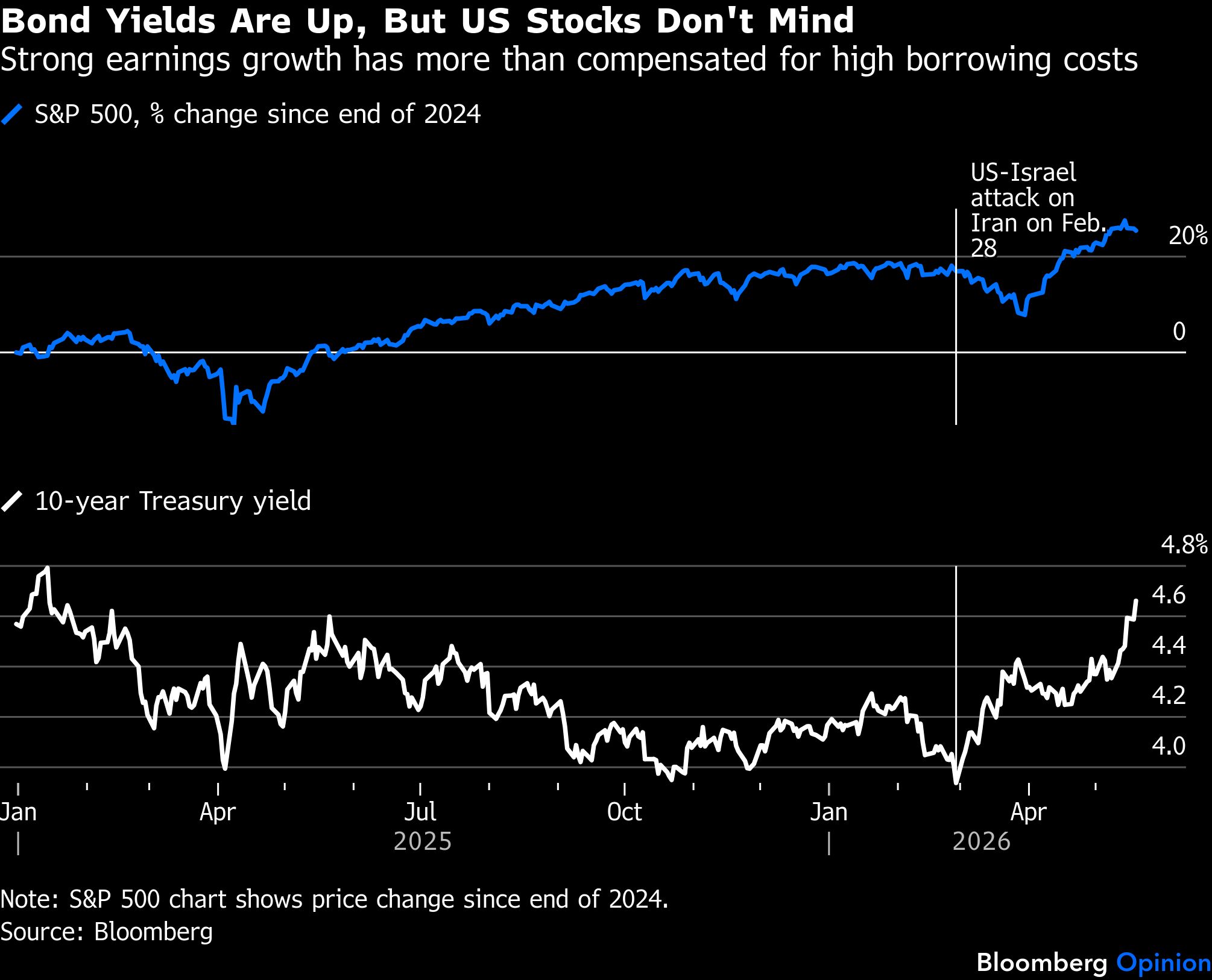

There’s a whiff of panic among investors these days. US Treasury yields have climbed to levels unseen in more than a year at the same time as a furious rally has left stocks near all-time highs. Surely, both moves can’t coexist for long, goes the narrative. Why are stock traders ignoring the warning bells ringing loudly in bond markets?

The near-term impetus for the selloff in government bonds comes, first and foremost, from the sharp resurgence in oil prices amid ongoing US tensions with Iran. But the US is also the center of a transformative artificial intelligence boom, which is driving a capex supercycle that’s minting a fortune for chipmakers and spawning town-sized data centers. Elevated borrowing costs are the countervailing force the economy needs to maintain market discipline and prevent the equity rally from becoming an all-out speculative bubble.

