The SpaceX initial public offering prospectus is more than 400 pages of rocket fuel-grade ambition. It is also an extended warning for investors in Tesla Inc. who aren’t named Elon Musk.

Musk’s latest pitch to the public market involves a mooted $2 trillion valuation for Space Exploration Technologies Corp., where he is chief executive officer, chief technical officer and chairman. Common to all Musk ventures, the company calculates a total addressable market that is monumental, only more so; the largest “in human history” at $28.5 trillion. Future money spinners include such lively challenges as “energy production on the Moon and Mars” and “in-orbit manufacturing.” The market has become inured to the wild claims of special purpose acquisition companies of late, but this is perhaps better described as a special purpose aspiration company.

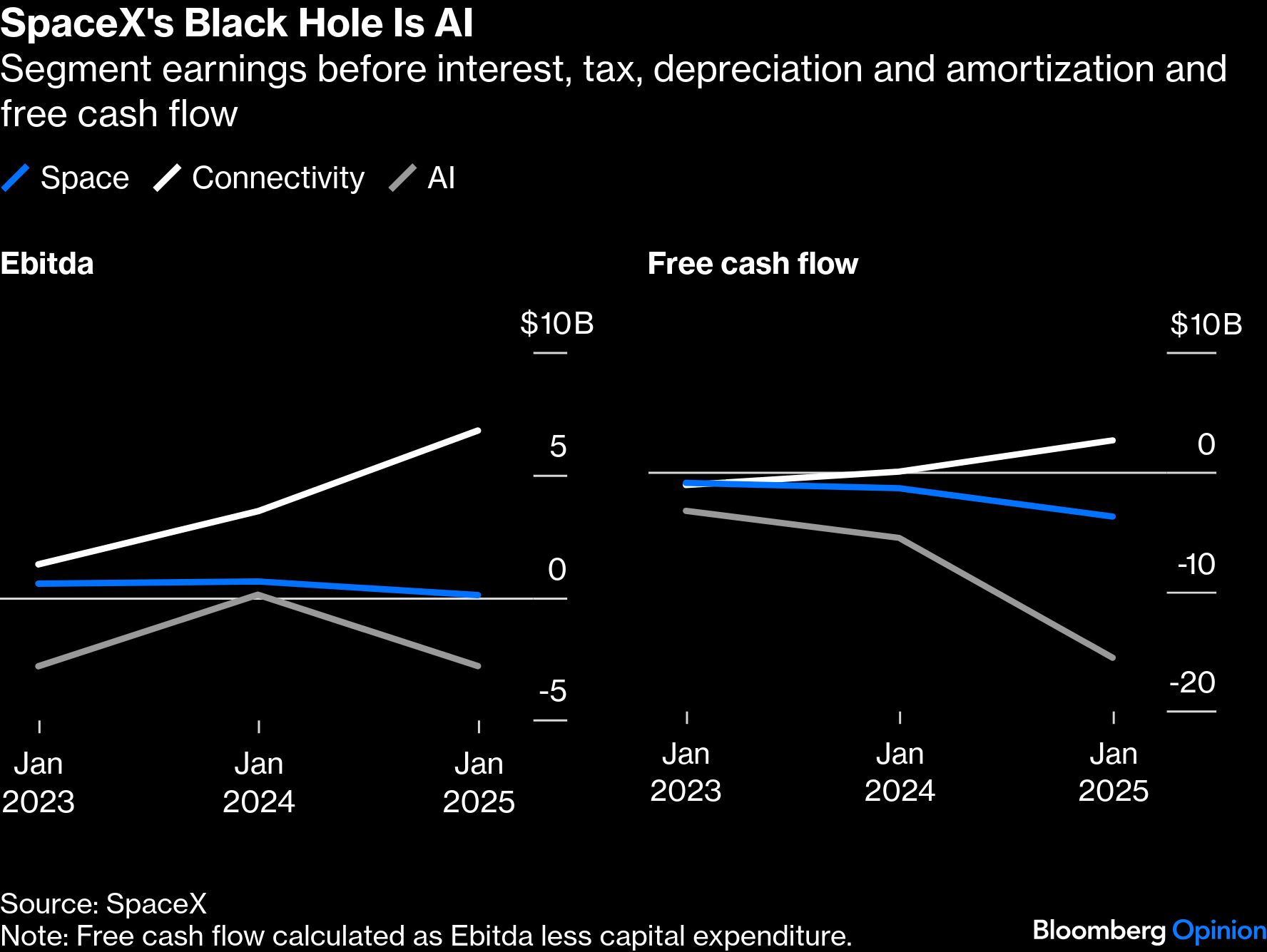

Within the noise, however, there is signal. The core business of SpaceX is launching rockets and providing satellite communications services via Starlink. These two divisions, space and connectivity, can be thought of as a symbiotic whole for now. Most launches carry those company-owned satellites, and together, they constitute a business with fast-growing profits that was almost self-funding last year.

