For much of the past few years, US Treasuries have failed to serve their traditional role as a sure-fire refuge from global market meltdowns.

During the last three big ones — caused by the post-pandemic inflation shock, President Donald Trump’s tariff rollout and, more recently, his war on Iran — US government bonds offered little protection. In fact, each time they declined alongside risk assets like stocks. In 2022, Treasuries tumbled even more than the Dow Jones Industrial Average.

Inflation was the biggest culprit, since rising consumer and energy prices erode the value of debt payments that are locked in. And that’s kept key bond yields pinned well above where they were in late 2024, despite several interest-rate cuts from the Federal Reserve since then.

But the episodes shine a spotlight on a deeper, more permanent shift that analysts say is underway: the gradual erosion in recent years of what’s known as a “convenience yield” enjoyed by Treasuries.

Investors were traditionally willing to pay higher prices — and accept lower payouts — because of their liquidity, safety and usefulness as collateral. That, in turn, saved the government billions each year.

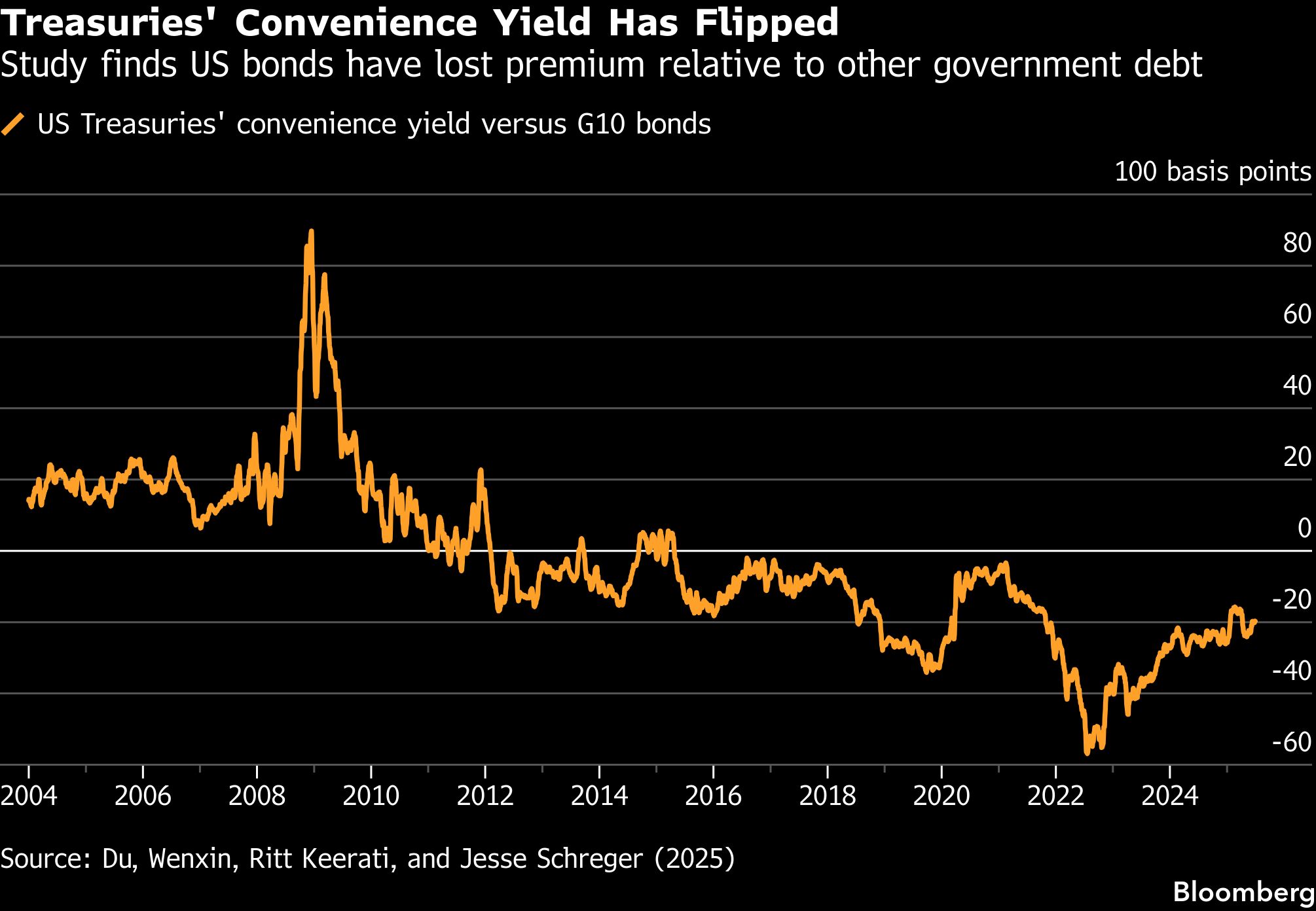

The premium, by all accounts, has fallen sharply or even disappeared. Estimates vary. But research by Wenxin Du, a Harvard professor and former Federal Reserve economist, suggests it has been reduced by nearly half a percentage point since the global financial crisis and is now negative when measured against currency-hedged debt from other major developed countries — meaning that Treasuries actually trade at a discount to their counterparts.