We should all stop deluding ourselves into thinking that borrowing costs will drop meaningfully anytime soon — or that such an outcome would even be desirable. In this environment, the bond market and the Federal Reserve are doing what they should be doing in gently tapping the brakes.

Higher bond yields will be painful for real estate and other rate-sensitive parts of the economy, no doubt, but stocks can keep humming on the strength of the investment boom for now — and maybe much longer if AI companies ever manage to meaningfully monetize the new technology.

Since the start of 2023, the S&P 500 Index has delivered a compound annual growth rate of about 23% — not too far from the extraordinary 27% annual returns of the peak dot-com years. The index sat only 2% off its all-time high on Tuesday, trading at a mildly frothy 20.7 times blended forward earnings — well above the average of 19 times of the past decade. Clearly, a 10-year bond yield that’s climbed 0.4 percentage point to 4.66% since February isn’t being received as some sort of economic or risk-market catastrophe.

Instead, investors are responding to a surge in earnings and the expectation that there’s more where that came from. Wall Street’s 2026 consensus earnings per share estimate for the S&P 500 is up 7% since February, driven by extraordinary revenue growth. With only modest leverage compared to the index’s history, there’s little reason to think that higher borrowing costs alone would necessarily throw the stock market off course. Mercifully, the casino vibes are still somewhat contained (at the moment).

