Financial planning is one of a multitude of reasons investors seek the help of a financial professional. Learn how SmartAsset AMP can connect you with prospective clients.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Opening a 529 plan is a tax-advantaged way to set aside money for college. The money you contribute can grow tax-deferred and qualified withdrawals are tax-free. While there is no federal tax break for making 529 plan contributions, you may be able to claim one at the state level. Breaking down the 529 tax deduction by state can give you an idea of how you might be able to benefit when saving for college. Need help creating a college savings plan? Get connected with a financial advisor to learn more.

Understanding 529 Plan Tax Deductions

Tax deductions are amounts that reduce your taxable income for the year. You can claim both federal and state tax deductions. They’re different from tax credits, which reduce your tax liability on a dollar-for-dollar basis.

Claiming tax deductions can help you pay less in taxes or garner a bigger refund if you typically get money back at the state or federal level. Some deductions are above the line, while others require you to itemize on your tax return. Credits, meanwhile, lower your tax bill.

The federal government offers some tax deductions for education, but a deduction for 529 plan contributions isn’t one of them. You can, however, deduct interest paid to student loans. The American Opportunity Tax Credit and the Lifetime Learning Tax Credit can also be claimed to offset higher education expenses.

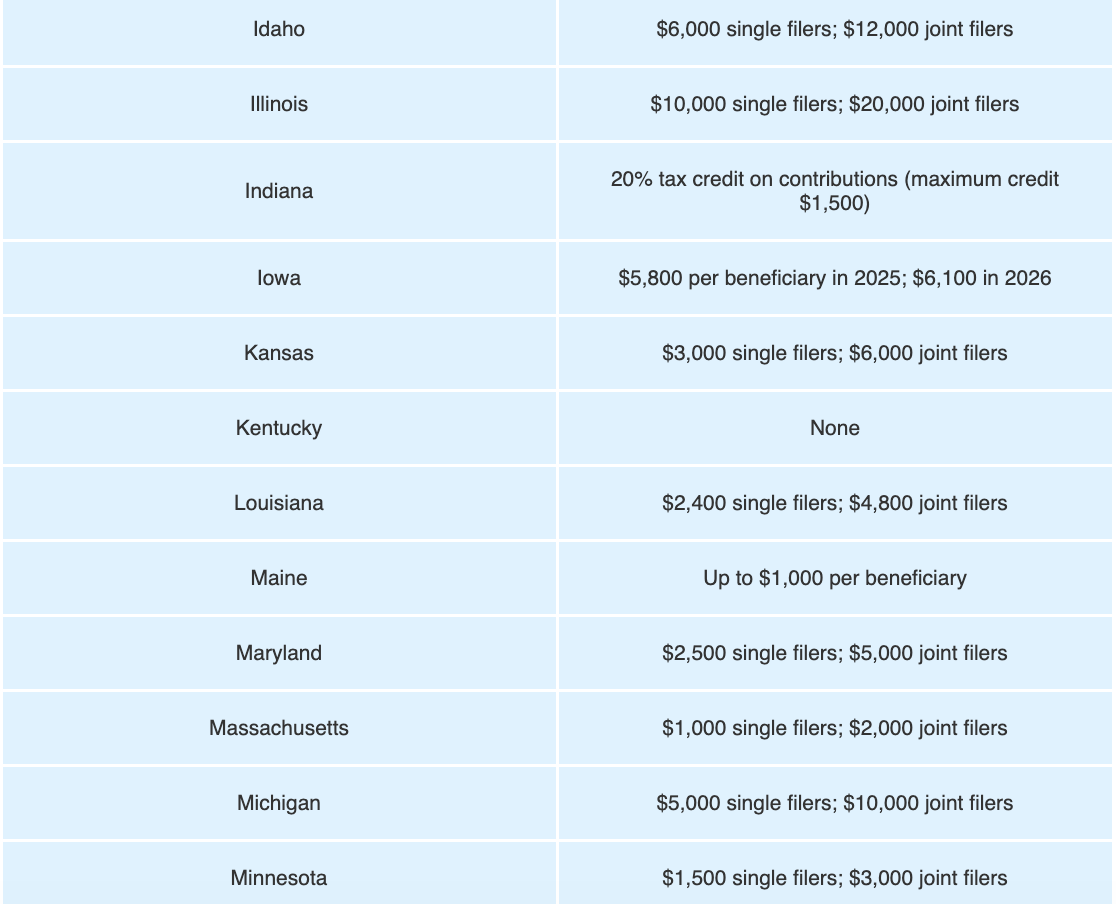

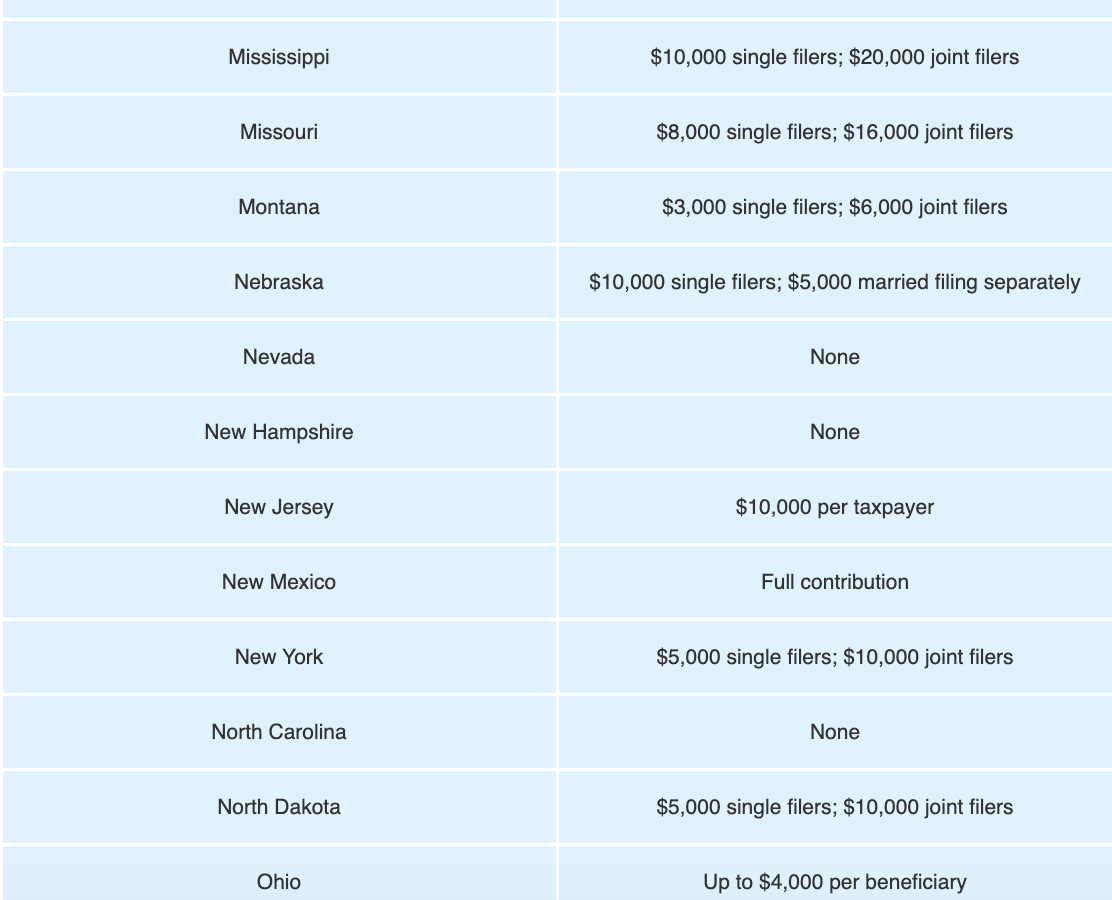

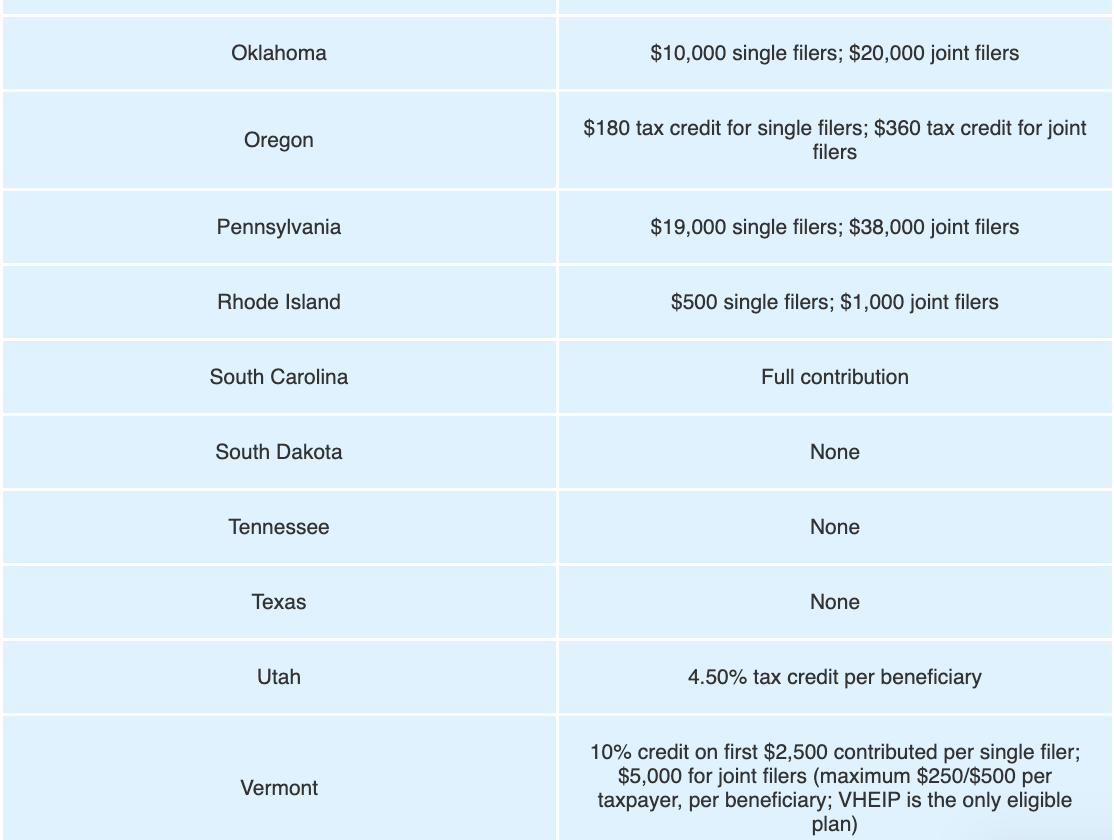

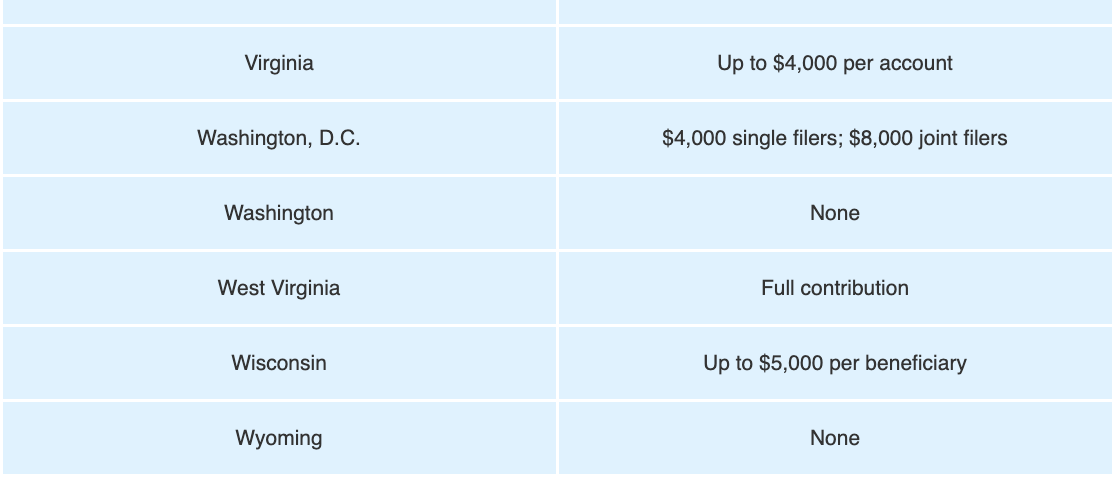

529 Tax Deduction by State

Every state offers at least one 529 plan, but states are not required to offer a tax deduction or other tax breaks for education. That being said, many states do offer deductions if you’re making contributions to a 529 plan. States can also offer credits or other tax breaks as an incentive to save for college.

Nine states do not have income tax, which means they don’t offer a 529 plan deduction. Those states are Alaska, Florida, New Hampshire, Nevada, South Dakota, Tennessee, Texas, Washington and Wyoming. California, Hawaii and Kentucky do not offer any type of 529 tax deduction but do assess income tax.

This table breaks down the 529 tax deduction by state.

Claiming 529 Plan Tax Benefits

To claim a tax deduction or credit for 529 plan contributions, you must live and file taxes in a state that offers these benefits. You must also be eligible to get a tax break, based on your relationship with the account beneficiary.

