Bankers are preparing to sell a jumbo debt package to support the $110 billion acquisition of Warner Bros. Discovery Inc. It’s a risky deal and comes at a moment when the bond markets have been wobbling. Even with the backing of the billionaire Ellison family, this will be a major test of debt investors’ willingness to support megamergers.

Paramount Skydance Corp., led by Top Gun: Maverick co-producer David Ellison, agreed to buy Warner in February after outbidding streaming giant Netflix Inc. The financial resources of his father, Oracle Corp. co-founder Larry Ellison, were central to winning the auction. After all, Paramount’s market value is barely $12 billion and it’s already weighed down with debt.

The main item on the bill is paying Warner shareholders $81 billion in cash to satisfy the $31-per-share offer price. Paramount must also assume Warner’s $29 billion of net debt. Around half of this will be rolled over into the enlarged company through a deal agreed this week. That still leaves $15 billion of Warner borrowings needing to be refinanced.

As for the sources of cash to cover all this, the starting point is the Ellisons and their Gulf sovereign wealth fund partners writing a check for $47 billion. Roughly half of that equity is being provided by the family. It will be for the debt markets to stump up $49 billion to cover the rest of the purchase price and the refinancing.

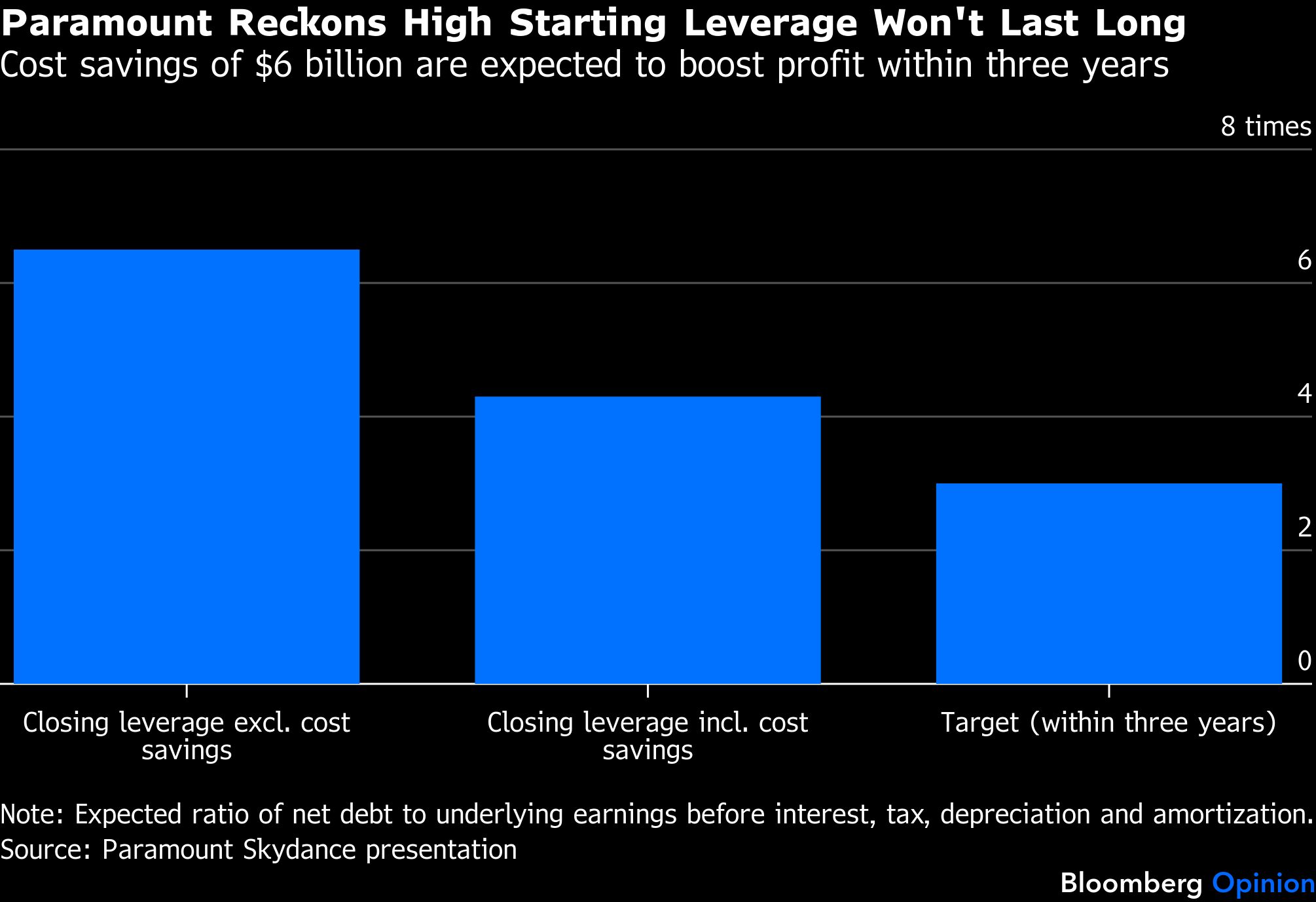

On its face, the investment case here looks pretty scary. The merged business will start life with extremely high leverage. Paramount’s existing debt, Warner’s rolled-over borrowings and the new debt add up to nearly $90 billion. Net debt will be 6.5 times this year’s forecast profit as measured by earnings before interest, tax, depreciation and amortization. That’s the kind of credit ratio you see in a private equity buyout, not a public company.

What makes this so nerve-wracking is that Paramount is doubling down on cable-TV, an industry that’s losing customers to streaming services. This melting ice cube is the main contributor to profit.

Of course, combining the companies’ legacy TV operations is also the main source of the immense $6 billion of annual savings that helped Paramount justify outbidding Netflix. These are critical to bringing down that excessive starting leverage. In addition, there is clear scope to create a powerful streaming platform by combining the Paramount+ and HBO Max franchises.

