Sometimes small changes speak loudly. Deutsche Bank AG’s new chief financial officer, Raja Akram, put the German lender’s consumer and asset management businesses before its corporate and investment banking units in his first earnings presentation last week. Akram, who joined from Morgan Stanley last year, wants Deutsche Bank to earn a smaller share of its profit from trading and dealmaking.

The shift highlights an important message not only for Germany but Europe as a whole: The region’s big lenders are all limiting how big they want to be in investment banking. Europeans have spent years strengthening their balance sheets and rebuilding profitability, and there had been some hopes that they might start retaking market share from their American rivals. But Wall Street firms are getting more competitive, helped by a White House hot for deregulation, and they’re going to increase their dominance of the industry everywhere.

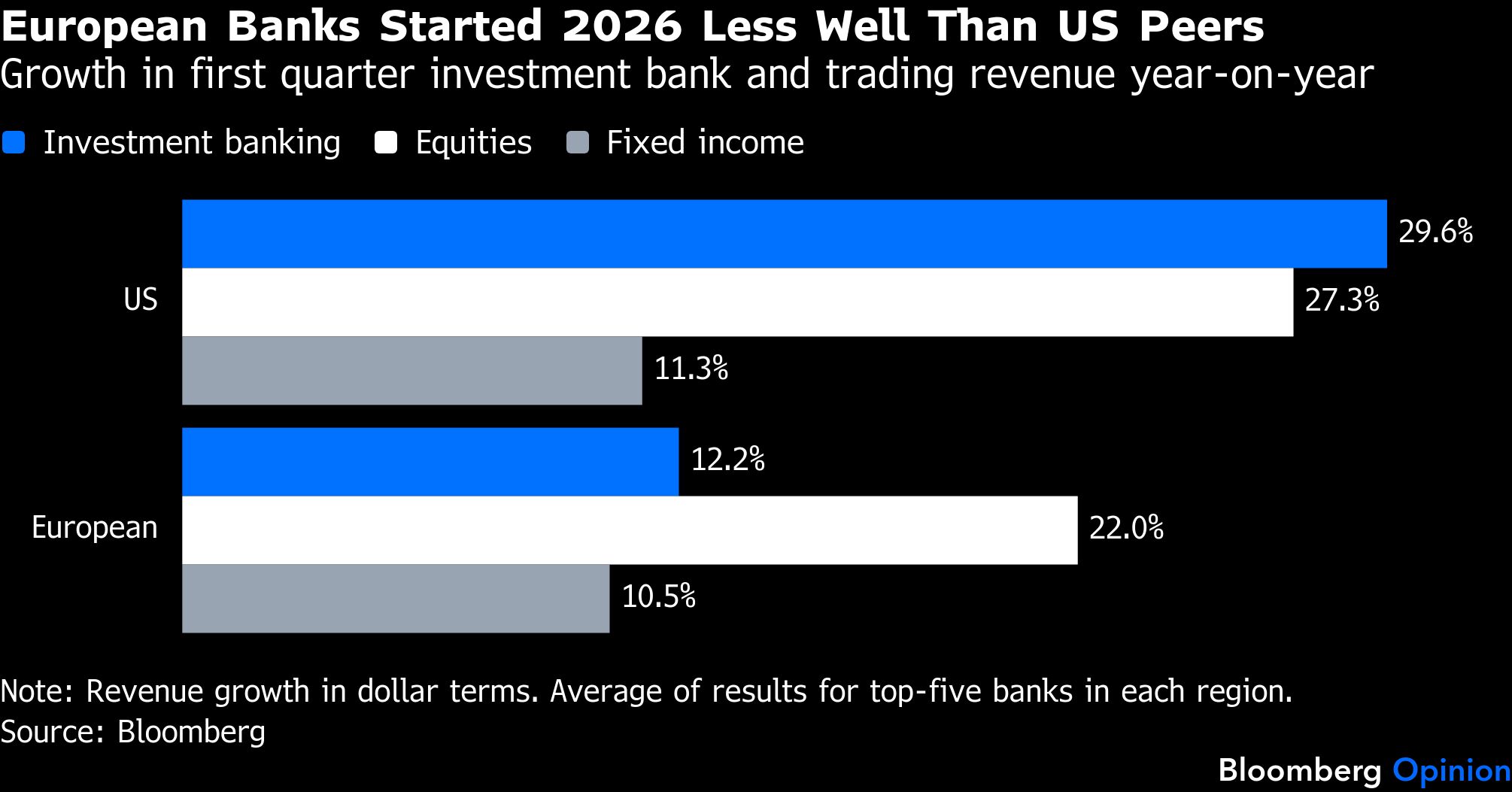

To be fair, European banks did well out of a volatile first quarter in financial markets, reporting good trading and investment banking results in most areas. But they still underperformed their US peers on average. The biggest gap was in dealmaking and fundraising for companies, where the five biggest Wall Street firms lifted first-quarter fees by 30% on average compared with the same period last year; the five leading Europeans grew by just 12% in dollar terms.

Averages smother a lot of detail, of course, and there are differences in what US and European banks do. For instance, most Europeans don’t do much trading in commodities, and the war in Iran has generated a lot of action there. Also, they mainly don’t have a very big presence in US markets. But the ceiling on European ambitions is real.

Barclays Plc is trying to reduce the amount of capital that its investment bank takes up to below 50% of the group’s total — it currently sits at 55%. It’s trying to rebalance by expanding everything else rather than shrinking the markets and advisory arms in absolute terms. But its bankers need to work much harder to justify every bit of balance sheet they want to use than they did in the past.

UBS Group AG, too, has capped the total share of risk-weighted assets within the bank at 25% and is enforcing tight discipline on what traders and investment bankers can do. It might have to get even more strict if the Swiss government pushes through a threatened big increase in capital demands. BNP Paribas SA of France has only about one-third of its capital in its corporate and investment bank and, although it doesn’t have a formal limit, it doesn’t expect that to increase. Societe Generale SA, which has been going through a long strategic overhaul, has also focused on growth outside its investment bank.

