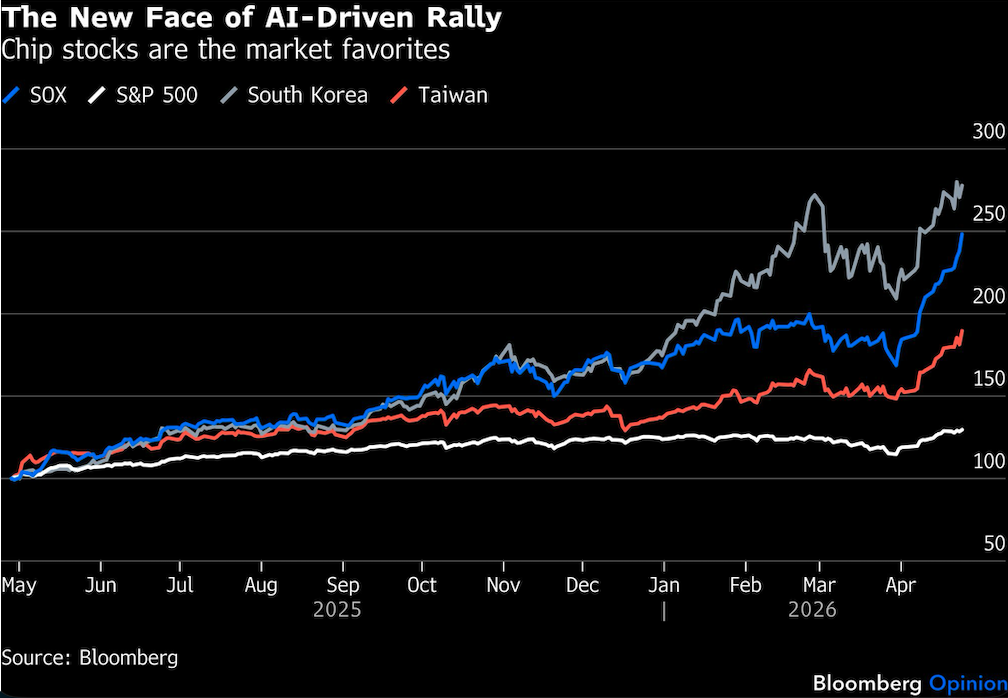

The chip industry seems to be the only game in town lately. The Philadelphia Semiconductor Index, known as the SOX, has risen 48% this year. Bourses in Taiwan, South Korea and Japan are riding the wave and hitting record highs, brushing away potential energy shocks from the military conflict over Iran.

Investors can’t get enough of the chips. The Roundhill Memory ETF, where three memory chip makers — SK Hynix Inc., Samsung Electronics Co. and Micron Technology Inc. — constitute about 65% of the total portfolio, came to market on April 2. It has already attracted $1.4 billion net inflows, a resounding success for the asset manager.

Some are now talking about an industry supercycle. As the focus of AI development moves from training large-language models to applications, the list of beneficiaries in the supply chain will broaden beyond Nvidia Corp. to those manufacturing central processing units, or CPUs, and memory chips, as well as equipment makers integral to the manufacturing process.

Unlike previous cycles, where end-demand was driven by consumer electronics, the ultimate clients this time are hyperscalers and cloud providers whose commitments might be more stable and long-term. With better earnings visibility, one can argue the industry deserves higher valuation. Indeed, since the arrival of ChatGPT in late 2022, SOX has largely traded at premium valuation to the S&P 500, bucking historic trends.

This earnings season has also given confidence to those who believe that suppliers hold all the cards. Hynix talked about excess demand over the next three years, while the world’s largest foundry, Taiwan Semiconductor Manufacturing Co., raised its full-year outlook. Of the six companies on SOX that have reported their first-quarter earnings, all have delivered pleasant surprises.

Still, while these are all healthy tailwinds, I wonder if investors are getting carried away.

My biggest concern is that the market seems to be rewarding every chip company, as if a healthy industry backdrop will lift all boats. But surely there will be winners and losers? Of the 30 stocks on SOX, only one company — Qualcomm Inc. — was in the red this year.