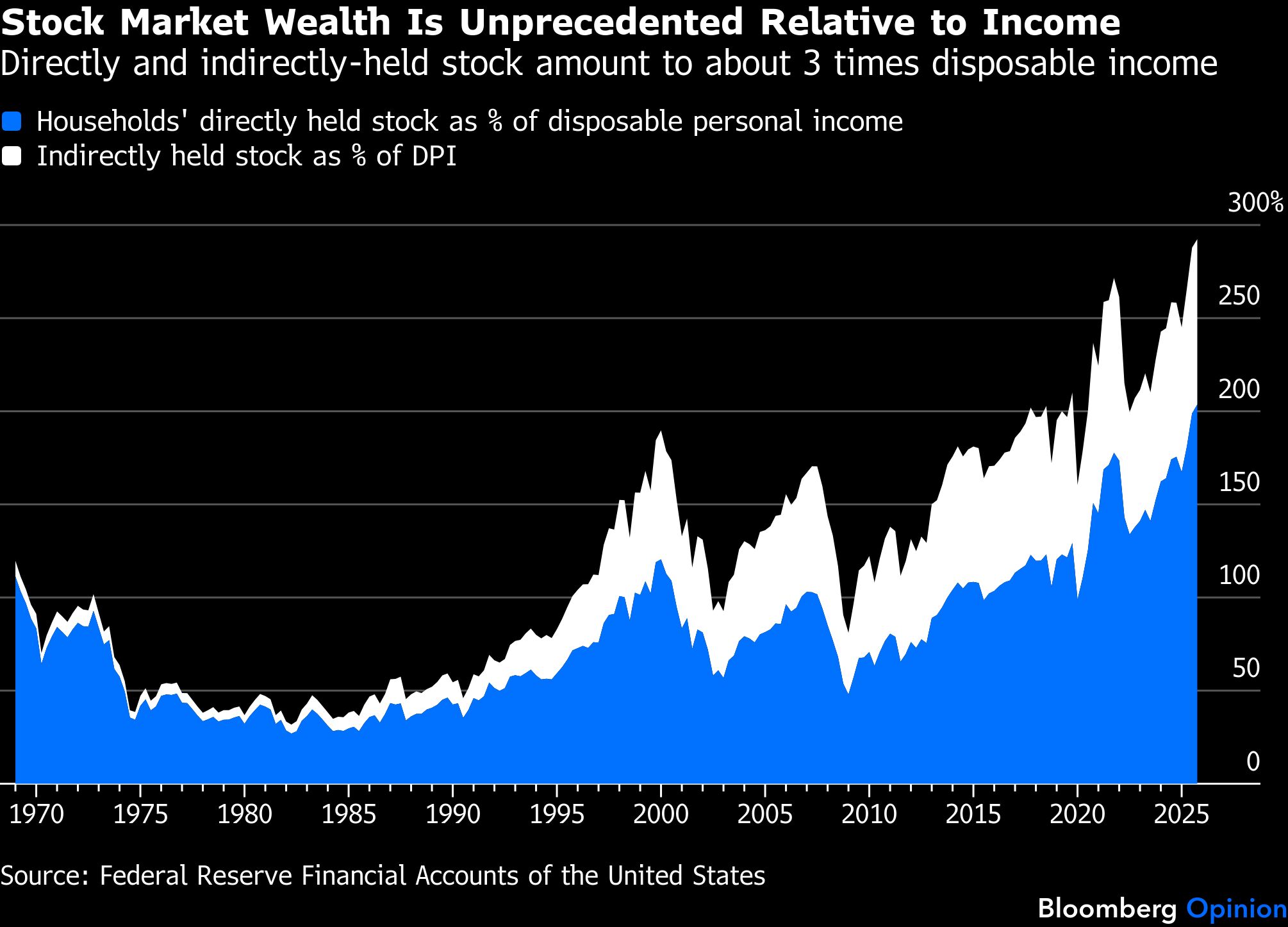

Then there’s the wealth effect, which has been breathtaking: Household net worth has increased by more than $40 trillion since the end of 2022, and the value of direct household equity holdings is at the highest on record relative to disposable income. Even if households only spend an extra penny or two for each dollar of new stock market wealth, the growth has been so strong that it’s bound to move the needle in an economy that’s predominantly driven by consumer spending.

Now consider the counterfactual. If 10-year yields were 3% today, the S&P 500 would easily be hundreds of points higher, especially when you factor in animal spirits. The conversation would be all about overheating and bubbles. That should make incoming Fed Chair Kevin Warsh extremely nervous about attempting to usher in the rate cuts that President Donald Trump campaigned for.

In theory, no one should be surprised to see high bond yields alongside a technological revolution. Productivity is hard to gauge in real time, but the productivity-driven expansion that some expect from AI has the potential to increase the marginal return on capital, which helps drive up credit demand. This, in turn, creates overheating risk if borrowing costs don’t also rise. For all the “this-time-is-different” takes, history mostly backs this up.

The most alarming precedent is the 1920s. The economy was bearing the fruit of widespread electrification, the popularization of automobiles was redefining American life and the radio industry was on fire, with Radio Corporation of America one of the decade’s most emblematic stocks. It was also a decade with vivid signs of speculative excess, including the Florida land boom and growing use of leverage in the stock market. Into that bullish cocktail, the Fed famously reduced its discount rates in 1927, feeding the bubble that would end in the 1929 stock market crash and the Great Depression.

The 1990s were a bit more complicated, but nevertheless telling. During the internet craze, Alan Greenspan’s Fed generally pursued a policy of keeping rates modestly restrictive and above the rate of realized and expected inflation. On an inflation-adjusted basis, 10-year Treasury yields averaged around 3% throughout the 1990s, compared with around 1% so far this decade. The restraint was perhaps one reason that the ultimate crash wasn’t even more economically damaging. But in 1998, following defaults by Russia and the collapse of hedge fund Long-Term Capital Management, the Fed may have helped reinvigorate the rally by cutting rates three-quarters of a percentage point. In fairness, Greenspan and his colleagues got back to hiking in June 1999, but the bubble was already mostly formed by then.

In practice, central bank policy is never the whole story. Bond markets have a mind of their own, and ill-advised Fed cuts can sometimes lead to even higher market yields, all else equal, as investors revise inflation estimates higher and price in future rate hikes that become necessary to fix the mistakes of the present.

That’s not the situation we face today. Even as Trump has pushed for interest rates of 1% or lower, Fed policymakers have maintained credibility by keeping rates at least somewhat restrictive — a stance that Warsh would be ill-advised to abandon. That has so far prevented persistently warm inflation from turning back into a 2022-style inferno. It’s also had the additional effect of keeping the economy growing within a safe and sustainable speed limit and preventing giddy stock-market investors from getting overly high on their own success, a mentality that can quickly become self-destructive.

Unfortunately for the US’s global peers, the run-up in bond yields is largely a global phenomenon, and many countries won’t get away from higher borrowing costs unscathed. Energy and bond-market conditions are slowing developed-market economies including the UK, Germany and Japan, markets that won’t see anywhere near the same tailwinds from AI spending in the near term. In the US, the restraint from rising bond yields may be subtly preventing a boom from turning into a frenzy, and long-term investors lamenting today’s bond-market conditions should be careful what they wish for.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Jonathan Levin