But the potential benefits of mashing together Paramount and Warner won’t harvest themselves. They depend on Ellison junior delivering an integration like nothing he has managed before. Media M&A has a history of disappointing, including deals involving these two firms.

And even if Ellison pulls off this grand operational feat, there’s the looming specter of artificial intelligence. As analysts at Moody’s Corp. say, it may be risky to bet that compelling storytelling will be among the few cognitive functions AI fails to master.

Finally, there’s just the sheer size of it all. The debt needs are so ambitious that Paramount is targeting two different groups: marketing senior secured debt to investment-grade bond investors and riskier junior debt to the junk market. That split structure mimics Charter Communications Inc., which analysts at Bloomberg Intelligence see as a comparable credit. Apollo Global Management Inc.’s insurance business is expected to take a large slice of the investment-grade offering, according to Bloomberg News.

However risky this looks, at least it’s not software, the sector facing really serious financing challenges. If the merger savings fail to materialize, the Ellisons would have the means and incentive to put in cash themselves. Their reputations and their equity investment would be on the line. Indeed, they’ve formally committed to cut the leverage ratio to three times.

This should give comfort to debt investors. If it doesn’t, the Ellisons have the capacity to inject more money to reduce the starting debt. Larry Ellison is fifth in Bloomberg’s Billionaires Index, with a net worth of nearly $250 billion.

“If you’re lending money you should have some comfort that the equity is $47 billion,” says Stephen Flynn, a Bloomberg Intelligence credit analyst. “It’s a very large check.”

Conditions may not be as favorable as they were a few months ago; inflation fears driven by the Iran war have pushed up benchmark government yields. But corporate bonds are still in demand. High-yield debt volumes are up 41% year-to-date, Bloomberg data show. The average yield on corporate junk debt is higher than when the Warner takeover was agreed, though remains lower than it was a year ago.

All in all, the cost of debt may be broadly in line with what the Ellisons should have been expecting when plotting their bid for Warner earlier in 2025. Paramount is wise to try to lock in the money before the funding environment possibly worsens. But if this borrowing gets done without the terms being too pricey, it can only encourage more dealmaking.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Chris Hughes