“One can argue bonds are less of a good hedge against risk,” said Du, who worked at the Fed from 2013 to 2018. “They’re just not your fly-to-safety assets because people don’t necessarily fly to them over crisis.”

Treasuries haven’t lost their privileged status at the heart of the global economy, of course, since no other bond market rivals its size. US government debt continues to be a pillar of diversified investment portfolios around the world. And Treasuries have outperformed many global peers since the US-Iran war started because the oil-price shock is expected to hit energy-importing countries particularly hard.

Moreover, despite speculation that Trump’s clashes with allies and go-it-alone approach would cause overseas investors to dump American assets, foreign holdings of Treasuries have continued to climb and are at record levels.

“Concerns about US debt are real and deserve attention,” said Lawrence Gillum, chief fixed-income strategist at LPL Financial. “But declarations of the end of Treasury exceptionalism remain, for now, exaggerated.”

Yet the massive increase in the government debt, according to researchers and the International Monetary Fund, has been ushering in a steady shift in the market. After Trump’s tax cuts and Covid-era stimulus, the amount of Treasuries circulating in financial markets has more than doubled over the past decade to roughly $31 trillion.

The amount held by the public was less than 40% of the US gross domestic product in 2008, according to the Congressional Budget Office. It’s projected to push over 100% this year and hit 120% a decade from now, surpassing the record levels seen during the World War II.

For every 10 percentage-point increase in the debt-to-GDP ratio, the Treasury market’s convenience yields decline by 4 to 9 basis points, according to a study by Du and her co-authors Ritt Keerati and Jesse Schreger published last year.

“The US Treasury used to be quite special,” said Du. “Then, since the global financial crisis, what you have seen is a secular decline in the Treasury premium. If there’s so much of something, it’s not really that special.”

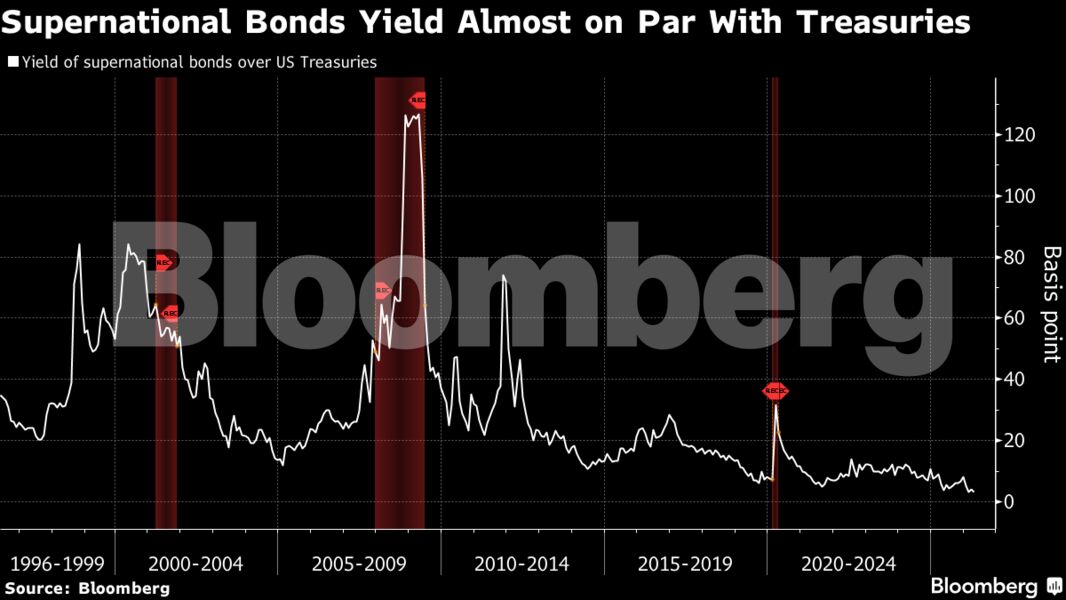

Other indicators point to a similar trend. The difference between the yields on US Treasuries and debt backed by top-rated supranational agencies, like the World Bank and the Asian Development Bank, has also virtually disappeared, data compiled by Blooomberg show. A decade ago, those institutions paid rates that were roughly 20 basis points more than what the US Treasury did. That has since shrunk to just 4 basis points.

“Investors, all else equal, are requiring more to own US Treasuries, particularly out the curve,” Gregory Peters, co-chief investment officer at PGIM Fixed Income, said on Bloomberg Television. The combination of large deficits and policy uncertainty “takes some of the shine off Treasuries,” he said.

