The Energy Pivot: Establishing Supply in the Face of Historic Demand

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

I just kept eyeing my monitor in disbelief. On the screen was the monthly statement from our electrical company. The charge was three times as much as the highest bill we had ever received. When I shared the amount with my team, they immediately reached for their sweaters, knowing the office thermostat was about to take a nosedive.

Artificial intelligence has relentlessly inundated every facet of our lives, sparking a massive surge in energy demand to power this new technology. At the same time, the Iran conflict has critically disrupted global energy markets. Energy has always been top of mind for nations around the world, but a clear shift is now taking place: Those who do not invest appropriately will almost certainly fall behind.

How, then, will nations generate the electricity to meet the demands of AI?

Everyone’s Drilling, Baby

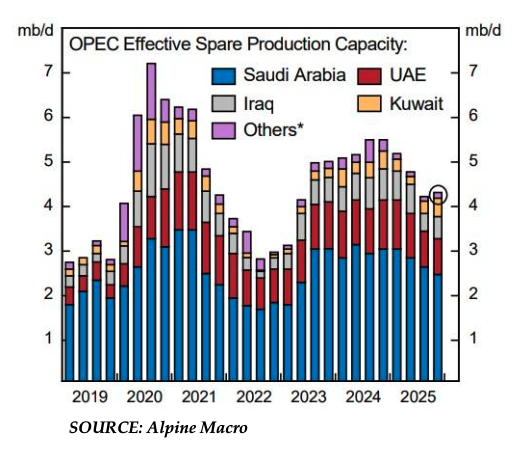

During the first Gulf War in 1990, I recall hearing the protest chant, “No war for oil!” That, of course, was at a time when the United States was far more reliant on Middle Eastern supply. Since that time, the U.S. has evolved into the world’s leading oil supplier, and not by a small margin. Saudi Arabia and Russia are a distant second and third [source: U.S. Energy Information Administration]. Total global supply is up 24% since 2000, and would likely be even higher if not for the COVID interruption when the price of Brent Crude oil fell to a lowly $32 per barrel.

More recently, prior to the Iran conflict, the price per barrel had slipped to under $60. Oil inventories had reached multi-year highs and OPEC+ (a 23-nation alliance of oil-producing countries) was operating well below capacity. Most market traders anticipate that once the Strait of Hormuz re-opens, oil production will skyrocket to make up for lost revenue, suppressing prices to their previous lows.

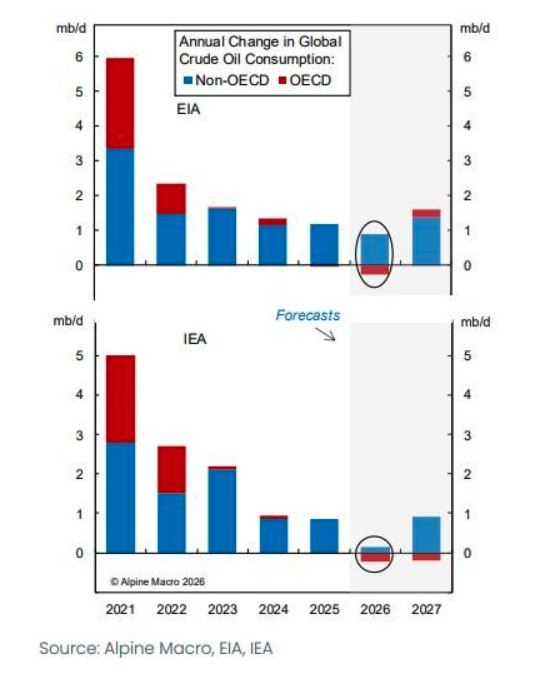

Will global demand meet this supply? It doesn’t appear so. Nations overly dependent on oil have learned their lesson and will likely diversify their sources of energy going forward. Broader U.S. demand is expected to drop significantly in the coming decades as other sources of electricity become more abundant, such as renewables and natural gas.

Oxford Economics projects that electric vehicles will constitute 80% of new vehicle sales in the U.S. by 2050. China’s demand for oil is also expected to be reduced significantly, as I will address later. Japan and South Korea, who are for the moment heavily reliant on Middle Eastern oil, will likely look to diversify their energy to avoid geopolitical risk associated with that part of the world.

