The bond ETF industry is approaching $3.5 trillion in assets globally, and the fund managers running these exchange-traded funds would like you to know that bonds are back.

Yields are higher than they’ve been in a decade. Liquidity is deep. Active fixed-income ETFs pulled in more than $200 billion last year alone. The pitch, increasingly, is that bond ETFs are no longer a satellite holding to balance equity risk — they are the foundation of a modern portfolio.

There’s a lot of truth to this. The first generation of bond ETFs, tracking broad investment-grade indexes for fees of just 0.03 or 0.04 percentage point, are one of the great deals in finance. They did for retail bond investing what Vanguard Group Inc. did for equities: democratized access to a market that used to require a dealer relationship and a six-figure minimum.

But the part of the bond ETF complex that’s growing fastest isn’t that part. It’s the active and outcome-oriented funds — multisector strategies, flexible income vehicles, securitized credit funds, options-overlay products — that charge 0.30 to 1 percentage point and promise more yield, less duration, or both. And the marketing pitch behind them quietly elides something important. They aren’t really bond funds.

Consider the typical “multisector” active bond ETF, a category that has absorbed a substantial share of recent flows. Its yield looks attractive: well over 5% in many cases, against the four-and-change you get from a broad investment-grade index. Its duration is shorter, too, which sounds like a free lunch in a world where investors fear rising rates. How is the manager doing this?

He is doing it by buying things that aren’t really bonds in the way an investor sitting at a kitchen table thinks about bonds. The yield uplift comes from below-investment-grade credit, collateralized loan obligations, non-agency mortgages and emerging market debt. These are securities whose prices fall hard when equities fall hard — exactly when an investor most wants the bond sleeve to hold its value. They are, in useful shorthand, equity-light. You are paying a manager to take equity-shaped risk and put it in a wrapper labeled “bond fund.”

This isn’t a scandal. It’s a perfectly defensible portfolio construction, and the prospectuses say what they say. The problem is that the products are sold against a benchmark — the broad index — that is not equity-light, and against a category — fixed income — that has connoted safety in retail investors’ minds for 40 years.

A standard mean-variance optimizer — the textbook tool for choosing portfolio weights — fed the historical return and volatility of one of these funds will report low correlation with equities and recommend a hefty allocation. The optimizer is fooled by the wrapper. In stress, when correlations all run to one, the equity-light part of the bond sleeve is going to behave like equities, and the investor who bought it for ballast is going to be unpleasantly surprised, like the guy who gets a notice that his homeowner’s policy is cancelled while the hurricane is approaching.

