Billionaire money manager Bill Ackman is giving away a stake in his firm to investors who support his latest hedge-fund launch. This looks like a good deal. And so it should: If you’re selling a fund in the form of an initial public offering, you have to dangle the prospect of a quick buck.

Ackman is looking to raise $5 billion to $10 billion by selling shares in Pershing Square USA (PSUS), a New York-listed vehicle that will target large, high-quality North American companies. This will be more than just another bland big-cap equity fund. It will take occasional macroeconomic bets, for example via credit derivatives. With large positions and clout, PSUS will likely be able to influence the boardrooms of its portfolio companies without the expense of a takeover.

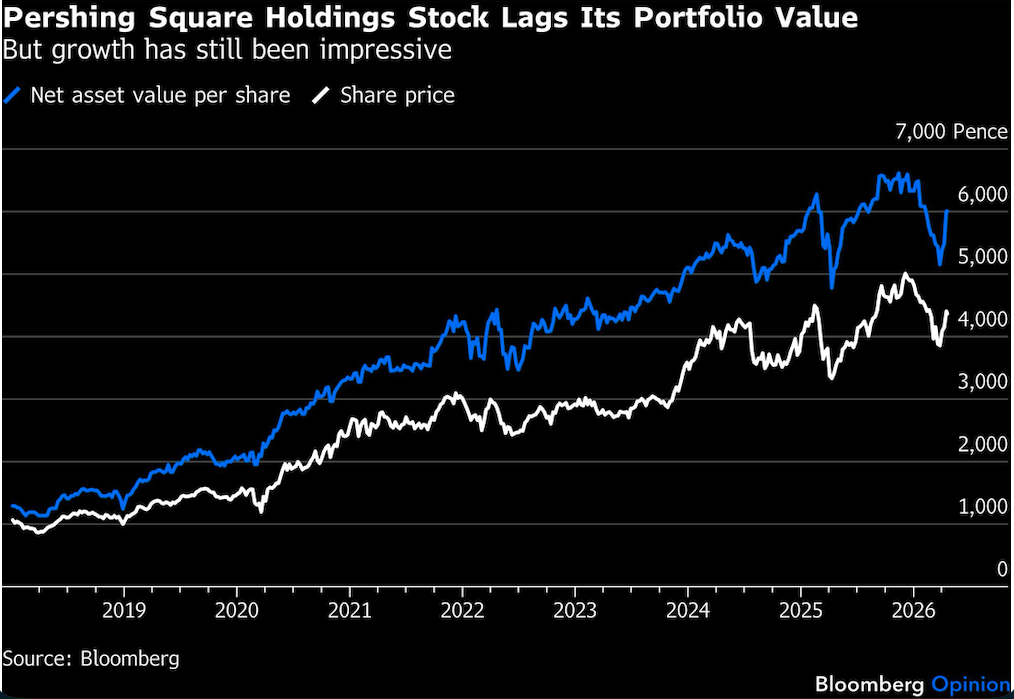

A London-listed forerunner, Pershing Square Holdings Ltd. (PSH), has grown its assets far faster than the S&P 500 index over the last eight years using this strategy.

It’s not all good. The question hanging over PSUS is whether it will imitate the unfortunate weakness that PSH’s stock price suffers versus the strength of its underlying asset value. That trading discount is currently almost 30%.

But PSUS won’t share some key PSH drawbacks, like restrictions on being marketed to US investors, nor the London fund’s onerous US tax treatment. Fees will be cheaper, too. Absent those drags, maybe PSUS will trade at a narrower discount to its net assets. If US investors lap up this rare chance to buy a listed hedge fund, might it even trade at a premium?

We won’t know until it lists. That’s the thing with IPOs: They have no stock-market history, and uncertainty over their trading dynamic is why buyers expect a sweetener. Hence new stock sales by companies are typically priced at a discount of 10% to 20% of the firm’s purported fair value.

It’s not so easy to embed such a discount for an investment fund, since it has no pre-existing assets. Ackman is offering an alternative carrot — one free share in his hedge fund manager, Pershing Square Inc., for every five bought in the fund IPO.

PSUS is being sold at $50 a share. Pershing Square itself was valued at $10.5 billion in a stake sale in 2024, equating to roughly $26 per share at today’s share count. Divide by five and the freebie is worth around $5 per PSUS share.

That historic valuation sounds high for a business that made net income of less than $300 million in 2025 and manages only $21 billion of fee-paying assets. Millennium Management, the multi-strategy hedge fund with $84 billion under management, was valued at $14 billion in a stake sale last year. Private equity firm Carlyle Group Inc., with nearly $340 billion of fee-paying assets, has a market value of $19 billion.

