growth in CDS contracts leading up to the GFC. Note that synthetic CDOs accounted for a large share of the growth.

Trust Followed Defaults

When subprime defaults started to increase, losses weren’t the only problem. Equally important was a lack of trust among the largest financial institutions. Eroding confidence was most evident in the "boiler room” of the financial system: the overnight Fed Funds and repo markets.

These overnight loan markets ensure banks and brokers have ample daily liquidity to function. The biggest risk to the financial system is the concern that money lent today will not be repaid tomorrow. Once the rumors of losses started to grow, Wall Street questioned what its counterparties were on the hook for. Trust was lost, and the overnight repo markets seized up.

Lehman Brothers, which had survived the Great Depression, went bankrupt in one weekend. AIG, a large issuer of synthetic insurance, collapsed. Many of the world’s largest banks and brokers were on the brink of failure. The web of leverage and derivatives surrounding subprime mortgages was so tight that pulling on one thread unraveled the entire financial structure.

While it's fair to say that defaulting subprime borrowers were certainly the match, the bonfire, fueled by greed and irrational expectations, had been building for years.

------------------------------------------------------------------

Part Two: Private Credit, the Shadow System's First Stress Test

Over the past decade, as regulators forced banks to hold more capital and retreat from riskier lending, an alternative credit ecosystem has taken their place. Private credit funds, business development companies (BDCs), and specialty finance vehicles have filled the gap. By 2025, the private credit market had grown to an estimated $3.4 trillion globally. Unlike the various subprime securities and derivatives, which were largely owned by institutional investors, retail investors have been heavily involved in private credit. They were tempted with high yields and monthly or quarterly redemption windows.

The tremors started with the 2024 bankruptcies in the auto sector — Tricolor and First Brands. Then, Market Financial Solutions in the U.K. faced allegations of "serious irregularities.” The private credit fund Blue Owl gated withdrawals from a retail credit vehicle in early 2026. Ares Strategic Income Fund, with $10.7 billion under management, followed, capping redemptions at 5% despite withdrawal requests of nearly 12%. Apollo marked down assets in one of its BDCs and cut the payout. The list goes on.

Private Credit’s Structural Flaw

While defaults and collateral pledging irregularities are problematic, the headlines about gated funds are driving negative sentiment in the sectors. Currently, I do not think losses and defaults in the underlying loans are the problem. Rather, it's that a large number of inexperienced retail investors own the funds.

The fundamental problem in private credit is a mismatch. Private credit funds lend money over four- to five-year periods, but many offer investors quarterly or even monthly redemption windows. When redemptions spike, a fund cannot call its borrowers and get its money back. Its only option is to limit redemptions or sell the loans at a discount in a market that has few ready buyers for illiquid paper. Such forced selling drives prices down, which weighs on the net asset values (NAVs) of funds and triggers further redemption requests. More funds are gated, leading to worsening sentiment.

Compounding the problem is that over 25% of private credit loans are to software companies. As these companies' stock prices are affected by AI narratives, their credit investors get nervous and demand their money back.

This Isn’t 2008

Private credit today is a fancy term for direct lending. The fund makes a loan, holds it on the balance sheet, and bears the loss if it defaults. There are no synthetic CDOs replicating that exposure across the system. There are no insurance companies writing unhedged protection on private credit indices. The derivative structure that turned a manageable subprime loss problem into a global catastrophe simply does not exist in comparable form with private credit.

The risk today is more subtle. If negative private credit sentiment changes the behaviors of banks and other direct lenders, liquidity is comprised and credit creation weakens. This can manifest in economic weakness as it flows downstream to consumers and small businesses.

How Stress Travels: From Private Credit To Your Credit Card

The private credit ecosystem did not develop in a vacuum. Banks fed it. According to Federal Reserve data, bank loans to non-depository financial institutions reached $1.14 trillion in 2025. JPMorgan, Jefferies, and Fifth Third all disclosed losses tied to the auto-sector bankruptcies. When a private credit fund struggles, the losses surface on the balance sheets of the banks that provided the leverage to build it.

Now extend that chain one link further to consumer credit platforms.

Non-bank consumer lenders — marketplace lenders, fintech credit providers, buy-now-pay-later platforms, and specialty lenders serving borrowers below prime — are directly dependent on wholesale capital markets and institutional investor appetite to fund their loan books. When private credit investors experience losses, ask for redemptions, and pull back from new commitments, the appetite for purchasing consumer loan asset-backed securities (ABS) or providing warehouse lines to consumer lenders contracts sharply. The funding cost for that credit rises. Underwriting standards tighten. Credit becomes scarcer and more expensive for the consumer at the end of the chain.

When institutional investors retreat from risk assets, the first-order effect is on asset prices. The second-order effect — the one that actually damages the real economy — is on credit availability. Small businesses that borrow from direct lenders find their credit lines pulled or repriced. Consumers who rely on fintech lenders for personal loans or credit discover the tap has tightened. The capital that once flowed freely through the shadow banking system begins pooling behind closed gates.

Unlike 2008, when the Federal Reserve had a well-established playbook for supporting bank-centered markets, the regulatory infrastructure for addressing stress in non-bank finance is still being written.

The Fed's Uncomfortable Position

The Federal Reserve is not oblivious to this. In early 2025, minutes from an FOMC meeting revealed that several participants suggested halting or slowing balance sheet reduction amid concerns about liquidity conditions. It is worth asking whether that was a signal cloaked as a procedural footnote.

The Fed has intervened repeatedly in credit markets beyond its mandate — in 2008, in 2020, and arguably in 2023 during the regional banking crisis. It has a pattern of throwing its own rule book aside when financial stability is at stake.

If private credit stress spreads meaningfully to bank balance sheets or seizes up consumer lending markets, political pressure for Fed intervention will intensify. But the Fed backstopping a market built on years of aggressive lending creates its own moral hazard.

The Thread Worth Watching

We are not in 2008. The subprime crisis was larger and more deeply embedded in the core banking system. Private credit, for all its growth, remains a $3 trillion to $4 trillion market within a global financial system measured in the hundreds of trillions. Default rates, while rising, remain manageable at the aggregate level.

But manageability is a function of confidence, and confidence is a function of trust in valuations, liquidity, and counterparty integrity. All three are under pressure today. The marks on private credit portfolios are still largely self-reported, with limited secondary market verification. The redemption pressures are real and accelerating. And the interconnections between private lenders, banks, and ultimately consumer credit are deeper than the headline numbers suggest.

The lesson isn't that history repeats. It's that leverage, opacity, and interconnected risk have a way of transforming manageable losses into cascading crises.

Michael Lebowitz is a portfolio manager with RIA Advisors and author for Real Investment Advice. For more information, contact him at [email protected] or 301.466.1204.

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All