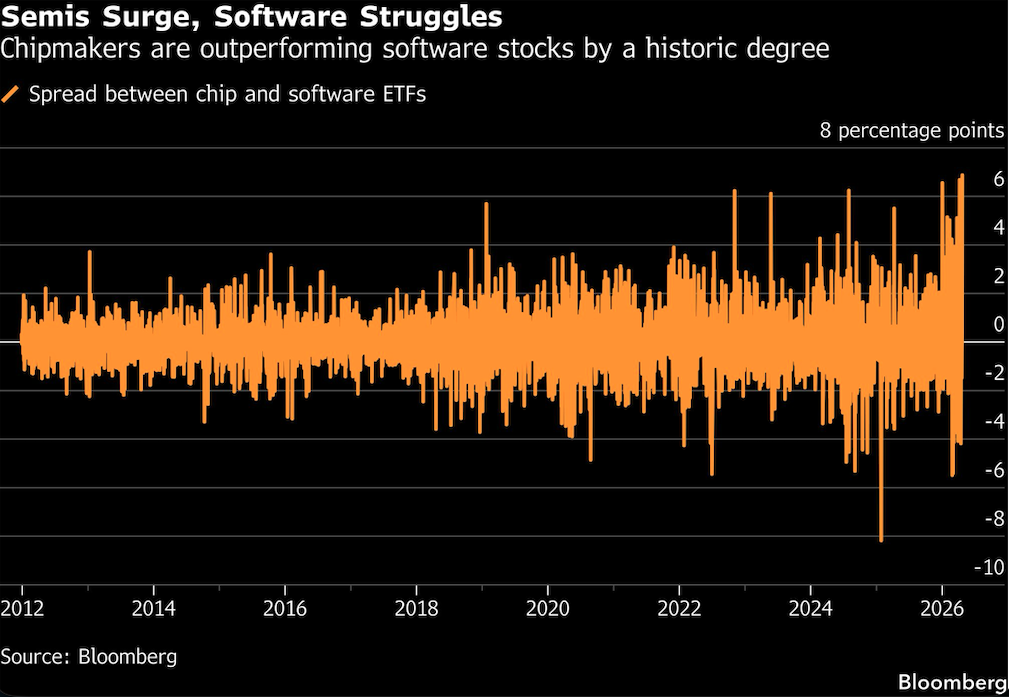

In a choppy year for tech investors, one trade has stood out as a success: buy chip stocks, sell software shares. And the divide between winners and losers is getting bigger as 2026 moves along.

“We’re likely i

n a new normal, where growth and margins for semis keep getting re-priced higher and growth and margins for software keep getting re-priced lower,” said Kevin Shea, senior equity strategist at BNY Wealth.

The two groups have charted decisively different paths in the stock market, as spending to develop artificial intelligence capabilities propels growth for semiconductor manufacturers, and the possibilities that AI presents imperil software providers at the same time.

The $58 billion VanEck Semiconductor ETF, or SMH, has been on a tear since the start of 2023, soaring almost 400% in that time, including a 32% jump this month alone. Meanwhile, the $11.5 billion iShares Expanded Tech Software ETF, or IGV is coming off its worst quarter since the 2008 financial crisis and is down 19% for the year.

“The divergence between the two looks rational,” Shea said. “It’s hard to see a significant re-rating for software where it gets back to where it used to trade relative to semis.”

The trade was on display last week when SMH leaped 9.1% while IGV was flat. On Thursday, the chips ETF rose 1.1% and the software fund sank 5.8%, the widest gap for a session in data going back to late 2011 — and the previous record was set earlier this month. Measured as a ratio, chipmakers are outperforming software this year by their widest margin on record.

Investors may see a reversal on Tuesday after a Wall Street Journal report that OpenAI failed to meet targets for sales and new users sent shares of AI-linked stocks tumbling. Chipmakers including Advanced Micro Devices Inc., Broadcom Inc. and Intel all fell more than 2.5% in early trading, while an ETF tracking the sector slid nearly 3%.

Last week’s moves came amid earnings reports that affirmed the narrative. Chip giant Texas Instruments Inc. gave a robust sales forecast as AI demand boosts spending on data centers, and the stock surged 19% for its best session since October 2000. That was followed a day later by blowout results from Intel Corp., which sent the stock flying 24% for its best day since 1987.

On the same afternoon as the Texas Instruments report, enterprise software maker ServiceNow Inc. posted results that fed into concerns about AI disruption, pushing the stock down 18% for its worst session ever. And an underwhelming performance by International Business Machines Corp.’s software business only added to the cautious tone.

“What earnings have shown is that semis and software are in very different environments,” Shea said. “There’s so much demand for chips and not enough supply, which means visibility is very different than for software, where it looks like it’s already harder for deals to close.”

Questioning the Divergence

The scale of the moves has some Wall Street pros wondering if the divergence is sustainable. Many software investors see the selloff in the group as indiscriminate and overdone. At the same time, the rally in the Philadelphia Stock Exchange Semiconductor Index, better known as the SOX, looks like something out of the dot-com era, according to Jonathan Krinsky, chief market technician at BTIG. Its 18-session winning streak through Friday was its longest ever, and it climbed 47% in that time.

The recent gain “is only exceeded by the move out of the Oct. ‘02 bottom, which came after an -80% bear market. So this is the biggest such move into a new high in the history of the semiconductor index,” Krinsky wrote in a note to clients Thursday. That stat, in addition to the degree to which the index is above its 200-day moving average, puts it in “extreme/unsustainable territory,” he wrote. “The window for a meaningful downside reversal is close.”

The run up has made chip stocks relatively expensive, with the SOX index trading at 23 times forward earnings compared with its 10-year average of 19. However, that multiple is hardly extreme considering the the tech-heavy Nasdaq 100 Index is also priced at 23 times forward earnings, and the S&P 500 Index is at 21 times.

Of course, investors are buying chip stocks because of the strong fundamental picture, not the price. Wall Street analysts expect semiconductor companies to post earnings growth of 35% in 2027, according to Bloomberg Intelligence data, a consensus that has risen dramatically since late January, when the projection was for 25.5%. Estimates have also been revised higher for revenue.

For software firms, on the other hand, earnings and revenue growth is expected to trail well behind semiconductors, and the consensus has only risen marginally in recent weeks. Yet, software stocks still look relatively expensive compared to chip stocks, with the S&P North American Expanded Technology Software Index is trading at 22 times forward earnings, a slight discount to the far better performing chips index.

“Everything has been feeding the narrative that companies will continue to spend on AI, which will lead to higher chip prices and better earnings and margins for semiconductor companies,” said Jordan Klein, a tech-sector specialist at Mizuho Securities. “At the same time, no one knows what the catalyst could be to reverse the AI overhang on software, let alone lead to better growth for the group.”

He expects investors to continue piling into what has worked and avoid what hasn’t.

“Hoping for a software recovery has been a disastrous trade, which has created the mindset of, this is not the time to buy on the hope we’ve bottomed,” Klein said. “Lately the only place you’ve been able to generate alpha in tech is in semis, which just feeds further gains. It’s a self-fulfilling narrative.”

Tech Chart of the Day

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.