If Oil Becomes Cheap, Why Diversify?

As of this writing, the price for a gallon of gasoline in Zurich, Switzerland is over $9 USD. You read that correctly. Over the past four years, due to COVID and now the Iran conflict, the price of energy has inflicted significant harm on the EU, one of the world's largest economies. Until recently, Europe relied on a more local supplier of oil and natural gas to avoid dependence on the unpredictable Middle East. Unfortunately, that supplier — Russia — invaded Ukraine, forcing the EU to make some difficult choices.

Assuming prices eventually normalize, cheap oil today doesn't help much when your supplier turns hostile tomorrow. Nations across the globe, instead of asking, “What does energy cost right now?" are turning their attention to "What happens the next time the supply chain breaks?"

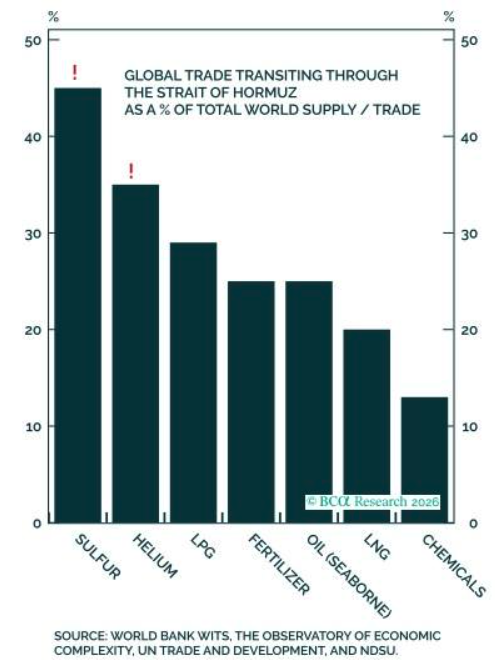

It also turns out that the Iran conflict's reach extends well beyond crude oil. According to BCA Research, the Strait of Hormuz carries roughly 45% of the global sulfur trade, 35% of helium, and significant volumes of fertilizer and LNG. The disruption ripples beyond gasoline pumps — into agriculture, manufacturing, and even uranium production, which I'll come back to shortly.

Absolute Strategy Research's Michael Hessel has constructed a series of scenarios for how global energy policy will evolve. One of the more likely outcomes is what he labels as "Energy First" — a world in which nations prioritize energy security over price economics. In that world, capital flows wherever governments direct it, regardless of whether oil is $50 or $150 a barrel. This will require sophisticated energy diversification.

Perhaps most importantly, oil doesn't power data centers. Nor does it power EV batteries, air conditioners, or any of the critical components that are increasingly running modern life. The story of the next decade isn't really about oil. It's about electrification.

Electricity, Eee-lectricity!

