Would you buy OpenAI’s shares even though the transaction might expose you to a liquidity crunch? SoftBank Group Corp.’s founder Masayoshi Son did just that.

OpenAI completed the largest funding round in Silicon Valley history last month, raising $122 billion ahead of a blockbuster public listing expected by the end of this year. SoftBank, already one of the ChatGPT maker’s largest shareholders, promised to put in $30 billion more.

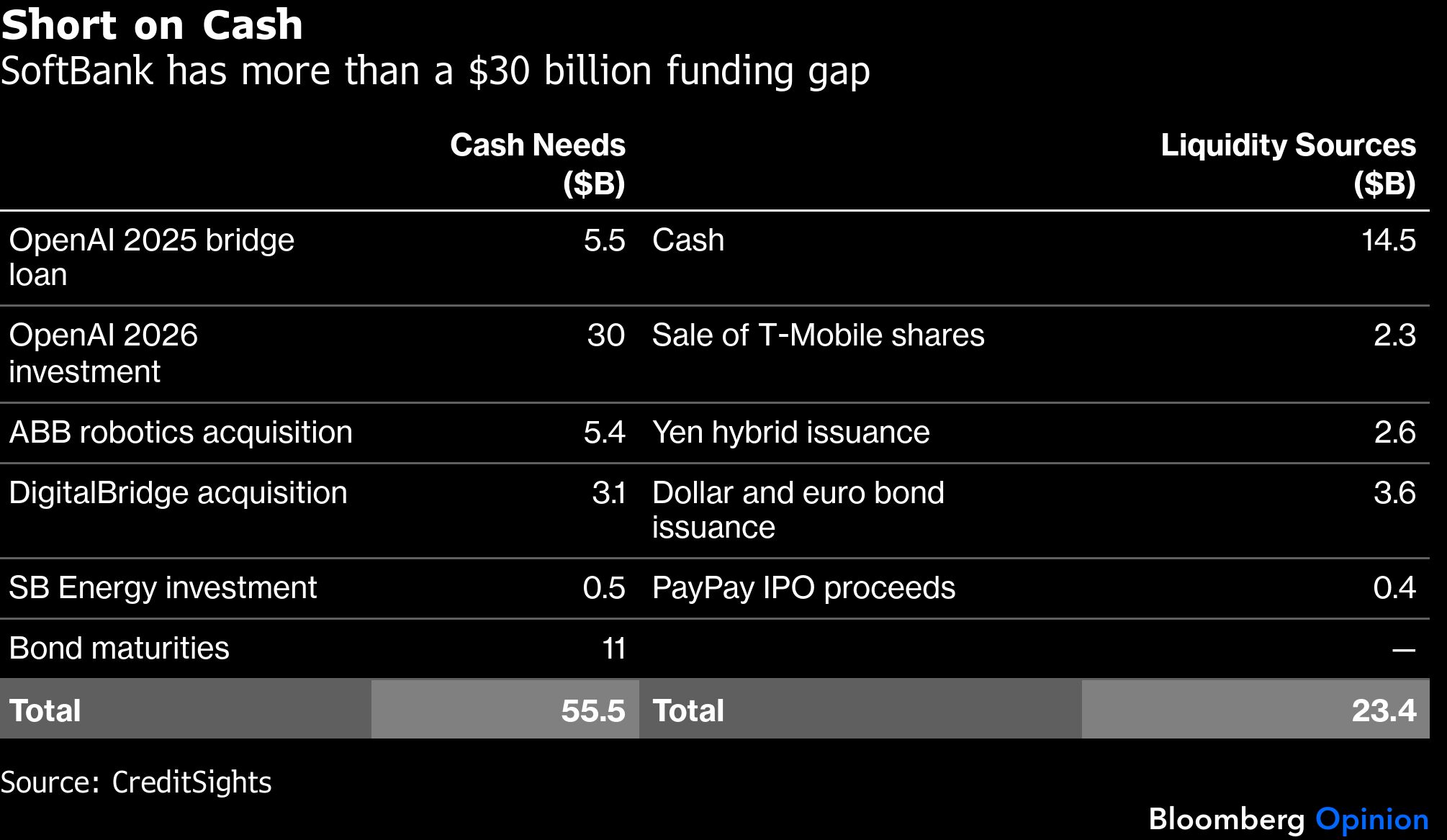

This funding round, on the heels of $30 billion invested in OpenAI last year, is stretching SoftBank’s balance sheet ever further. Based on estimates from research outlet CreditSights, the Japanese conglomerate is staring at a $32 billion funding shortfall, including bond maturities over the next two years and other investment deals the company has agreed to, such as a $5.4 billion acquisition of ABB Ltd.’s industrial robots unit.

As such, SoftBank recently signed a $40 billion bridge loan with banks to manage liquidity. This is a temporary solution, however, in that the jumbo debt will be due in a year.

Credit markets are puzzling over how Son plans to manage his company’s cash flow. Its 87% ownership in Arm Holdings Plc, worth about $150 billion, is by far the biggest asset. But since the chip designer’s stock has so little public float, it doesn’t serve as a good collateral. SoftBank might only be able to raise another $5 billion if it increases an Arm-backed margin loan, assuming a 20% loan-to-value ratio, according to Bloomberg Intelligence. Meanwhile, selling Arm shares outright can be tricky because the action might trigger stock slumps and margin calls.

There are other assets SoftBank could sell, including a possibly strategic $6 billion stake in Intel Corp. Unfortunately, Son already picked the low-hanging fruit last year when he wrote the first $30 billion check to Sam Altman’s startup, including by selling SoftBank’s entire stake in Nvidia Corp. Last week, SoftBank paid its highest interest rate on dollar notes as part of a $3.6 billion bond offering.

This is why an imminent OpenAI IPO is imperative to Son, not just to showcase his track record as a venture capitalist but to bridge his liquidity needs. Once OpenAI becomes a publicly listed company, SoftBank can sell some of its estimated $110 billion holdings or — if history is any guide — obtain margin loans using the ChatGPT maker’s shares as collateral.

Whether a blockbuster IPO can happen soon, however, is out of Son’s hands. Market conditions can change swiftly. Some early backers are already questioning the startup’s latest $852 billion valuation and calling it a “deeply unfocused” company.

This begs the question of why Son decided to make a follow-on investment. He’s done very well with the first $30 billion, which allowed him to buy into OpenAI at only a $260 billion pre-money valuation. Why did he choose to go big again, exposing SoftBank to a potential liquidity crunch?

One possible explanation is that SoftBank might have to serve as a meaningful cornerstone investor to anchor OpenAI’s sky-high valuation, especially since some retail investors participated in the latest funding round. The other two big backers — Nvidia and Amazon.com Inc. — may not come across as convincing because their investments could be interpreted as vendor financing. OpenAI will in turn use the proceeds to buybillions of dollars’ worth of AI chips from the two tech giants.

SoftBank certainly has an incentive to keep lifting OpenAI’s valuation. The company has already booked about $20 billion fair value gain from its OpenAI shares. With this latest valuation more than 70% higher than last October’s, SoftBank is on track for its second-most profitable year.

But these are only unrealized paper profits, which Son is essentially paying for with shaky liquidity management and higher borrowing costs. When OpenAI is ready to go public, does he have the financial means to guarantee a successful IPO?

There’s good reason to believe that OpenAI has reached peak valuation. Retail has been brought into the latest funding round, especially Cathie Wood’s ARK Investment Management, which topped Morningstar Inc.’s chart in wealth destruction. Son is once again partying too hard.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Shuli Ren