But a company is worth what someone is willing to pay for it. And there are reasons why the stake buyers would have put a high value on Ackman’s business. What matters is the resilience and profitability of assets under management, not just their size.

Most of the money Pershing Square manages is in vehicles with shareholders, who can’t make withdrawals from the fund and must sell their stock if they want to cash out. This “permanent capital” model means fee income is more reliable than even in the private capital sphere and Ackman will never be forced to sell assets to meet redemptions. Decent performance should then compound the assets over time.

In addition, Pershing Square’s fees on investment gains have an unusual degree of predictability. At PSH, it takes a cut of the first 5% of returns (after the management fee) and can recoup fees forgone in a bad year from gains in subsequent years. As long as PSH makes a compound 5% return over time, its long-term performance fees capture that.

How could Pershing Square be valued once it starts trading? It will list too; the market will set the price when the stock starts changing hands. One way into the question is to guess at the earnings it’ll be expected to make in 2027 assuming a successful PSUS launch.

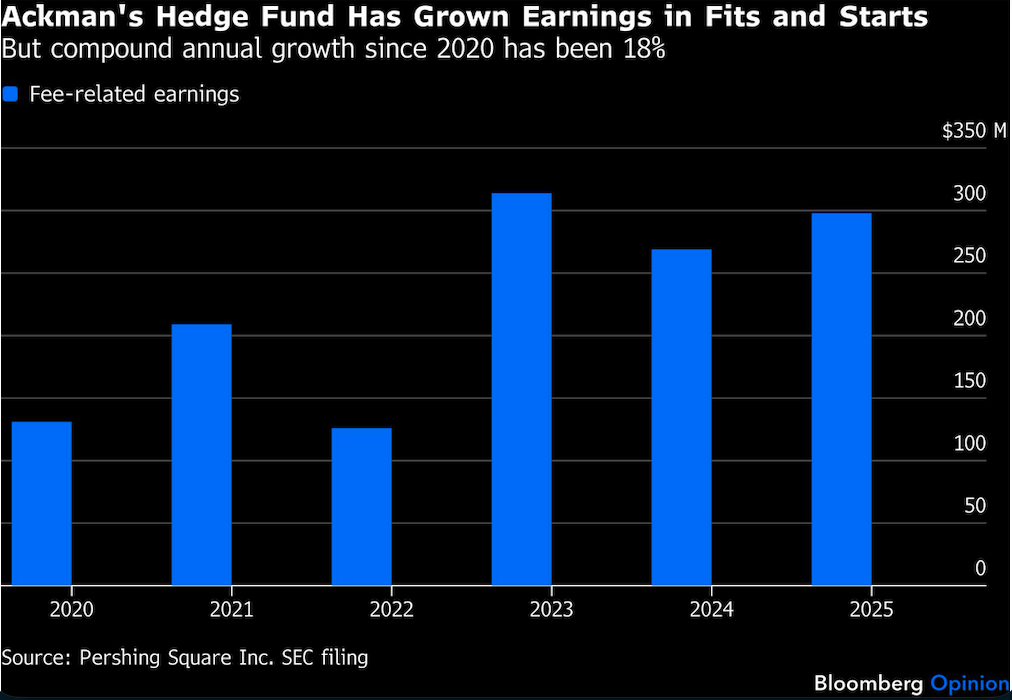

Last year, fee revenue was $343 million. Assume crudely that this base rises 15% to around $400 million driven by investment performance (Ackman’s long-run record is better). If a PSUS IPO raises its maximum target and grows afterwards, that could add a further $180 million in fees. Factor in a modest contribution from Howard Hughes Holdings Inc., Ackman’s new Berkshire Hathaway Inc.-style vehicle, and you’re looking at around $600 million of fee revenue.

Expenses would be low, perhaps only $50 million. There’d be tax too, but net income in the $400 million to $450 million ballpark wouldn’t be outlandish. On a 30 times multiple, the firm would then be worth around $14 billion (adding on a $600 million stake in Howard Hughes).

Perhaps that’s too low. On YouTube, Chief Investment Officer Ryan Israel last week drew attention to the fact that certain alternative asset managers commanded high-30s earnings multiples in 2025 amid rosy expectations for private credit. Pershing Square, he suggested, has the sort of growth potential investors were excited about back then, without the risk of the redemptions that private credit is seeing now.

Whether that sort of valuation can be achieved on day one remains to be seen. There’s a case for Pershing Square commanding a premium to the sector given its permanent capital. But industry multiples have come down a lot. Either way, the bonus shares are clearly valuable.

Ackman’s giveaway isn’t altruism. He needs to offer IPO investors a special deal for taking a punt on the new and to create a buzz for follow-on fund launches. And if the IPO market gives Ackman what he wants, he, as Pershing Square’s lead shareholder, will be the biggest winner.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.