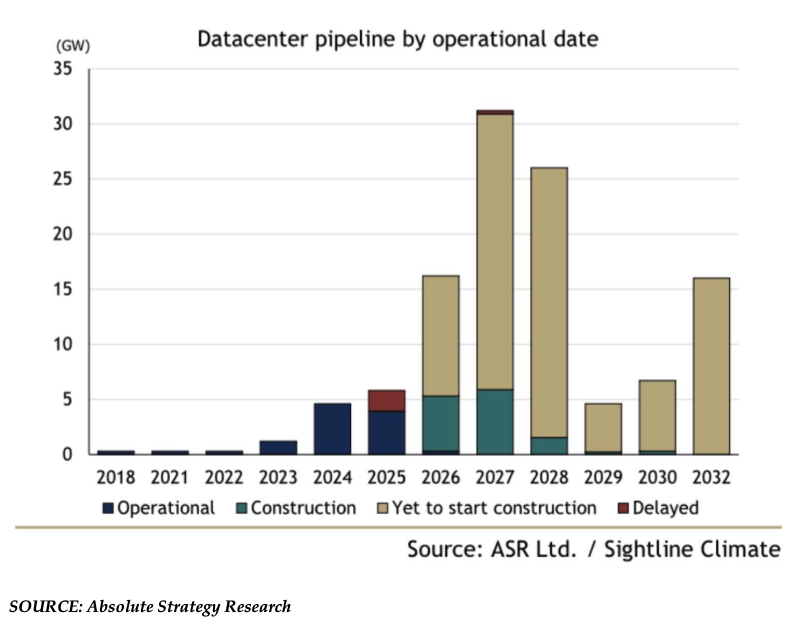

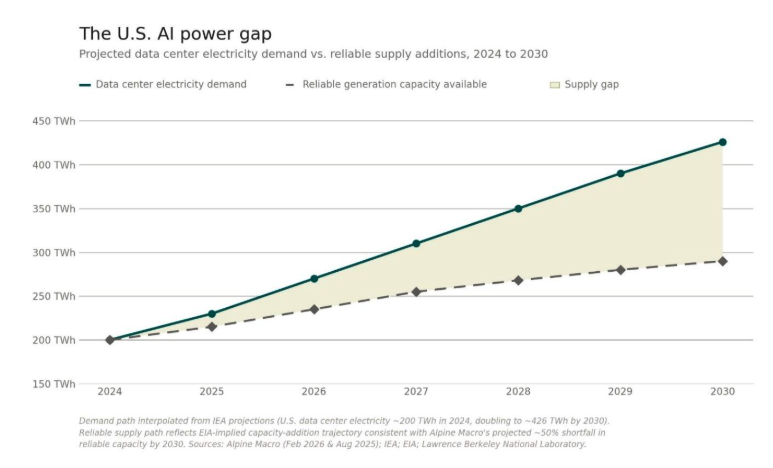

While the U.S. presently is the leader in AI development, it has a problem: AI is going to consume energy at a scale that current infrastructure is unable to deliver.

Alpine Macro estimates that global data electricity demand will increase by 128%... in six years! By the year 2030, the U.S. is expected to have an energy shortfall of 50%. We can compensate through new electrical transmission projects, but that presents another problem: New commercial data centers typically take two to three years to construct, while new transmission projects require four to eight years. In fact, in spite of the humongous levels of hyperscaler spending on data centers, only a very small fraction are actually online. The delay? Yup, lack of power:

The Trump administration has a mixed record with managing this energy gap. To its credit, Trump has taken unprecedented steps to expand the use of nuclear energy, which is a very powerful source of clean energy. Further, the administration is highly supportive of geothermal energy, a largely underused source in the U.S. They have also reduced the amount of time required to obtain permits for new energy generation.

Unfortunately, Trump, mostly due to ideological purposes, has elected to roll back the clean energy subsidies passed into law during the Biden administration. As noted above, if energy security is the primary objective, then the U.S. would benefit from utilizing every option available.

Going Nuclear

Have you ever seen the movie, “The China Syndrome,” starring Jane Fonda, Jack Lemmon and Michael Douglas? The plot involves a criminally constructed nuclear reactor that, if it were to melt down, would carve its way to the other side of the earth all the way to China. Released twelve days before the partial meltdown at Three Mile Island in 1979, the film helped scare a generation of Americans away from nuclear power for the next four decades.

If you haven't seen it, well then, don't. Because guess who just signed a 20-year deal to acquire power from Three Mile Island? Microsoft. To power its AI. Like it or not, nuclear energy is coming back to a theater near you.

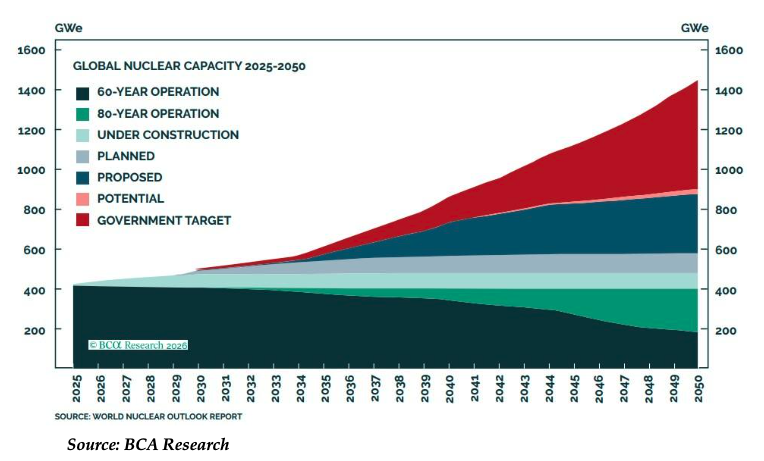

The demand for nuclear energy is soaring. The World Nuclear Association projects an increase in generation capacity of 260% between 2025 and 2050. The International Energy Agency anticipates nuclear investment will triple between now and 2035. Nuclear's biggest challenge isn't demand — it's supply. The world's reactors consume roughly 180 million pounds of uranium each year, but long-term supply has run closer to 116 million.