In most states, any contributor to a 529 plan can claim a tax break, regardless of whether they’re the account owner or not. However, some states limit tax benefits to account owners only. That means grandparents, aunts and uncles or other contributors would be excluded from deducting contributions or claiming tax credits.

The good news is that there are no time limits on claiming state-level tax benefits associated with a 529 college savings plan if you’re eligible to do so. Unlike Coverdell Education Savings Accounts (ESAs), which require you to withdraw all assets once the beneficiary turns 30, 529 plan money can stay in the account indefinitely. So, as long as you’re making contributions you could still claim a deduction or tax credit if you’re eligible.

Is Contributing to a 529 College Savings Plan Worth It?

Saving money in a 529 plan can be worth it for a few reasons, starting with the laundry list of tax breaks they offer. Contributions grow on a tax-deferred basis, so you’re not having to pay tax on any earnings while the money is in the account. Any qualified withdrawals are tax-free, as long as you use them for eligible higher education expenses. Under a provision of the One Big Beautiful Bill Act signed into law in July 2025, you can now withdraw up to $20,000 without a tax penalty in 2026 to pay for qualified expenses for grades K-12 (up from $10,000 in 2025).

You can open a 529 plan and contribute money to it on behalf of any eligible beneficiary, including yourself or your spouse. Should your beneficiary decide not to go to college or if they don’t use up all of their savings, you could transfer the money to a different beneficiary. As outlined in the table above, some states offer tax breaks for college savings in the form of deductions or credits.

Aside from those benefits, a 529 plan can offer a better rate of return on your money compared to keeping money in a high-yield savings account or even a CD. They also allow for more flexibility than savings bonds. And while you could tap into an individual retirement account (IRA) to pay for college, that could shortchange your retirement savings and potentially trigger some tax consequences.

Bottom Line

Getting a head start on college planning can help you to be better prepared when it’s time for your student to head off to school. Saving money in a 529 plan can benefit you at tax time and your money may have more room to grow than it would sitting in a bank account. Reviewing your 529 tax deduction by state can help you figure out how much of an additional tax advantage you might get from saving.

Financial Planning Tips

- If you’re ready to start saving for college but you don’t know how to approach it, getting professional advice can help. A financial advisor can walk you through different college savings options so you can choose the one that best fits your needs and situation. Finding a financial advisor doesn’t need to be hard. SmartAsset’s free tool matches you with vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- When comparing 529 savings plans, remember that you’re not locked into choosing your state’s plan. You could invest in a different state’s plan if you prefer the range of investment options offered or if another plan allows for higher lifetime contribution limits. Keep in mind, however, that your choice of plan may affect your ability to deduct those contributions on your state income tax return.

Rebecca Lake is a retirement, investing and estate planning expert who has been writing about personal finance for a decade. Her expertise in the finance niche also extends to home buying, credit cards, banking and small business. She's worked directly with several major financial and insurance brands, including Citibank, Discover and AIG and her writing has appeared online at U.S. News and World Report, CreditCards.com and Investopedia. Rebecca is a graduate of the University of South Carolina and she also attended Charleston Southern University as a graduate student. Originally from central Virginia, she now lives on the North Carolina coast along with her two children. Rebecca also holds the Certified Educator in Personal Finance (CEPF®) designation.

SmartAsset Advisors, LLC ("SmartAsset"), a wholly owned subsidiary of Financial Insight Technology, is registered with the U.S. Securities and Exchange Commission as an investment adviser. SmartAsset's services are limited to referring users to third party advisers registered or chartered as fiduciaries ("Adviser(s)") with a regulatory body in the United States that have elected to participate in our matching platform based on information gathered from users through our online questionnaire. SmartAsset receives compensation from Advisers for our services. SmartAsset does not review the ongoing performance of any Adviser, participate in the management of any user's account by an Adviser or provide advice regarding specific investments.

We do not manage client funds or hold custody of assets, we help users connect with relevant financial advisors.

This is not an offer to buy or sell any security or interest. All investing involves risk, including loss of principal. Working with an adviser may come with potential downsides, such as payment of fees (which will reduce returns). Past performance is not a guarantee of future results. There are no guarantees that working with an adviser will yield positive returns. The existence of a fiduciary duty does not prevent the rise of potential conflicts of interest.

SmartAdvisor helps qualified financial advisors build meaningful relationships directly with mass-affluent consumers who are actively searching for financial advice. Learn more about how our platform can help grow your practice.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more articles by Rebecca Lake