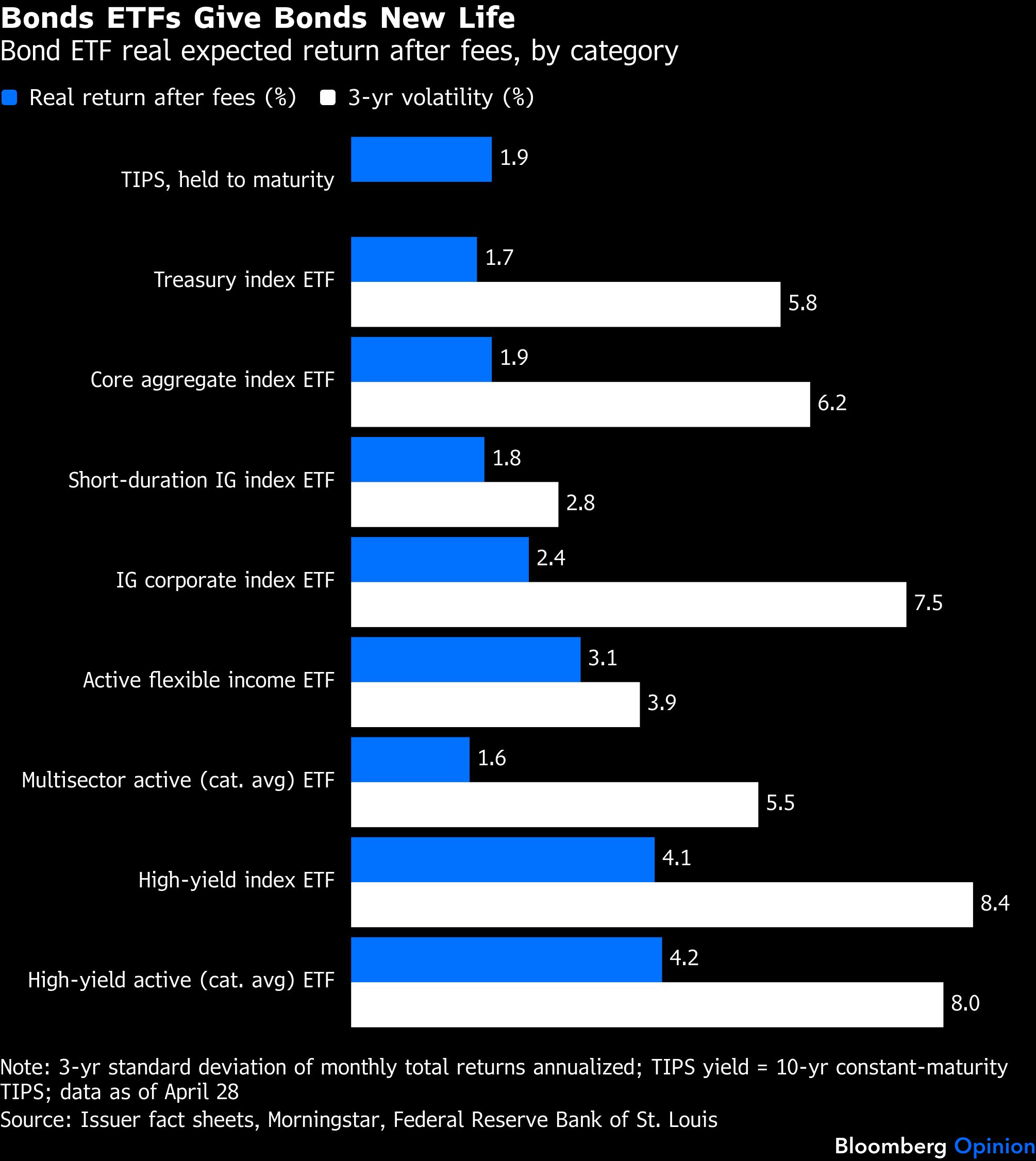

So that’s the first thing the bond ETF revolution forgot to mention: Many of the most popular new products are not really bonds in the conventional sense. The second thing has to do with the part of the complex that is really bonds — the cheap index ETFs. Here the issue isn’t a hidden risk; it’s arithmetic. The 30-day SEC yield on a broad investment-grade ETF is around 4.3%. Subtract roughly 2.4% of expected inflation, as the Treasury inflation-protected securities (TIPS) market is currently pricing it, and the real yield is about 1.9%. Subtract a 0.03 percentage point expense ratio and you get 1.87%. This is fine, but it’s also the cheapest version of the trade.

The same calculation applied to actively managed multi-sector products with expense ratios of 0.40 to 1 percentage point take the real yield down by 20% to 50%. Against thin real yields, fees that look small in nominal terms become large in real terms. A 1% fee on a 5% nominal yield is a fifth of the gross. The same 1% fee on a 1.5% real yield is two-thirds. This is a structural feature of the current rate environment, not a critique of any particular product. When real yields are thin, fees matter much more than they did when yields were thicker. The industry talks about its products in nominal terms; investors live in real terms.

If what an investor wants out of the bond sleeve of a portfolio is what bonds were originally supposed to provide — protection of purchasing power, low correlation with equities, freedom from manager risk — there is a way to get exactly that, with no expense ratio and no mark-to-model anything. It’s called Treasury Direct. The US Treasury sells inflation-protected securities directly to retail buyers at auction, and a TIPS held to maturity earns its real yield with no principal volatility and no fee.

The most recent five-year TIPS auction cleared at a real yield of about 1.4%. The 10-year is yielding around 1.9% in real terms. An investor who builds a small TIPS ladder in a Treasury Direct account is, for the safe sleeve of a portfolio, capturing essentially the entire real yield the market is offering, with no intermediary taking a cut. What the investor gives up is liquidity, so this is an option for medium and long-term allocations, not a cash-substitute.

For investors looking for a cash substitute, short- and medium-term investment grade bond ETFs can be higher-yielding alternatives to money-market funds. The trade-off is the risk. Money you need for end-of-the-month rent should be in money markets, but emergency reserve cash or money being saved for house down payments might find such a bond ETF preferable. This is the part of bond investing that hasn’t changed. It is also the part the new products are competing against, even if the comparison rarely appears in the marketing materials.

Investors who want the sophistication of an actively managed credit portfolio can certainly buy one, and many should. Investors who want what their parents thought they were buying when they bought “bonds” can do that too. They just need to know the difference.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Aaron Brown