Western buyers are losing ground, with Kazakhstan and Niger's production effectively offline since the 2022 and 2023 coups. Even the Iran war has tightened the supply chain in unexpected ways: Roughly 45% of global sulfur trade transits the Strait of Hormuz, and sulfuric acid is the critical chemical needed to extract over half the world's uranium.

Much of the investment in nuclear will be devoted to small modular reactors (SMRs). SMRs are exactly what they sound like — nuclear reactors small enough to fit on a single industrial site and modular enough to be manufactured in a factory. Where a traditional nuclear plant takes a decade and tens of billions of dollars to build, SMRs are designed to come online in years rather than decades, at a fraction of the cost.

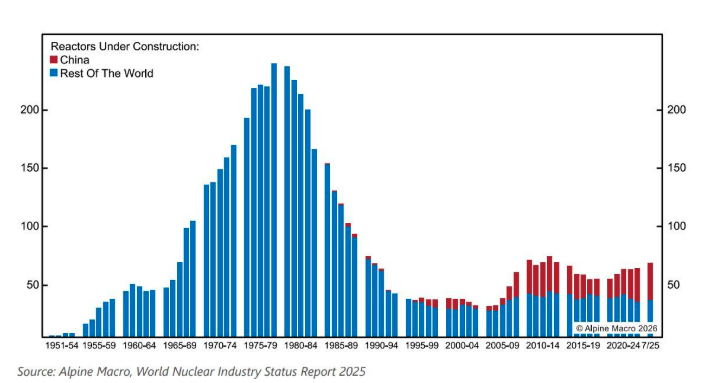

They are also small enough to be co-located next to AI data centers — which is exactly why companies like Amazon, Google, and Oracle have already signed deals with SMR developers to power their compute infrastructure. Despite this, the rest of the world lags behind China’s reactor construction.

Picks and Shovels

There is an old business proverb: When everyone is digging for gold, you have a better chance at profits by selling shovels.

In addition to energy demand, the world has another problem — existing electrical grids are not capable of meeting the levels of power demand expected by Alpine Macro and others. Apollo Global Management estimates that the global energy transition requires an investment of $60 trillion–$80 trillion (!) for power generation and utilities. Too much of the world’s infrastructure is insufficient to handle tomorrow’s demand.

There is one country that is simultaneously generating increasing amounts of energy along with the capacity to deliver that energy — you guessed it, China.

The uncomfortable truth is that everyone else in the world is lagging far behind. Oxford Economics indicates that there is a $15 trillion funding gap for the G20 economies. The U.S. is dramatically behind with a $3.7 trillion funding gap over the next seven years. Meanwhile, Federal infrastructure spending has momentarily plateaued. The EU is also behind but is actively mobilizing, spending $700 billion on clean energy infrastructure. Japan and South Korea have also allocated or proposed near-term infrastructure spending for this purpose. More will need to be done if nations want to keep pace in the AI and quantum computing race.

Headwinds

Naturally, there are a variety of risks and impediments to these global energy objectives.

Much of this capital investment will be derived through government appropriations, and accordingly, such expenditures are subject to policy reversals. This is precisely what we have seen with the Trump administration’s pullback on clean energy. Further, even when fully approved, construction can take years, perhaps decades, to complete.

At present, China is massively oversupplied with EVs, solar energy components and a variety of related goods. They are actively attempting to sell these goods globally at rock-bottom prices. So far, most major economies are blocking these sales to protect their domestic manufacturers. If deals are ultimately struck to permit the sale of China’s goods across the globe, it would likely have a consequentially adverse effect on clean energy producers.

