South Korea is home to the world’s best-performing stock market, up by 71% this year. But global investors, who own about 39% of the Kospi index, have been steadily selling, offloading almost $60 billion since Jan. 1.

At first glance, the retreat of foreign asset managers is ominous. Signs of a domestic retail frenzy are everywhere. Cash deposits in local brokerage accounts have reached 137 trillion won ($91 billion), a two-third jump from six months ago. Margin loans have also hit record levels as locals amplify their bets. Are global institutional investors voting with their feet; is this a sign that the Kospi has become excessively exuberant?

Global funds may just be rebalancing to maintain a diversified portfolio. If anything, their actions are a reflection of how narrow the global AI-fueled stock rally is — a problem the US market also faces. It’s not a bearish directional bet against the Kospi.

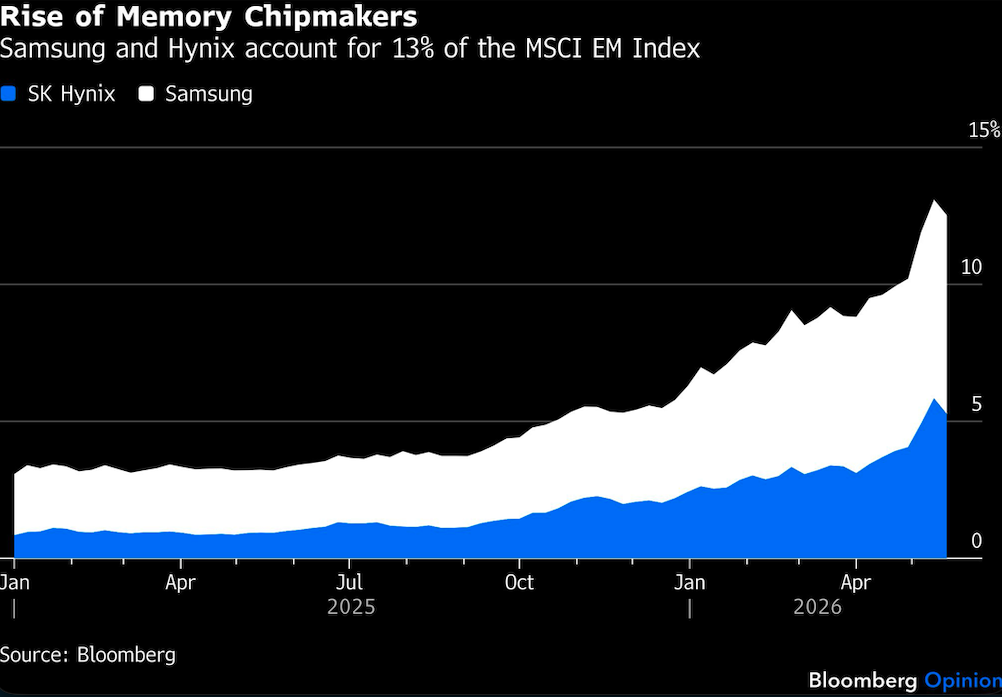

Most of the selling is concentrated in Samsung Electronics Co. and SK Hynix Inc., poised to be among the world’s most profitable companies this year as AI demand for memory chips soars. Ironically, their outsized success is forcing global funds to trim positions to avoid excessive single-stock concentration.

Take a look at the MSCI Emerging Markets Index, the benchmark for more than $1 trillion in assets under management. After more than doubling in market value this year, Hynix commands a weighting equivalent to China’s tech giants Tencent Holdings Ltd. and Alibaba Group Holding Ltd. combined. The two Korean chipmakers, alongside Taiwan Semiconductor Manufacturing Co., account for more than 25% of the benchmark index and have contributed to over 70% of its gain so far in 2026. As a result, this entire asset class is becoming an AI-infrastructure proxy.

For managers schooled in diversification, it would be difficult to stay with the rally even if they believed the Korean chipmakers were still reasonably valued.

Meanwhile, retail investors don’t mind putting all their eggs in one basket. In fact, many are clamoring for financial products with just one theme — especially along the AI supply chain. In the US, the Roundhill Memory ETF, a highly concentrated play with the two Korean chipmakers making up almost half of the entire portfolio, was launched in early April. It already has $8.7 billion of net inflows, making it the fastest-growing ETF ever.

In a way, professional managers’ Kospi dilemma is not unlike the headache they faced in late 2020, when Chinese companies made up more than 40% of the MSCI Emerging Markets Index. That excessive concentration ultimately led to the creation of new indices that catered to those who wanted to invest in the asset class without being crowded out by China.

Going forward, the key question for professional stock pickers is whether they are willing to cast aside old-school portfolio construction and accept concentration risks. Chances are, the AI-fueled rally will likely go hand-in-hand with poor market breadth. In chip manufacturing especially, those with state-of-the-art factories and assembly lines in place get to earn profits immediately, resulting in winner-takes-all scenarios.

As such, in a rising market, maintaining diversified holdings, which would entail selling some outperforming stocks, means they have to leave money on the table and explain to investors why the benchmark is delivering better returns. On the other hand, betting on just a few AI beneficiaries greatly increases drawdown risks.

As a revolutionary technology, AI is disrupting every corner of the financial markets as well as the socioeconomic order. The debates it has set off in Korea, from workers’ pay and wealth redistribution to the changing market leadership and what the best investment portfolios should look like, are resonating well beyond its shores.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.