Of the $28.5 trillion touted addressable market, however, 93% relates not to that core business but instead to artificial intelligence. This is where things begin to converge with Tesla, an electric vehicle maker that Musk, also CEO there, has rebranded an AI and robotics leader.

SpaceX properly launched itself into this now critical business only this year with the acquisition of another Musk company, xAI, which had itself bought another Musk company, the social media platform X, last year. The $250 billion that SpaceX paid for xAI in stock, a cool 78 times trailing revenue, was undoubtedly a good deal for xAI — which means a good deal for Musk and the various private investors, as well as creditors, he corralled to fund his struggling social media and AI side gigs.

You can tell they were struggling because the financials reveal an AI division that is barely growing and burned almost five times more cash in 2025 than it did two years before. You can also tell because most of the debt on the SpaceX balance sheet consists of a bridge loan to refinance the junk debt it inherited with buying xAI.

This might strike a familiar clang to investors in Musk’s existing listed company.

Tesla has switched its narrative, and analysts have shifted their valuation stacks, away from electric vehicles toward AI and robotics. One result of this is a massive increase in capital expenditure, even as revenue and margins have stalled out. Tesla generated roughly $6 billion of positive free cash flow last year and is forecast to burn through almost $10 billion this year. Positive inflows aren’t anticipated until 2029 — and Wall Street is habitually overoptimistic on Tesla’s long-term earnings.

The commonality of cash burn between SpaceX and Tesla isn’t just coincident, of course.

Tesla plowed $2 billion into xAI just before SpaceX bought the whole thing (Tesla’s investment converted to a small stake in SpaceX). Tesla and SpaceX are also collaborating on the huge (read: expensive) undertaking of building a giant chip-making facility, dubbed the Terafab, although the details around schedule and spending haven’t been agreed. They are also jointly developing an agentic AI tool with the decidedly brogrammer name of Macrohard. And both companies are also apparently planning to build large-scale solar equipment factories barely two hours drive away from each other in Texas.

In other words, when it comes to narrative, spending and, of course, governance, the Venn diagram for SpaceX and Tesla approaches something like a total eclipse.

For Musk, SpaceX is a more perfect public vehicle than his existing one. He has a much bigger stake and, with a dual-share structure, effectively unfettered control that outclasses even the supine board and forgiving shareholder base of Tesla. At $2 trillion, SpaceX would also eclipse Tesla on valuation and the core rockets-plus-Starlink business can even claim fast-growing profits, which Tesla no longer can. Musk also just seems far more enamored with the idea of humanity saving itself by leaving the planet rather than protecting it these days.

For all this, plus the added attraction of not having to host two sets of earnings calls, the logic of combining Tesla with SpaceX would seem pretty straightforward for Musk. He would get a company more closely aligned with his interests of near-absolute control, narrative plasticity and seamless cross-subsidization. Yet any such deal would also present a conflict risk of galactic proportions.

With Musk having 85% control of SpaceX, pre-IPO, and a 20% stake in Tesla, the merger math would favor SpaceX getting Tesla for a bargain rather than bidding it up. The IPO itself could be a catalyst for this. Tesla’s shareholder base is believed to have a particularly large retail cohort, perhaps as high as 40%. SpaceX is reportedly considering reserving a high share of its offering, as much as 30%, for the retail crowd — the prospectus’ purple prose and artistic renderings seem geared that way, at least. A migration of some money away from Musk’s old thing to the new thing looks likely, especially with the first evidence of Tesla’s cash burn due to be revealed in early July.

The net result would be a widening of the likely valuation gap between Musk’s heavenly AI vehicle and his earthly one — and an invitation for him to do some cosmic alignment.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Liam Denning