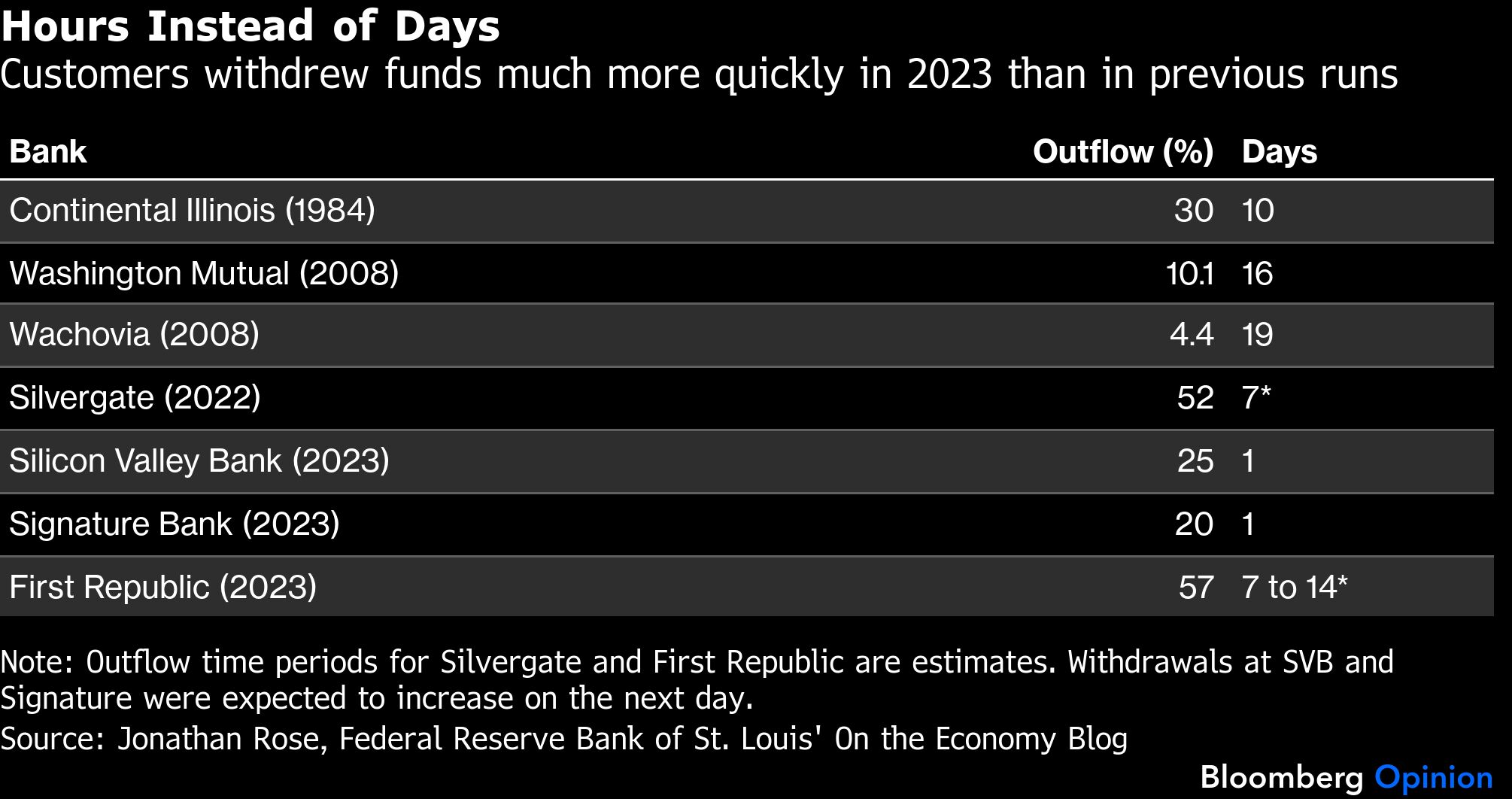

It’s been more than three years since Silicon Valley Bank lost a quarter of its deposits in a day, kicking off a string of bank rescues. The shocking speed of that run was attributed, in part, to the rapid spread of information on social media and the efficiency of digital banking. Future panics could unfold even faster. Policymakers ought to stop debating the risks and erect some common-sense guardrails.

Advances in technology are only making it easier and more attractive for depositors to withdraw their funds from banks. Artificial intelligence tools may soon be able to shift money around automatically and instantaneously in response to negative news or changes in deposit rates. Meanwhile, the growing supply of stablecoins — a kind of digital cash meant to be backed by actual dollars — offers an alternative to deposits, one that has alarmed the banks.

If there’s another crisis, what defenses have been erected since 2023 may not hold up. The percentage of deposits that exceed the $250,000 federal insurance limit — as more than 90% of Silicon Valley Bank’s deposits did — has declined from its two-decade peak in late 2021. Yet a recent analysis from the Federal Deposit Insurance Corp. found that withdrawals during the 2023 debacle extended beyond uninsured funds; top depositors pulled virtually all their money.

More important, Silicon Valley Bank wasn’t set up to borrow from the Federal Reserve’s discount window, which might have provided a ready source of liquidity. While more banks are today, the number is still too low. The Fed can only lend against good collateral — collateral that banks often have incentive to keep elsewhere.

Rather than mandating that banks hold enough liquid assets to meet an estimated 30 days of withdrawals — a meaningless rule if deposits can be drained in a week — regulators should give them credit for collateral that’s been pre-pledged at the Federal Reserve. The combination of liquid assets and borrowing capacity from the Fed against that collateral should be sufficient to cover all short-term liabilities — both on-demand deposits and any other funding due within a month.

The point is to have access to cash, not just to hold a lot of it. Banks that find these new requirements too onerous can replace some short-term liabilities with longer-term funding.

The change would accomplish several desirable goals. Ensuring that banks can pay off all depositors will reduce the likelihood and severity of runs. Giving banks liquidity credit for collateral at the Fed can mitigate the long-standing stigma associated with borrowing from the discount window — and lessen banks’ tendency to depend on the less reliable Federal Home Loan Banks. And decreasing the need to hold liquid assets should help banks get back to making loans instead of stockpiling Treasuries.

At the same time, regulators should insist on high levels of capital to absorb losses on assets. Central banks are meant to provide emergency liquidity only to banks that are solvent — which, as research has shown, rarely proves to be true when there’s a run. Recent moves to allow more leverage at banks are thus counterproductive.

The deposit-funding model that has sustained banks for centuries could soon face unprecedented strains. Now is the time to prepare for the next crisis.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.