The change in tone at Deutsche Bank may be subtle, but it matters. Its fund management and wealth businesses are where it wants to invest and expand — which is perhaps unsurprising under a finance chief who came from Morgan Stanley, the firm that most successfully made that strategic pivot in the years following the 2008 financial crisis. In the first quarter, trading and dealmaking contributed less than half of Deutsche Bank’s pretax profits versus almost 55% in the same period last year. That’s a shift Akram wants to build on.

It’s not going to be a revolution, and the German bank isn’t going to turn into an entirely different beast over the years ahead; big corporate clients still matter, especially in Germany. But it is further confirmation that each of the big European investment banks has narrowed its focus and will only attempt to do certain kinds of business with particular clients.

Deutsche Bank Chief Executive Officer Christian Sewing said he wasn’t worried about increased US competition, even as the White House pushes for further deregulation that will allow American firms to be more aggressive. “Obviously, I can see that there may be an advantage on the US side from a capital point of view, from a balance sheet expansion,” he said on Wednesday’s earnings call. “And in this geopolitical situation … our clients around the world would like to have a European bank at the table, and this is exactly where we see our opportunity.”

This is a common refrain: Each European bank sees a role for itself among the handful of American banks working on any given deal, because lots of clients want at least one non-US advisor around.

UBS CEO Sergio Ermotti also highlighted the increasing power of US banks to compete given the easing of rules they’re getting from regulators. “It's fair to say that the US banks have a fair bit of dry powder when it comes to capital deployment,” he said last week. “We're competing really well in the investment bank sectors in which we're choosing to play. We recognize the fierce competition, but we like our chances.”

Focus is admirable. In the past, European banks have taken themselves to the verge of ruin — and sometimes beyond — when going up against the Americans in US markets. Being smaller, nimbler and more focused on reliable interest income and money-management fees is also what investors want from these banks. Local regulators also remain wary of too much dollar-denominated risk inside European lenders.

The individual strategic choices all make sense, but in the longer term they’ll leave European companies ever more reliant on US banks for access to capital markets. None of this is going to help Europe and the UK develop deeper and more liquid capital markets of their own. That isn’t a healthy direction of travel.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Paul Davies