There are a wide variety of economic and financial risks that can directly impede the investments discussed in this article. Government debt is at historic levels, there is greater kinetic conflict in the world than in recent years, and most nations are actively competing for available resources to facilitate energy investments. All of these risks can lead to steady and accumulating inflation.

Conclusion

Put succinctly, the world today requires substantially more electricity than only a few years ago. AI, electrification, reshored manufacturing, and population growth in the developing world are converging into a demand curve that the existing global power system simply cannot meet.

The gap already affects virtually every user — from my terrifying PSE&G bill, to transmission queues stretching past 2030, to every politician taking angry calls from their constituents. Closing the gap will require trillions of dollars of investment and decades of construction.

Some countries are leaning in, but most, including the U.S., are not yet doing enough. Apart from China, none are doing it fast enough.

Sources

Alpine Macro, "Post-War Oil Market: From Scarcity To Glut?", written by Kelly Xu, April 20, 2026

Alpine Macro, "Uranium: The Bull Case Deepens", written by Noah Ramos, February 17, 2026

Alpine Macro, "The AI Commodity Nexus: Powering Demand For Energy And Metals – Special Report", written by Kelly Xu, February 2, 2026

Alpine Macro, "AI, Energy, And The Grid – A Collision Course", written by Noah Ramos, August 6, 2025

Alpine Macro, "Renewable Energy: Exploring Unconventional Opportunities", written by Noah Ramos, October 29, 2025

Absolute Strategy Research, "Funky Correlations & Missing Links #19: Is the Market Complacent about the Risk of Stagflation?", written by David Bowers and Ian Harnett, April 22, 2026

Absolute Strategy Research, "Investing in a Resource-Constrained World", written by Michael Hessel, March 4, 2026

BCA Research, "Uranium: The Bull Case Just Got Enriched", written by Jeremie Peloso, April 13, 2026

Rosenberg Research, "Middle East Crisis Makes Alternative Energy a Big Winner", written by Robert Embree, March 25, 2026

Rosenberg Research, "Building the Future: The Investment Case for Private Infrastructure", written by John Smolinski and David Rosenberg, September 4, 2025

Rosenberg Research, "Early Morning with Dave", written by David Rosenberg, March 19, 2026

Oxford Economics, "Global oil demand set to peak in 2028", written by Jack Reid, February 11, 2026

Oxford Economics, "Stable long-run inflation expectations argue against a rate hike", written by Grace Zwemmer, March 30, 2026

David Tepp is the founder and chief wealth strategist of Tepp Wealth Management, an SEC-registered investment advisor based in Westfield, New Jersey. With over 20 years of experience in wealth management, David provides strategic financial planning and investment advisory services to high-net-worth individuals and families. He frequently writes on macroeconomic policy, fiscal risk, and market strategy to help investors navigate an increasingly complex global economy.

DISCLOSURES

Investment advisory services offered through Tepp RIA, LLC dba (Tepp Wealth Management), is a SEC registered investment adviser. Registration as an Investment Adviser with the SEC or any state securities authority does not imply a certain level of skill or training. For information pertaining to the registration status of Tepp Wealth Management, A copy of Tepp Wealth Management’s current written disclosure statement discussing Tepp Wealth Management’s business operations, services, and fees is available at the SEC’s investment adviser public information website – www.adviserinfo.sec.gov (CRD# 283899) or from the Adviser upon written request: Tepp Wealth Management, 210 Elmer Street, Westfield, NJ 07090.

This article is an expression of corroborated facts along with the opinions of the author. This is for informational purposes only and is intended to inform the reader about market-related activities which could affect individual portfolios and provide insight on specific relevant topics. It is not intended to recommend or suggest any specific course of action or investment strategy. The reader should not infer the likelihood of any future events. Past performance is not indicative of future results. Investors should always consult an investment professional and/or tax professionals to discuss their unique needs and objectives.

Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by the Adviser), will be profitable or equal any historical performance level(s). Investing involves risk, including the potential loss of principal.

Tepp Wealth Management may discuss and display, charts, graphs, formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. Tepp Wealth Management has no affiliation with any sourced company, and the use of such information should not be considered an endorsement of any firm. This information is provided for guidance and information purposes only and is not a solicitation. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All