The rise of CPU chips is a good example. As we move to the agentic AI world with the arrival of applications such as OpenClaw — which serves as a personal digital assistant that manages your calendar and sends emails — industry analysts have suggested that in the future, data centers will need one CPU for every graphics processing unit deployed, versus one to four currently. The server CPU market can expand to $60 billion by 2030, up from $26 billion last year, according to Arm Holdings Plc. Last Friday, Intel Corp.’s shares jumped 24% on an earnings beat, lifting similarly focused companies such as Advanced Micro Devices Inc. and Arm.

However, the competitive landscape for CPUs used in data centers lacks clarity. Big companies are moving quickly to capitalize on it. Nvidia, best known for making powerful processors, launched Vera CPU in March, purposely-built for agentic AI. Days later, Arm, which traditionally makes money by licensing its CPU architecture to bigger companies like Nvidia, decided to make the chips itself. Meanwhile, AMD remains a formidable player.

Whether Intel or Arm can gain market share remains an important question. But investors have already gotten carried away. Intel is now valued at 54 times estimated 2027 earnings, while Arm, 87% owned by SoftBank Group Corp., trades at 109 times.

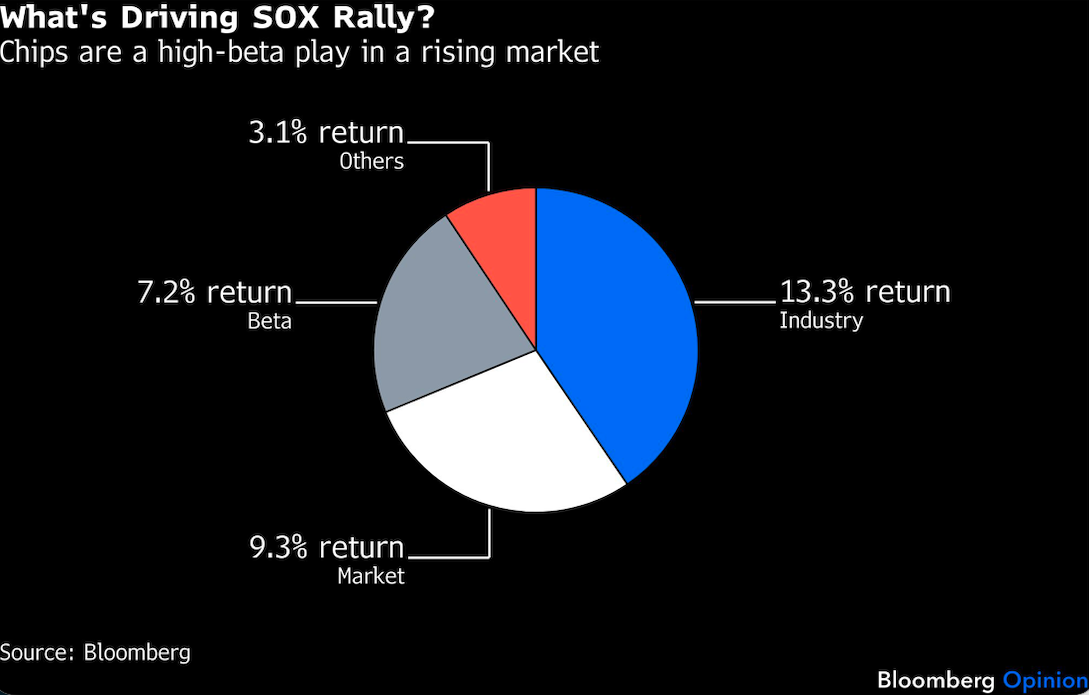

More likely, people are just chasing high-beta plays. Factor analysis shows that in April, chip stocks outperformed largely because of the broader market rebound. Believing that the TACO trade is still on, investors have rushed in to position themselves for the next phase of the AI-driven rally. Individual stock picking would not have mattered.

Ultimately, chip manufacturing is a complex process. You can have a huge pool but only a few fish are thriving — as Nvidia has shown with semiconductors used for training models. The fact that markets are positioned as if there are no losers in this game shows that willful blindness is on the rise.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Shuli Ren