At the same time, a shift in ownership is seen as likely to make Treasuries more volatile than in the past. Central banks — traditionally less sensitive to price — now own about 43% of Treasuries held by overseas investors, down from roughly 65% a decade ago.

Private buyers such as hedge funds, which demand higher compensation and are prone to leverage strategies that sometimes force them to dump assets during broader market turmoil, are playing a larger role.

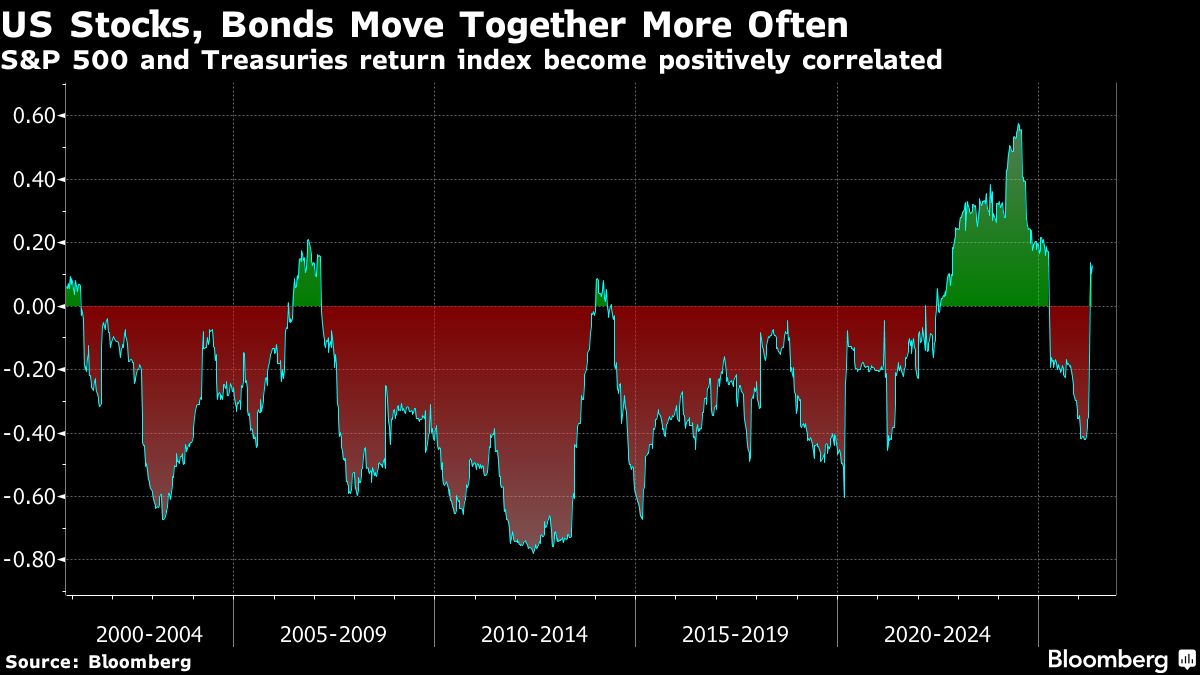

One consequence is that stocks and bonds have both been dragged down by shocks that upended markets in recent years. That marked a break from previous episodes — like the early 1990s recession, the dot.com bust, and the credit crisis — when Treasuries acted as a buffer by rising when stocks fell.

But the correlation between the two has been positive for much of the past four years, meaning they have tended to rise and fall at the same time.

Economists Viral Acharya and Toomas Laarits at New York University found that 10-year convenience yields declined sharply during last April’s tariff shock, which contributed to the simultaneous selloff in stock and bonds. That pattern happened again during the Iran conflict, with Treasuries initially sliding along with equities, then rebounding in tandem when the ceasefire buoyed hopes that the conflict was drawing toward an end.

Ed Al-Hussainy, a portfolio manager at Columbia Threadneedle Investments, said the disappearance of the Treasury convenience-yield premium has been most apparent in the longest-date bonds most exposed to the risks of the ballooning deficit.

To soften the impact, the Treasury Department has leaned more heavily on sales of short-term bills to finance its shortfalls. But that strategy requires more frequent issuance and increases vulnerability to shifts in market conditions and investor sentiment. Scott Bessent’s Treasury Department will unveil its quarterly borrowing plan on May 6.

“There are too many bonds out there relative to the level of demand,” Ed Al-Hussainy said.

Ed Al-Hussainy, a portfolio manager at Columbia Threadneedle Investments, said the disappearance of the Treasury convenience-yield premium has been most apparent in the longest-date bonds most exposed to the risks of the ballooning deficit.

To soften the impact, the Treasury Department has leaned more heavily on sales of short-term bills to finance its shortfalls. But that strategy requires more frequent issuance and increases vulnerability to shifts in market conditions and investor sentiment. Scott Bessent’s Treasury Department will unveil its quarterly borrowing plan on May 6.

“There are too many bonds out there relative to the level of demand,” Ed Al-Hussainy said.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.